|

市场调查报告书

商品编码

1911453

电动装置:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Electric Drives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

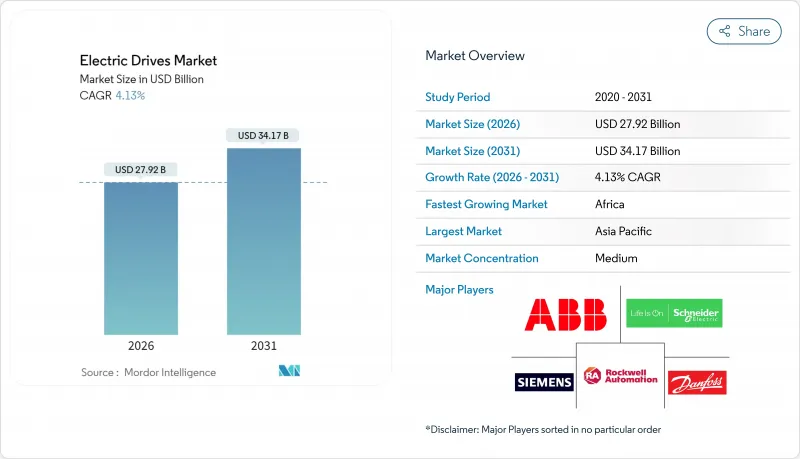

预计到 2026 年,电动装置市场规模将达到 279.2 亿美元,高于 2025 年的 268.1 亿美元。

预计到 2031 年将达到 341.7 亿美元,2026 年至 2031 年的复合年增长率为 4.13%。

成长主要由三大支柱驱动:强制性能源效率法规推动变频技术的普及、电动车线路对高精度操作的需求,以及现有设备的维修以降低营运成本。亚太地区将在2024年以45.64%的收入份额引领市场,这主要得益于中国工厂的规模优势和印度不断扩大的工业基础。同时,非洲将以5.46%的复合年增长率成为成长最快的地区,这主要得益于采矿业和基础设施投资。儘管空调机组以71.13%的市场份额占据主导地位,但伺服驱动器的成长速度最快,复合年增长率达4.47%,这反映了离散製造业对微米级定位的需求。随着重型工业业者对其压缩机和泵浦设备进行现代化改造,中压计划也以4.81%的复合年增长率加速成长。

全球电动装置市场趋势与洞察

严格的全球和国家能源效率法规

美国、欧洲和中国的新法规提高了马达的最低能效标准,实际上强制要求高能耗工厂安装变频驱动装置。工业审核发现,马达消耗的电力占生产用电量的70%之多,因此,更换定速启动器可以显着排放碳排放并节省成本。各国政府目前将认证驱动装置器维修的性能与税收优惠和补贴计画挂钩,使得对认证产品的需求更加可预测。供应商也积极回应,将驱动器与能源评估软体捆绑销售,以量化三年或更短时间内的投资回收期。因此,在政策强制执行的支持下,电动装置市场正经历持续的更新週期。

加速电动车生产线建设,需要高精度驱动装置

电动车工厂的电池组装、马达绕线和品管控制站需要小于0.1毫米的重复精度,这使得伺服驱动器成为生产线设计的核心组成部分。汽车製造商在电气化领域投资超过1000亿美元,新建工厂从一开始就指定采用先进的运动控制封装。即使是对现有内燃机工厂的维修,也在以基于伺服的柔性单元取代传统的输送机。伺服供应商透过增加整合安全功能和分散式I/O来加速即插即用技术的应用,从而简化协作机器人的整合。持续不断的资金流入使电动装置市场稳居电动车投资的主要受益者之列。

与固定速度替代方案的初始资本投资比较

变频驱动器的成本是接触器启动器的三到五倍,这使得资本投资成为融资紧张的工厂的一大障碍。三年或更短的投资回收期对精明的业者来说颇具吸引力,但即便电力补贴政策实施,许多业者仍会推迟升级。这种担忧在15kW以下的功率范围内尤其突出,因为该功率范围内的绝对节能效果有限,且盈亏平衡时间更长。驱动器租赁和能源即服务等资金筹措方案正在兴起,但在北美和西欧以外的地区仍然有限。随着时间的推移,半导体价格的下降和公用事业公司的奖励可能会降低这些门槛,并扩大电动装置市场的潜在需求。

细分市场分析

到2025年,交流驱动器将占据电动装置市场70.62%的份额,这反映了其在泵浦、风机和输送机线等全球工厂自动化基础应用的广泛适用性。标准化的介面、成熟的零件供应链以及安装人员丰富的知识储备支撑着市场需求,尤其是在食品加工和供水事业领域,这些领域对可靠性的要求高于现有技术水平。随着公用事业公司在预测期内持续提高离心设备的能源效率目标,电动装置市场将继续依赖交流电平台进行基础马达控制。伺服驱动器仍将是成长最快的细分市场,到2031年将以4.25%的复合年增长率成长,这主要得益于离散製造厂对电池、电子产品和医疗设备组装中亚微米定位的需求。伺服驱动器供应商目前正透过捆绑整合安全功能和单电缆网路来区别于同质化的交流驱动器。

电动装置市场正受惠于技术交叉融合,伺服演算法正逐步迁移至高阶交流封装。这模糊了传统产品线的界限,同时为中阶市场用户保持了极具吸引力的成本优势。直流驱动器曾一度在金属和采矿领域占据主导地位,但随着现代交流向量控制系统在提供同等扭矩精度的同时降低维护成本,直流驱动器的市场份额正在下降。然而,一些轧延运营商仍然出于兼容旧系统的目的而指定使用直流驱动器,从而产生了小规模的升级需求。将交流、伺服和直流轴整合于单一机架中的多驱动平台正日益普及,尤其是在重视跨运动类别统一程式设计的机械製造商OEM中。这种融合为主要供应商带来了全生命週期业务收益,并巩固了整个电动装置市场的适度集中度。

2025年,1kV以下的低压系统将占总收入的62.98%,为大多数工厂的泵浦、压缩机和物料输送线提供动力。易于安装、塑壳保护装置的普及以及技术人员技能的广泛应用,使得整体拥有成本保持在较低水平,从而确保了标准製造领域的电动装置市场将继续专注于低压领域。然而,成长将更转向中压应用,预计到2031年,随着重工业营运商将大型马达升级为变速运行,中压应用市场将以4.62%的复合年增长率成长。

当泵浦或压缩机的耗电量超过2兆瓦时,中压计划通常会应运而生,无论是棕地的扩建,或是液化天然气工厂、水泥厂或待开发区厂等新建工程的建设。营运商青睐这些解决方案,因为与并联多个低压马达相比,它们能够提高功率因数并降低电缆损耗。准两电平逆变器拓扑结构、碳化硅元件和能量再生功能如今已成为高阶中压马达组件的差异化优势,帮助供应商获得更高的利润。谐波抑制和併网辅助模式等电网介面功能与矿山和偏远油田新兴的微电网计画相契合,提升了电网的韧性价值。因此,电机市场正变得日益两极化。商品化的低压产品维持着市场规模,而技术先进的中压马达则创造了不成比例的利润。

区域分析

到2025年,亚太地区仍将保持其在电动装置市场的最大份额(45.10%),这主要得益于中国2024年500亿美元的自动化投资以及印度奖励政策推动的工厂扩张。中国企业持续以变速封装取代传统起动器,以满足最新的能源效率标准。在长三角Delta超级工厂集群中,伺服的应用正在加速。印度的生产连结奖励计画计画正在促进白色家电的在地化生产,刺激了对钣金压平机和射出成型机等中檔伺服马达的需求。日本和韩国保持技术主导地位,为协作机器人单元和半导体工厂采购先进的人工智慧驱动系统。同时,东南亚国家正在从基于检测的自动化单元转型为全规模生产线。这些协同效应巩固了该地区在电动装置市场的主导地位。

在北美,现有工厂的维修需求稳定,驱动装置的升级改造正在推进,以符合美国能源局的电机法规并利用需量反应电力折扣。汽车产业重返五大湖地区,推动了伺服的新订单,印证了离散製造业中电动装置市场的规模。加拿大矿业正在为其钾镍矿扩建项目引入中压封装。一家墨西哥一级汽车零件製造商为其变速箱壳体加工中心指定了安全整合伺服。同时,预测性维护云端平台的发展趋势正在推动国内软体生态系统的发展,建构起将数位服务与硬体交付结合的全新格局。

欧洲是一个成熟且充满创新精神的地区,其工业4.0蓝图和欧洲绿色交易正在推动变速技术的应用。德国自动化设备出口商要求采用同步磁阻驱动装置以降低磁性材料风险;义大利机械製造商正在整合网路安全韧体以保护智慧财产权;北欧的加工厂正在采用再生驱动装置以增强以可再生能源为主的电网。非洲虽然面积较小,但预计到2031年将以5.26%的复合年增长率实现最快增长,这主要得益于南非矿山对运输卡车的电气化改造以及尼日利亚水泥压机采用中压逆变器。欧洲製造商也将劳力密集流程转移到北非,从而推动伺服在当地的应用。这些趋势共同作用,使区域收入来源多元化,并稳定了电动装置市场的长期成长轨迹。

其他福利

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 宏观经济因素的影响

- 市场驱动因素

- 製程製造和离散製造中心的快速工业化

- 严格的国际和国家能源效率法规

- 加速电动车生产线建设,需要高精度驱动装置

- 数位化维修-在现有设备中引入变速驱动器以节省能源

- 透过基于人工智慧的预测性维护减少驱动装置停机时间

- 向无稀土元素拓朴结构(轴向磁通、开关磁阻)的过渡

- 市场限制

- 与固定速度方案相比,初始资本投入较高

- 恶劣运转环境与高谐波环境下的可靠性问题

- 电力电子和磁铁供应链波动性

- 互联智慧驾驶中的网路安全漏洞

- 产业生态系分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 副产品

- 交流驱动

- 直流驱动器

- 伺服驱动器

- 透过电压

- 低压驱动

- 中压驱动

- 按额定输出

- 250千瓦或以下

- 251~500kW

- 500千瓦或以上

- 按最终用户行业划分

- 石油和天然气

- 用水和污水

- 化工/石油化工

- 饮食

- 发电

- HVAC

- 纸浆和造纸

- 离散产业

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 义大利

- 英国

- 法国

- 西班牙

- 其他欧洲

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ABB Ltd.

- Siemens AG

- Danfoss A/S

- Rockwell Automation Inc.

- Schneider Electric SE

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Nidec Corporation

- SEW-EURODRIVE GmbH and Co KG

- TMEIC Corporation

- WEG SA

- Hitachi Ltd.

- Fuji Electric Co. Ltd.

- Eaton Corporation plc

- Emerson Electric Co.

- Toshiba International Corporation Inc.

- Parker Hannifin Corporation

- Regal Rexnord Corporation

- Johnson Electric Holdings Limited

- Bonfiglioli Riduttori SpA

第七章 市场机会与未来展望

electric drives market size in 2026 is estimated at USD 27.92 billion, growing from 2025 value of USD 26.81 billion with 2031 projections showing USD 34.17 billion, growing at 4.13% CAGR over 2026-2031.

Growth rests on three pillars: mandatory efficiency rules that push variable-speed adoption, e-mobility lines demanding high-precision motion, and brownfield retrofits aimed at slashing utility bills. Asia Pacific leads with 45.64% revenue share in 2024 because of China's factory scale and India's expanding industrial base, while Africa registers the fastest 5.46% CAGR on the back of mining and infrastructure spending. AC units deliver the bulk of shipments at 71.13% share, yet servo drives advance the quickest at a 4.47% CAGR, mirroring discrete manufacturing's need for micron-level positioning. Medium-voltage projects also pick up pace, logging a 4.81% CAGR as heavy-industry operators modernize compressor and pump assets.

Global Electric Drives Market Trends and Insights

Stringent Global and National Energy-Efficiency Mandates

New U.S., European and Chinese rules elevate minimum motor efficiency levels, effectively compelling variable-frequency drive adoption in energy-intensive plants. Industrial audits show motors consuming up to 70% of manufacturing electricity, so replacing fixed-speed starters yields sizable carbon and cost savings. Governments now link tax incentives and grant programs to verified drive retrofits, creating predictable demand for certified products. Vendors respond by packaging drives with energy-assessment software that quantifies payback in under three years. As a result, the electric drives market gains a durable replacement cycle anchored in policy enforcement.

Acceleration of E-Mobility Production Lines Needing High-Precision Drives

Battery assembly, motor winding and quality-control stations in electric-vehicle plants require sub-0.1 millimeter repeatability, placing servo drives at the heart of line design Automotive OEMs have committed more than USD 100 billion toward electrification, and each greenfield factory specifies advanced motion packages from day one. Brownfield retrofits of internal-combustion plants also replace legacy conveyors with servo-based flexible cells. Servo vendors add integrated safety and decentralized I/O to simplify robot collaboration, accelerating plug-and-play deployment. This continuous capital flow cements the electric drives market as a primary beneficiary of e-mobility investment.

High Initial Capex Versus Fixed-Speed Alternatives

Variable-frequency drives cost three to five times more than contactor starters, making capex a hurdle in cash-constrained plants. Payback periods under three years appeal to financially savvy operators, yet many still defer upgrades when electricity is subsidized. The objection is acute in sub-15 kW ranges where absolute savings are modest, extending breakeven timelines. Financing options such as drive-leasing or energy-as-a-service are emerging but remain scarce outside North America and Western Europe. Over time, falling semiconductor prices and utility incentives may ease the barrier, widening addressable demand in the electric drives market.

Other drivers and restraints analyzed in the detailed report include:

- Digital Retrofits - Variable-Speed Drives for Brownfield Energy Savings

- AI-Enabled Predictive Maintenance Reducing Downtime of Drive Systems

- Cyber-Security Vulnerabilities in Network-Connected Smart Drives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AC drives held a dominant 70.62% electric drives market share in 2025, reflecting their versatility in pumps, fans and conveyor lines that underpin global factory automation. Standardized interfaces, mature component supply chains and broad installer familiarity sustain demand, particularly in food processing and water utilities where reliability trumps cutting-edge performance. Over the forecast horizon, the electric drives market will continue to rely on AC platforms for baseline motor control as utilities tighten efficiency targets in centrifugal equipment. Servo drives remain the fastest-growing niche with a 4.25% CAGR through 2031 thanks to discrete manufacturing plants that require sub-micrometer positioning in battery, electronics and medical-device assembly. Servo vendors now bundle integrated safety functions and one-cable networks, distinguishing their premium offerings from commoditized AC units.

The electric drives market benefits from a technology crossover as servo algorithms migrate into high-end AC packages, blurring historic product lines while keeping cost curves attractive for mid-tier users. DC drives, once favored in metals and mining, now occupy shrinking pockets because modern AC vector control replicates their torque fidelity at lower maintenance cost. Yet some rolling-mill operators still specify DC units for legacy compatibility, providing a modest replacement stream. Multi-drive platforms that combine AC, servo and DC axes in a single rack are gaining attention, especially among machine-builder OEMs that value unified programming across motion classes. This convergence supports life-cycle service revenues for top suppliers, reinforcing moderate concentration in the broader electric drives market.

Low-voltage systems below 1 kV accounted for 62.98% of 2025 revenue, underpinning most factory pumps, compressors and material-handling lines. Installation simplicity, ready availability of molded-case protection gear and widespread technician skill sets keep total ownership cost low, ensuring that the electric drives market retains a low-voltage core in standard manufacturing. Growth nonetheless skews toward medium-voltage equipment, which is projected to advance at a 4.62% CAGR through 2031 as heavy-industry operators upgrade large motors to variable-speed duty.

Medium-voltage projects typically surface during brownfield capacity expansions or greenfield investments in LNG, cement and desalination plants, where pumps or compressors exceed 2 MW. Operators favor these solutions for improved power factor and reduced cable losses relative to running multiple low-voltage motors in parallel. Quasi-two-level inverter topologies, silicon-carbide devices and regenerative capabilities now differentiate premium medium-voltage packages, helping suppliers justify higher margins. Utility-interactive features such as harmonic mitigation and grid-support modes align with nascent microgrid programs in mining and remote oilfields, adding resilience value. As a result, the electric drives market sees a bifurcation: commoditized low-voltage volumes sustain scale while technologically sophisticated medium-voltage units generate disproportionate profit pools.

The Electric Drives Market Report is Segmented by Product (AC Drives, DC Drives, and Servo Drives), Voltage (Low-Voltage Drive, and Medium-Voltage Drive), Power Rating (Less Than 250 KW, 251-500 KW, and More Than 500 KW), End-User Industry (Oil and Gas, Water and Wastewater, Chemical and Petrochemical, Food and Beverage, Power Generation, HVAC, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific retained the largest share of the electric drives market in 2025 at 45.10%, sustained by China's USD 50 billion 2024 automation spend and India's incentive-backed factory build-out. Chinese enterprises continue to replace legacy starters with variable-speed packages to satisfy the country's latest energy-intensity mandate, while servo adoption accelerates in battery-gigafactory clusters along the Yangtze River Delta. India's Production Linked Incentive scheme drives localized manufacturing of whitegoods, spurring mid-range servo demand in sheet-metal presses and injection-molding machines. Japan and South Korea remain technology front runners, purchasing premium AI-enabled drives for collaborative robot cells and semiconductor fabs, whereas Southeast Asian nations advance from pilot automation cells to full production lines. These combined activities cement regional primacy in the electric drives market.

North America delivers steady replacement demand as brownfield plants retrofit drives to meet U.S. DOE motor rules and leverage utility rebates for demand-response. Automotive reshoring initiatives around the Great Lakes trigger fresh servo orders, underscoring the electric drives market size within discrete manufacturing. Canada's mining sector deploys medium-voltage packages in potash and nickel expansions, while Mexico's tier-one automotive suppliers specify safety-integrated servos for transmission-housing machining centers. A parallel trend toward predictive-maintenance cloud platforms favors domestic software ecosystems, ensuring that digital services layer atop hardware shipments.

Europe represents a mature yet innovation-driven arena where Industry 4.0 roadmaps and the European Green Deal reinforce variable-speed penetration. German automation exporters demand synchronous-reluctance drives to trim magnet material risk, Italian machinery OEMs embed cyber-secure firmware to protect intellectual property, and Nordic process plants adopt regenerative drives to bolster renewable-heavy grids. Africa, although holding a smaller base today, records the fastest 5.26% CAGR to 2031 as South African mines electrify haul trucks and Nigerian cement presses install medium-voltage inverters. European manufacturers relocating labor-intensive stages to North Africa also lift localized servo uptake. Collectively, these patterns diversify regional revenue streams, stabilizing the long-term trajectory of the electric drives market.

- ABB Ltd.

- Siemens AG

- Danfoss A/S

- Rockwell Automation Inc.

- Schneider Electric SE

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Nidec Corporation

- SEW-EURODRIVE GmbH and Co KG

- TMEIC Corporation

- WEG S.A.

- Hitachi Ltd.

- Fuji Electric Co. Ltd.

- Eaton Corporation plc

- Emerson Electric Co.

- Toshiba International Corporation Inc.

- Parker Hannifin Corporation

- Regal Rexnord Corporation

- Johnson Electric Holdings Limited

- Bonfiglioli Riduttori S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors

- 4.3 Market Drivers

- 4.3.1 Rapid industrialisation in process and discrete manufacturing hubs

- 4.3.2 Stringent global and national energy-efficiency mandates

- 4.3.3 Acceleration of e-mobility production lines needing high-precision drives

- 4.3.4 Digital retrofits - variable-speed drives for brownfield energy savings

- 4.3.5 AI-enabled predictive maintenance reducing downtime of drive systems

- 4.3.6 Shift toward rare-earth-free topologies (axial-flux, switched-reluctance)

- 4.4 Market Restraints

- 4.4.1 High initial capex versus fixed-speed alternatives

- 4.4.2 Reliability concerns in harsh-duty, high-harmonic environments

- 4.4.3 Supply-chain volatility for power-electronic components and magnets

- 4.4.4 Cyber-security vulnerabilities in network-connected smart drives

- 4.5 Industry Ecosystem Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 AC Drives

- 5.1.2 DC Drives

- 5.1.3 Servo Drives

- 5.2 By Voltage

- 5.2.1 Low-Voltage Drive

- 5.2.2 Medium-Voltage Drive

- 5.3 By Power Rating

- 5.3.1 Less than 250 kW

- 5.3.2 251-500 kW

- 5.3.3 Above 500 kW

- 5.4 By End-User Industry

- 5.4.1 Oil and Gas

- 5.4.2 Water and Wastewater

- 5.4.3 Chemical and Petrochemical

- 5.4.4 Food and Beverage

- 5.4.5 Power Generation

- 5.4.6 HVAC

- 5.4.7 Pulp and Paper

- 5.4.8 Discrete Industries

- 5.4.9 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 Italy

- 5.5.3.3 United Kingdom

- 5.5.3.4 France

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Siemens AG

- 6.4.3 Danfoss A/S

- 6.4.4 Rockwell Automation Inc.

- 6.4.5 Schneider Electric SE

- 6.4.6 Yaskawa Electric Corporation

- 6.4.7 Mitsubishi Electric Corporation

- 6.4.8 Nidec Corporation

- 6.4.9 SEW-EURODRIVE GmbH and Co KG

- 6.4.10 TMEIC Corporation

- 6.4.11 WEG S.A.

- 6.4.12 Hitachi Ltd.

- 6.4.13 Fuji Electric Co. Ltd.

- 6.4.14 Eaton Corporation plc

- 6.4.15 Emerson Electric Co.

- 6.4.16 Toshiba International Corporation Inc.

- 6.4.17 Parker Hannifin Corporation

- 6.4.18 Regal Rexnord Corporation

- 6.4.19 Johnson Electric Holdings Limited

- 6.4.20 Bonfiglioli Riduttori S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

OEM电动驱动单元市场机会、成长要素、产业趋势分析及2026-2035年预测

OEM电动驱动单元市场机会、成长要素、产业趋势分析及2026-2035年预测 电气和机械驱动装置市场:2026-2032年全球市场预测(按驱动系统、额定功率、速度范围、最终用户产业、应用和控制系统划分)

电气和机械驱动装置市场:2026-2032年全球市场预测(按驱动系统、额定功率、速度范围、最终用户产业、应用和控制系统划分) BEV电动装置的全球市场

BEV电动装置的全球市场 全球低压电力驱动市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)中东和非洲的电动式驱动:市场占有率分析、产业趋势和成长预测(2025-2030)亚太地区电动驱动:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)交流 (AC) 电力驱动器:市场占有率分析、行业趋势和成长预测(2025-2030 年)全球直流 (DC) 电力驱动市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)北美电动驱动器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)拉丁美洲电力驱动:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

全球低压电力驱动市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)中东和非洲的电动式驱动:市场占有率分析、产业趋势和成长预测(2025-2030)亚太地区电动驱动:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)交流 (AC) 电力驱动器:市场占有率分析、行业趋势和成长预测(2025-2030 年)全球直流 (DC) 电力驱动市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)北美电动驱动器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)拉丁美洲电力驱动:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)