|

市场调查报告书

商品编码

1911759

义大利资料中心:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)Italy Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

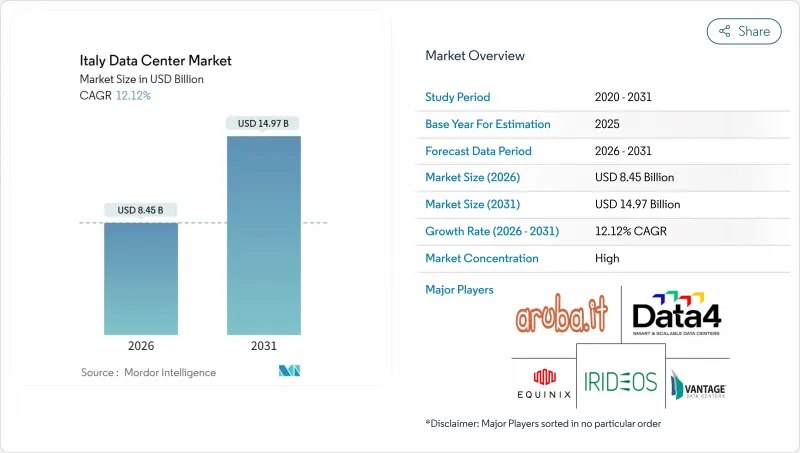

预计义大利资料中心市场将从 2025 年的 75.4 亿美元成长到 2026 年的 84.5 亿美元,到 2031 年达到 149.7 亿美元,2026 年至 2031 年的复合年增长率为 12.12%。

就IT负载容量而言,市场预计将从2025年的1080兆瓦成长到2030年的4090兆瓦,在预测期(2025-2030年)内复合年增长率(CAGR)为30.49%。市场占有率和估计值均以兆瓦(MW)为单位计算和报告。需求成长的驱动因素包括超大规模云端运算的扩张、公共部门积极的数位化计画以及对人工智慧驱动运算日益增长的需求。米兰凭藉其靠近跨欧洲光纤线路、电力采购的改善以及不断增加的海底电缆铺设计划,仍然是高密度建设的理想位置。与法兰克福、伦敦、阿姆斯特丹、巴黎和都柏林相比,义大利的土地和电力供应更容易取得,因此也更受国际投资者青睐。併购活动的活性化表明,随着规模经济成为决定性因素,市场可能正在进入整合阶段。

义大利资料中心市场趋势与分析

超大规模资料中心业者加速云端扩张

如今,义大利已成为全球云端服务供应商的首选目的地,他们希望将资源从拥挤的北欧枢纽转移出去。微软正在Lombardia投资43亿欧元(约46亿美元)兴建新设施,并计画在2027年前投入多个可用区运作。谷歌云正在米兰和都灵开设横跨六栋建筑的双区域,以满足本地数据居住需求。亚马逊网路服务(AWS)正在评估一些前义大利国家电力公司(Enel)的发电厂旧址,例如蒙塔尔托·迪·卡斯特罗,这将缩短审批时间并充分利用现有电网。外资的涌入正在帮助提升建筑标准,促进液冷技术的应用,并促成与国家电网营运商Terna签订重要的电力合约。

基于PNRR的公共部门云端迁移

义大利耗资1915亿欧元的「復苏与韧性计画」(PNRR)加速了全国的数位转型。 2024年,国家战略中心(Polo Strategico Nazionale)授予了价值5.2亿欧元的合同,用于将各部会的工作负载迁移到主权云,比上一年增长了73%。该倡议要求资料储存在国内,优先选择具备量子级加密和99.995%运转率的Tier 4级资料中心。义大利电信(TIM)正在投资1.3亿欧元(约1.41亿美元)在罗马附近建造一座25兆瓦的资料中心,预计2026年底完工。此资料中心专为GPU丛集而设计。随着各市政当局也积极回应,公立医院、学校和其他场所对小规模边缘节点的需求也不断增长。

电力成本上涨和电网限制

预计到2024年,义大利批发电力价格平均将达到133欧元/兆瓦时(144美元/兆瓦时),比法国高出30%,比西班牙高出40%,这将对营运利润率构成压力。截至2025年3月,义大利国家电网公司(Terna)已接受42吉瓦的併网申请,远超过目前的发电储备容量,并暴露出供给能力短缺的问题。可再生能源审核速度缓慢,2022年全部区域提交的太阳能申请中仅有1%获得批准。义大利资料中心市场要求营运商签订多年期可再生能源购电协议(PPA),投资兴建现场储能电池,并根据变电站升级改造分阶段进行建置。

细分市场分析

大型资料中心将引领义大利资料中心市场的发展,预计到2025年将占总营收的46.45%。 Digital Realty和Aruba等供应商正将这些设施用作批发託管套件和多租户云端节点的丛集。同时,随着超大规模云端服务供应商将人工智慧训练工作负载转移到内部,预计到2031年,大型园区(超过60兆瓦)将以29.10%的复合年增长率成长。米兰东环路週边地区的建设热潮尤为明显,该地区三个总合装置容量达350兆瓦的计划已于2025年破土动工。公用事业规模的用地面积需要专用的150千伏特电网连接和现场变电站来降低输电费用的波动。随着工厂和电信中心机房的模组化扩建能够满足边缘运算的需求,小规模资料中心正在稳步减少。

加速向更大规模发展将降低整体拥有成本。将电力基础设施分布在更多机架上,可使每千瓦的资本支出降低高达 25%,而集中式热回收迴路为贝加莫等城市的区域供热系统提供热能,则可提高电源使用效率 (PUE)。同时,地方政府正在推广综合分区规划,以最大限度地减少土地利用衝突。因此,向更大规模园区发展的趋势强化了长期土地购买策略,尤其是在Lombardia和Piemonte地区,这些地区已具备高速公路和暗纤线路。在此背景下,预计未来五年义大利资料中心市场(就大型计划而言)将成长约四倍,其新建设资本配置将超过中型资料中心。

预计到2025年,四级设施将占总收入的55.05%,年复合成长率达30.20%,这反映了企业对可同时维护的基础设施的需求。金融机构、通讯业者和公共部门机构都需要采用2N+1架构,配备双132kV电源、72小时柴油日用储槽和完全弹性的冷却迴路。三级设施的建造成本比四级设施低15%,但仅限于灾害復原应用和第三方託管非关键工作负载。一级和二级设施则针对本地内容快取和工厂资料转储等特定边缘场景。

预计2026年推出的监管改革可能会将公共云端提供者与政府签订合约的运作要求写入法律,实际上强制要求获得Tier 4认证。这一前景预计将进一步推动投资向最高层级倾斜,到2027年,Tier 4在义大利资料中心市场的份额将达到约60%。由于大多数关键任务型应用无法容忍每年超过五分钟的停机时间,因此需求仍然缺乏弹性。因此,专注于Tier 4架构的供应商将获得定价权,而Tier 3供应商则需要增加收入来源,例如资安管理服务,才能保持竞争力。

意大利数据中心市场报告按数据中心规模(大型、超大型、中型、巨型、小规模)、等级(Tier 1-2、Tier 3、Tier 4)、数据中心类型(超大规模/自建、企业/边缘、託管)、最终用户(银行、金融服务和保险 (BFSI)、IT 和 ITES、电子商务、政府、製造业、媒体和娱乐、电信等)以及热点进行细分。市场预测以 IT 负载容量(兆瓦,MW)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 超大规模资料中心业者加速云端扩张

- 基于PNRR的公共部门云端迁移

- 人工智慧驱动的高密度运算需求

- 战略性海底到陆地连接升级

- 区域供热製冷中余热回收的现状

- 现有设施(棕地)和地下场地的再利用

- 市场限制

- 电力成本上涨和电网限制

- 监管方面的不确定性和审批程序的延误

- 保障水资源安全与限製冷却

- 国内用于大规模建设的资金有限

- 市场展望

- IT负载能力

- 高架楼层面积

- 託管收入

- 预装机架

- 机架空间利用率

- 海底电缆

- 主要行业趋势

- 智慧型手机用户数量

- 每部智慧型手机的数据流量

- 行动资料通讯速度

- 宽频资料通讯速度

- 光纤连接网路

- 法律规范

- 价值炼和通路分析

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(兆瓦)

- 按资料中心规模

- 大规模

- 大规模

- 中号

- 百万

- 小规模

- 依层级类型

- 一级和二级

- 三级

- 第四级

- 依资料中心类型

- 超大规模/内部建设

- 企业/边缘运算

- 搭配

- 未使用的

- 运作中

- 零售共址

- 批发託管

- 最终用户

- BFSI

- 资讯科技与资讯科技服务

- 电子商务

- 政府机构

- 製造业

- 媒体与娱乐

- 沟通

- 其他最终用户

- 透过热点

- 米兰

- 热那亚

- 义大利其他地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Telecom Italia SpA

- IBM Corporation

- Data4 Group SAS

- Google LLC

- Microsoft Corporation

- Retelit SpA

- STACK Infrastructure, Inc.

- CloudHQ, LLC

- Vantage Data Centers, LLC

- ReeVo SpA

- Equinix, Inc.

- Aruba SpA

- Cloudflare, Inc.

- Eni SpA

- Oracle Corporation

- Digital Realty Trust, Inc.

- Amazon Web Services, Inc.

- CyrusOne LLC

- Iron Mountain Inc.

- Irideos SpA

第七章 市场机会与未来展望

The Italy Data Center market is expected to grow from USD 7.54 billion in 2025 to USD 8.45 billion in 2026 and is forecast to reach USD 14.97 billion by 2031 at 12.12% CAGR over 2026-2031.

In terms of IT load capacity, the market is expected to grow from 1.08 thousand megawatt in 2025 to 4.09 thousand megawatt by 2030, at a CAGR of 30.49% during the forecast period (2025-2030). The market segment shares and estimates are calculated and reported in terms of MW. Hyperscale cloud expansion, aggressive public sector digitalization programs, and rising AI-driven computing needs fuel demand. Milan's proximity to trans-European fiber routes, improvements in power procurement, and a growing pipeline of submarine cables keep the country attractive for high-density builds. International investors also favor Italy because land and power are still easier to secure than in Frankfurt, London, Amsterdam, Paris and Dublin. Heightened merger activity suggests the market could enter a consolidation phase as scale economies become decisive.

Italy Data Center Market Trends and Insights

Accelerated Hyperscaler Cloud Expansion

Italy is now a top-tier destination for global cloud providers that need capacity relief from congested Northern European hubs. Microsoft earmarked EUR 4.3 billion (USD 4.6 billion) for new Lombardy facilities that will bring multiple availability zones online by 2027. Google Cloud opened twin regions in Milan and Turin, spanning six buildings to meet local data-residency requirements. Amazon Web Services is evaluating former Enel power-plant sites such as Montalto di Castro to condense permitting timelines and leverage existing transmission links. The influx of foreign capital lifts construction standards, accelerates adoption of liquid cooling, and pushes bulk-power engagement with Terna, the national grid operator.

Public Sector Cloud Migration Under PNRR

Italy's EUR 191.5 billion Recovery and Resilience Plan accelerated nationwide digital transformation. The National Strategic Hub (Polo Strategico Nazionale) awarded contracts worth EUR 520 million in 2024, representing a 73% year-over-year increase, to migrate ministerial workloads to sovereign clouds. The initiative obliges data to remain on domestic soil, favoring Tier 4 sites with quantum-safe encryption and 99.995% uptime. TIM committed EUR 130 million (USD 141 million) for a 25 MW facility near Rome, scheduled for completion in late 2026, specifically designed for GPU clusters. As municipalities seek compliance, demand is emerging for smaller edge nodes across public hospitals and schools.

High Electricity Costs and Grid Constraints

Italian wholesale power averaged EUR 133/MWh (USD 144/MWh) in 2024, 30% higher than France and 40% above Spain, eroding operating margins. Terna received 42 GW of connection requests by March 2025, dwarfing current generation reserves and exposing capacity shortfalls. Renewable approvals are sluggish: regions cleared only 1% of solar applications filed in 2022. For the Italy data center market, operators must therefore sign multi-year renewable PPAs, invest in on-site batteries, and phase construction to match sub-station upgrades.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven High-Density Compute Demand

- Strategic Submarine and Terrestrial Connectivity Upgrades

- Regulatory Uncertainty and Permitting Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The large-facility tier led the Italy data center market with 46.45% revenue in 2025. Operators such as Digital Realty and Aruba use these sites to cluster wholesale colocation suites and multi-tenant cloud nodes. Meanwhile, massive campuses above 60 MW are set to post a 29.10% CAGR through 2031 as hyperscale clouds migrate AI training workloads in-house. The resulting construction swing is visible around Milan's eastern ring road, where three projects totaling 350 MW broke ground in 2025. Utility-scale footprints justify private 150 kV grid connections and on-site substations that mitigate volatile transmission tariffs. Small facilities decline steadily because edge use cases can be served from modular annexes attached to factories or telecom central offices.

Acceleration toward larger footprints compresses the total cost of ownership. Spreading power infrastructure over more racks lowers capex per kW by up to 25% and improves PUE through centralized heat-recovery loops that feed district heating in towns like Bergamo. At the same time, local municipalities favor consolidated zoning to minimize land-use conflicts. The momentum toward massive campuses, therefore, reinforces long-term land banking strategies, especially in Lombardy and Piedmont, where motorway access and dark fiber routes already exist. Within this context, the Italy data center market size for massive projects is positioned to expand almost fourfold over five years, eclipsing medium-tier deployments in new-build capex.

Tier 4 facilities held 55.05% of 2025 revenue and are forecast for a 30.20% CAGR, reflecting enterprise appetite for concurrent-maintainable infrastructure. Financial institutions, telecom operators, and public-sector entities all specify 2N+1 architectures with dual 132 kV feeds, diesel day-tanks sized for 72 hours, and fully fault-tolerant cooling loops. Tier 3 sites, though cheaper by 15% in build cost, remain relegated to disaster-recovery roles or third-party hosting of non-critical workloads. Tier 1-2 installations fill niche edge scenarios such as local content caches or factory data dumps.

Regulatory reforms anticipated for 2026 may codify uptime requirements for public cloud providers serving government contracts, effectively mandating Tier 4 certification. This prospect further tilts investment toward the highest tier and is expected to push the Italy data center market share of Tier 4 to approximately 60% by 2027. Demand elasticity is low because most mission-critical applications cannot tolerate more than five minutes of annual downtime. Accordingly, vendors focusing on Tier 4 builds gain pricing power, while Tier 3 operators need to add revenue streams such as managed security services to stay competitive.

The Italy Data Center Market Report is Segmented by Data Center Size (Large, Massive, Medium, Mega, and Small), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-built, Enterprise/Edge, and Colocation), End User (BFSI, IT and ITES, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom, and More), and Hotspot. The Market Forecasts are Provided in Terms of IT Load Capacity (MW).

List of Companies Covered in this Report:

- Telecom Italia S.p.A.

- IBM Corporation

- Data4 Group S.A.S.

- Google LLC

- Microsoft Corporation

- Retelit S.p.A.

- STACK Infrastructure, Inc.

- CloudHQ, LLC

- Vantage Data Centers, LLC

- ReeVo S.p.A.

- Equinix, Inc.

- Aruba S.p.A.

- Cloudflare, Inc.

- Eni S.p.A.

- Oracle Corporation

- Digital Realty Trust, Inc.

- Amazon Web Services, Inc.

- CyrusOne LLC

- Iron Mountain Inc.

- Irideos S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated hyperscaler cloud expansion

- 4.2.2 Public sector cloud migration under PNRR

- 4.2.3 AI-driven high-density compute demand

- 4.2.4 Strategic submarine and terrestrial connectivity upgrades

- 4.2.5 District heating waste-heat recovery adoption

- 4.2.6 Brownfield and underground site repurposing

- 4.3 Market Restraints

- 4.3.1 High electricity costs and grid constraints

- 4.3.2 Regulatory uncertainty and permitting delays

- 4.3.3 Water availability and cooling restrictions

- 4.3.4 Limited domestic capital for large-scale builds

- 4.4 Market Outlook

- 4.4.1 IT Load Capacity

- 4.4.2 Raised Floor Space

- 4.4.3 Colocation Revenue

- 4.4.4 Installed Racks

- 4.4.5 Rack Space Utilization

- 4.4.6 Submarine Cable

- 4.5 Key Industry Trends

- 4.5.1 Smartphone Users

- 4.5.2 Data Traffic Per Smartphone

- 4.5.3 Mobile Data Speed

- 4.5.4 Broadband Data Speed

- 4.5.5 Fiber Connectivity Network

- 4.5.6 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (MEGAWATT)

- 5.1 By Data Center Size

- 5.1.1 Large

- 5.1.2 Massive

- 5.1.3 Medium

- 5.1.4 Mega

- 5.1.5 Small

- 5.2 By Tier Type

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 By Data Center Type

- 5.3.1 Hyperscale / Self-built

- 5.3.2 Enterprise / Edge

- 5.3.3 Colocation

- 5.3.3.1 Non-Utilized

- 5.3.3.2 Utilized

- 5.3.3.2.1 Retail Colocation

- 5.3.3.2.2 Wholesale Colocation

- 5.4 By End User

- 5.4.1 BFSI

- 5.4.2 IT and ITES

- 5.4.3 E-Commerce

- 5.4.4 Government

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Telecom

- 5.4.8 Other End Users

- 5.5 By Hotspot

- 5.5.1 Milan

- 5.5.2 Genova

- 5.5.3 Rest of Italy

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Telecom Italia S.p.A.

- 6.4.2 IBM Corporation

- 6.4.3 Data4 Group S.A.S.

- 6.4.4 Google LLC

- 6.4.5 Microsoft Corporation

- 6.4.6 Retelit S.p.A.

- 6.4.7 STACK Infrastructure, Inc.

- 6.4.8 CloudHQ, LLC

- 6.4.9 Vantage Data Centers, LLC

- 6.4.10 ReeVo S.p.A.

- 6.4.11 Equinix, Inc.

- 6.4.12 Aruba S.p.A.

- 6.4.13 Cloudflare, Inc.

- 6.4.14 Eni S.p.A.

- 6.4.15 Oracle Corporation

- 6.4.16 Digital Realty Trust, Inc.

- 6.4.17 Amazon Web Services, Inc.

- 6.4.18 CyrusOne LLC

- 6.4.19 Iron Mountain Inc.

- 6.4.20 Irideos S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

2026年全球智慧客户资料中心市场报告2026年全球网路资料中心(IDC)市场报告2026年全球资料中心房地产市场报告

2026年全球智慧客户资料中心市场报告2026年全球网路资料中心(IDC)市场报告2026年全球资料中心房地产市场报告 资料中心市场:按组件、资料中心类型、层级、冷却方式、电源、最终用户和组织规模划分-2026年至2032年全球市场预测

资料中心市场:按组件、资料中心类型、层级、冷却方式、电源、最终用户和组织规模划分-2026年至2032年全球市场预测 全球在轨资料中心市场预测(至2034年)-按平台、组件、系统、连接类型、应用、最终用户和地区分類的分析

全球在轨资料中心市场预测(至2034年)-按平台、组件、系统、连接类型、应用、最终用户和地区分類的分析 资料中心汇流排市场规模、份额和成长分析:按导体材料、绝缘类型、额定功率、安装/整合方法、资料中心类型和地区划分-2026-2033年产业预测2026年全球客製化资料中心市场报告

资料中心汇流排市场规模、份额和成长分析:按导体材料、绝缘类型、额定功率、安装/整合方法、资料中心类型和地区划分-2026-2033年产业预测2026年全球客製化资料中心市场报告 资料中心能源概况 - Oracle:自 2019 年以来,能源使用量以 24% 的复合年增长率成长,由于可再生能源的使用,排放保持稳定,但 Stargate 专案可能会大幅增加碳足迹。

资料中心能源概况 - Oracle:自 2019 年以来,能源使用量以 24% 的复合年增长率成长,由于可再生能源的使用,排放保持稳定,但 Stargate 专案可能会大幅增加碳足迹。 氢动力资料中心市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、功能、安装模式资料中心市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、解决方案

氢动力资料中心市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、功能、安装模式资料中心市场分析及预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署模式、最终用户、解决方案