|

市场调查报告书

商品编码

1934831

新加坡资讯通信技术:市场份额分析、产业趋势与统计、成长预测(2026-2031)Singapore ICT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

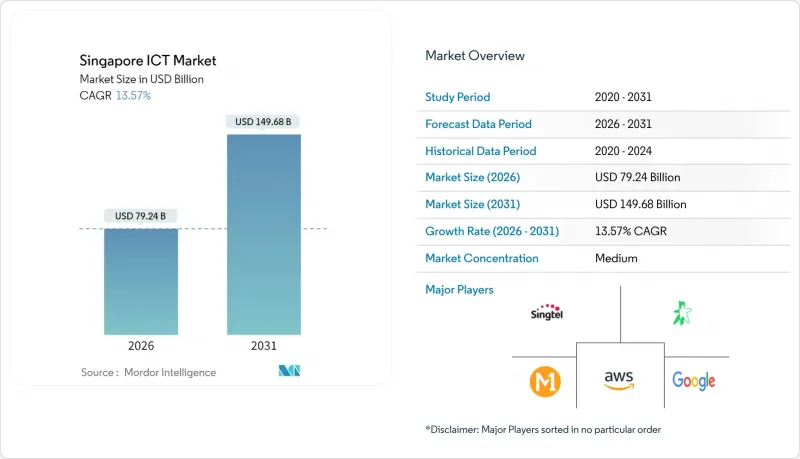

预计新加坡资讯通信技术市场将从 2025 年的 697.7 亿美元成长到 2026 年的 792.4 亿美元,到 2031 年将达到 1,496.8 亿美元,2026 年至 2031 年的复合年增长率为 13.57%。

新加坡的快速成长资金筹措、超大规模资料中心投资以及企业加速向云端和人工智慧平台迁移。跨国云端服务供应商竞相扩大本地容量,而中小企业则利用软体即服务(SaaS)来缩小与大型企业的能力差距。医疗数位数位化、纯数位银行牌照的发放以及国家人工智慧运算资源中心(NACR)的推出,旨在降低高阶分析的门槛,这些因素也推动了产业发展。然而,不断增长的支出与有限的电网容量和日益严重的网路安全人才短缺形成鲜明对比,导致营运成本上升和计划前置作业时间延长。

新加坡资讯通信技术市场趋势与洞察

政府主导的智慧国家支出激增

新加坡的「智慧国家2.0」计画将推动其从数位化应用迈向数位化管治,并承诺在2024年投入33亿美元用于网路安全、数据平台和现代化基础设施建设。这笔支出将加速分析引擎、边缘设备和即时处理工具的采购,刺激公共部门以外的广泛需求。反映这些标准的监管要求正迫使私营机构,尤其是金融和医疗保健行业的机构,更新其旧有系统。专注于API编配和跨平台安全的供应商将能够直接赢得大规模期合同,而互通框架将减少跨行业整合的摩擦。

云端优先公司政策

云端优先策略改变了基础架构规划,云端工作负载成长了 17.7%,而本地部署仅成长了 11.2%。多重云端策略正在推动价值 35 亿美元的国内云端市场发展,因为它们可以减少厂商锁定并满足资料主权法规的要求。中小企业 (SME) 的采用速度最快,他们利用基于订阅的 AI、分析和自动化功能来实现企业级功能。此外,对统一监控仪表板、混合连接平台和自动化策略管治的需求也不断增长,以确保分散式环境的合规性。

熟练数位人才短缺

网路安全专业人员短缺2800至4400人,导致部署进度延误,人事费用上升。同时,预计到2029年,安全需求将达到48.2亿美元。人工智慧工程师和云端架构师的短缺也同样存在,迫使中小企业与跨国公司展开薪资竞争。政府支持的技能培训项目,例如IBM的SkillsBuild项目(涵盖4500名学员),只能逐步缓解此短缺问题。因此,企业正在转向低程式码平台、人工智慧辅助开发和託管服务,以减少对稀缺专家的依赖。

细分市场分析

到2025年, IT基础设施将占新加坡ICT市场规模的25.86%,这显示市场对资料中心、网路设备和伺服器容量的投资将持续成长。 AWS的120亿美元超大规模扩张计画等措施正在推动这一领域的成长,但由于虚拟化带来的伺服器机架密度增加,其年增长率正在放缓。在云端原生平台、人工智慧工具链和工作流程自动化套件的驱动下,IT软体的成长速度超过了其他类别,复合年增长率高达16.35%。这种向软体的转变正在推动对容器编排管理、微服务安全和敏捷整合服务的需求。基础设施和应用程式的并行扩展支撑着一个均衡的成长平台。在企业软体领域,订阅定价模式的日益普及限制了资本支出的激增,并平滑了现金流。在硬体领域,商品化正在缩小利润率,而专用人工智慧加速器和边缘设备则维持着高价。 SAP等主要供应商已在新加坡设立研发中心,其「数位创新加速器」就是一个很好的例子,该加速器将产业专用的人工智慧模式与本地应用案例相结合。高容量基础设施与先进软体的互动形成良性循环,推动新加坡资讯通信技术市场持续成长。

预计到2025年,大型企业将占据新加坡资讯通信技术(ICT)市场66.78%的份额,它们利用自身的预算和内部人才推动复杂的多领域数位化。然而,由于许多公司已经完成了第一阶段的转型,其成长速度正在放缓至12.84%。相较之下,中小企业的复合年增长率(CAGR)高达14.88%,这主要得益于政府补贴和缩短引进週期的云端合约。承包人工智慧服务的日益普及使得小规模企业无需购买昂贵的硬体即可整合聊天机器人、分析工具和机器人流程自动化(RPA)。人才发展倡议正在为中小企业维持数位化人才储备。 IBM的SkillsBuild计画就是一个例子,该计画提供资料分析和网路安全的免费认证课程。诸如生产力解决方案补助金等财政奖励可报销高达70%的符合条件的技术投资,进一步创造了公平的竞争环境。随着中小企业规模的扩大,它们为託管服务供应商和增值转售商提供了重要的基本客群,从而加强了支持新加坡资讯通信技术市场的多元化供应商生态系统。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 市场定义与研究假设

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 政府智慧国家支出激增

- 快速部署和普及5G

- 企业中的云端优先策略

- 数位银行牌照推动了银行、金融服务和保险(BFSI)行业的技术支出。

- 国家人工智慧运算资源(NACR)简介

- 超大规模资料中心的绿色电力激励措施

- 市场限制

- 熟练数位人才短缺

- 扩大网路攻击的目标区域

- 新建资料中心建置面临的电网容量限制

- 因限制外籍劳工政策而导致的工资上涨

- 价值链分析

- 重要法规结构评估

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素的影响

第五章 市场规模与成长预测

- 按类型

- IT硬体

- 电脑硬体

- 网路装置

- 周边设备

- IT软体

- IT服务

- 託管服务

- 业务流程服务

- 商业咨询服务

- 云端服务

- IT基础设施

- 通讯服务

- IT硬体

- 按最终用户公司规模划分

- 小型企业

- 大公司

- 按部署模式

- 本地部署

- 云

- 杂交种

- 按最终用户行业划分

- 政府和公共机构

- BFSI

- 能源与公共产业

- 零售、电子商务与物流

- 製造业和工业4.0

- 医疗保健和生命科学

- 石油和天然气(上游、中游、下游)

- 游戏和电子竞技

- 其他行业

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amazon Web Services(AWS)Singapore

- International Business Machines Corporation(IBM Singapore Pte. Ltd.)

- Cognizant Technology Solutions Asia Pacific Pte. Ltd.

- Micron Semiconductor Asia Operations Pte. Ltd.

- SAP Asia Pte. Ltd.

- Wipro Ltd.(Singapore)

- Hewlett Packard Enterprise Singapore Pte. Ltd.

- Intel Technology Asia Pte. Ltd.

- Singapore Telecommunications Ltd.(Singtel)

- StarHub Ltd.

- M1 Ltd.

- TPG Telecom Pte. Ltd.(SIMBA Telecom)

- NCS Pte. Ltd.

- NEC Asia Pacific Pte. Ltd.

- Dell Technologies Singapore Pte. Ltd.

- Google Asia Pacific Pte. Ltd.

- Microsoft Operations Pte. Ltd.(Microsoft Singapore)

- Equinix Singapore Pte. Ltd.

- Alibaba Cloud(Singapore)Private Limited

- Palo Alto Networks(Singapore)Pte. Ltd.

- Check Point Software Technologies(Singapore)Pte. Ltd.

- Trend Micro(Singapore)Pte. Ltd.

第七章 市场机会与未来趋势

- 评估差距和未满足的需求

The Singapore ICT market is expected to grow from USD 69.77 billion in 2025 to USD 79.24 billion in 2026 and is forecast to reach USD 149.68 billion by 2031 at 13.57% CAGR over 2026-2031.

Singapore's surge pivots on Smart Nation 2.0 funding, hyperscale data-center investments, and accelerated enterprise migration to cloud and AI platforms. Multinational cloud providers are racing to expand local capacity, while small and medium enterprises (SMEs) leverage software-as-a-service to close capability gaps with larger rivals. Sector momentum is also reinforced by healthcare digitalization, digital-only banking licenses, and the National AI Compute Resource (NACR) that lowers barriers to advanced analytics. Heightened spending, however, collides with power-grid limits and a widening cybersecurity talent gap that lifts operating costs and elongate project lead times.

Singapore ICT Market Trends and Insights

Government Smart-Nation Expenditure Surge

Smart Nation 2.0 moves Singapore from digital adoption toward digital-first governance, channeling USD 3.3 billion in fiscal 2024 into cybersecurity, data platforms, and modernized infrastructure. The outlay accelerates procurement of analytics engines, edge devices, and real-time processing tools, catalyzing demand far beyond the public sector. Regulatory requirements that mirror these standards push private organizations, especially in finance and healthcare, to upgrade legacy systems. Vendors specializing in API orchestration and cross-platform security gain direct access to large multi-year contracts, while interoperable frameworks reduce integration friction across verticals.

Enterprise Cloud-first Mandates

Cloud-first policies have flipped infrastructure planning, with cloud workloads growing 17.7% against 11.2% for on-premise deployments. Multi-cloud strategies lessen vendor lock-in and satisfy data-sovereignty rules, prompting a USD 3.5 billion domestic cloud market. SMEs drive the fastest uptake, using subscription-based AI, analytics, and automation to match big-company capabilities. Secondary demand is emerging for unified observability dashboards, hybrid connectivity fabrics, and automated policy governance that keep distributed environments in regulatory compliance.

Scarcity of Skilled Digital Talent

A shortage of 2,800 to 4,400 cybersecurity professionals shackles rollout schedules and elevates salary costs, even as security demand is set to hit USD 4.82 billion by 2029. The gap extends to AI engineers and cloud architects, forcing SMEs to compete with multinationals on compensation. Government-backed upskilling programs, including IBM's SkillsBuild, which targets 4,500 learners, will narrow deficits only gradually. Firms therefore pivot to low-code platforms, AI-assisted development, and managed services that reduce reliance on scarce specialists.

Other drivers and restraints analyzed in the detailed report include:

- Digital Bank Licenses Boost BFSI Tech Spend

- National AI Compute Resource Roll-out

- Escalating Cyber-attack Surface

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IT infrastructure owned 25.86% of Singapore ICT market size in 2025, underlining continued investment in data centers, networking gear, and server capacity . The segment benefits from hyperscale expansion commitments such as AWS's USD 12 billion plan, but year-on-year growth is moderating as virtualization densifies server racks. IT software outpaces all other categories with a 16.35% CAGR, propelled by cloud-native platforms, AI toolchains, and workflow automation suites. This software pivot lifts demand for container orchestration, micro-services security, and agile integration services. Parallel expansion of infrastructure and applications underpins a balanced growth profile. Companies increasingly adopt subscription pricing for enterprise software, flattening capex spikes and smoothing cash flows. Hardware margins tighten amid commoditization, though specialized AI accelerators and edge devices command premiums. Major vendors such as SAP anchor R&D in Singapore, exemplified by its Digital Innovation Accelerator that aligns industry-specific AI models with local use cases . The interplay of high-capacity infrastructure with advanced software creates a virtuous cycle that keeps the Singapore ICT market on its upward trajectory.

Large enterprises held 66.78% of Singapore ICT market share in 2025, leveraging budgets and in-house talent to execute complex, multi-domain digitization. Growth, however, is slowing to 12.84% as many have already completed first-wave transformations. SMEs, in contrast, are posting a 14.88% CAGR, driven by government grants and cloud subscriptions that compress deployment cycles. The widening availability of turnkey AI services empowers small firms to integrate chatbots, analytics, and robotic process automation without owning expensive hardware. Training initiatives keep the pipeline of digital talent flowing to smaller companies. IBM's SkillsBuild is one example that provides free certification tracks for data analytics and cybersecurity . Financial incentives such as the Productivity Solutions Grant reimburse up to 70% of qualifying tech investments, further equalizing adoption conditions. As SMEs scale, they form a sizeable customer base for managed-service providers and value-added resellers, reinforcing a diversified vendor ecosystem that underpins the Singapore ICT market.

The Singapore ICT Market Report is Segmented by Type (IT Hardware, IT Software, and More), End-User Enterprise Size (Small and Medium Enterprises and Large Enterprises), Deployment Model (On-Premise, and More), and End-User Industry (Government and Public Administration, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amazon Web Services (AWS) Singapore

- International Business Machines Corporation (IBM Singapore Pte. Ltd.)

- Cognizant Technology Solutions Asia Pacific Pte. Ltd.

- Micron Semiconductor Asia Operations Pte. Ltd.

- SAP Asia Pte. Ltd.

- Wipro Ltd. (Singapore)

- Hewlett Packard Enterprise Singapore Pte. Ltd.

- Intel Technology Asia Pte. Ltd.

- Singapore Telecommunications Ltd. (Singtel)

- StarHub Ltd.

- M1 Ltd.

- TPG Telecom Pte. Ltd. (SIMBA Telecom)

- NCS Pte. Ltd.

- NEC Asia Pacific Pte. Ltd.

- Dell Technologies Singapore Pte. Ltd.

- Google Asia Pacific Pte. Ltd.

- Microsoft Operations Pte. Ltd. (Microsoft Singapore)

- Equinix Singapore Pte. Ltd.

- Alibaba Cloud (Singapore) Private Limited

- Palo Alto Networks (Singapore) Pte. Ltd.

- Check Point Software Technologies (Singapore) Pte. Ltd.

- Trend Micro (Singapore) Pte. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Smart-Nation Expenditure Surge

- 4.2.2 Rapid 5G Roll-out and Adoption

- 4.2.3 Enterprise Cloud-first Mandates

- 4.2.4 Digital Bank Licences Boost BFSI Tech Spend

- 4.2.5 National AI Compute Resource (NACR) Roll-out

- 4.2.6 Green-Powered Hyperscale Data-centre Incentives

- 4.3 Market Restraints

- 4.3.1 Scarcity of Skilled Digital Talent

- 4.3.2 Escalating Cyber-attack Surface

- 4.3.3 Power-grid Capacity Caps on New DC Builds

- 4.3.4 Wage Inflation from Foreign-Labour Curbs

- 4.4 Value Chain Analysis

- 4.5 Evaluation of Critical Regulatory Framework

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macro-economic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 IT Hardware

- 5.1.1.1 Computer Hardware

- 5.1.1.2 Networking Equipment

- 5.1.1.3 Peripherals

- 5.1.2 IT Software

- 5.1.3 IT Services

- 5.1.3.1 Managed Services

- 5.1.3.2 Business Process Services

- 5.1.3.3 Business Consulting Services

- 5.1.3.4 Cloud Services

- 5.1.4 IT Infrastructure

- 5.1.5 Communication Services

- 5.1.1 IT Hardware

- 5.2 By End-User Enterprise Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Deployment Model

- 5.3.1 On-premise

- 5.3.2 Cloud

- 5.3.3 Hybrid

- 5.4 By End-user Industry Vertical

- 5.4.1 Government and Public Administration

- 5.4.2 BFSI

- 5.4.3 Energy and Utilities

- 5.4.4 Retail, E-commerce and Logistics

- 5.4.5 Manufacturing and Industry 4.0

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Oil and Gas (Up-, Mid-, Down-stream)

- 5.4.8 Gaming and Esports

- 5.4.9 Other Verticals

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services (AWS) Singapore

- 6.4.2 International Business Machines Corporation (IBM Singapore Pte. Ltd.)

- 6.4.3 Cognizant Technology Solutions Asia Pacific Pte. Ltd.

- 6.4.4 Micron Semiconductor Asia Operations Pte. Ltd.

- 6.4.5 SAP Asia Pte. Ltd.

- 6.4.6 Wipro Ltd. (Singapore)

- 6.4.7 Hewlett Packard Enterprise Singapore Pte. Ltd.

- 6.4.8 Intel Technology Asia Pte. Ltd.

- 6.4.9 Singapore Telecommunications Ltd. (Singtel)

- 6.4.10 StarHub Ltd.

- 6.4.11 M1 Ltd.

- 6.4.12 TPG Telecom Pte. Ltd. (SIMBA Telecom)

- 6.4.13 NCS Pte. Ltd.

- 6.4.14 NEC Asia Pacific Pte. Ltd.

- 6.4.15 Dell Technologies Singapore Pte. Ltd.

- 6.4.16 Google Asia Pacific Pte. Ltd.

- 6.4.17 Microsoft Operations Pte. Ltd. (Microsoft Singapore)

- 6.4.18 Equinix Singapore Pte. Ltd.

- 6.4.19 Alibaba Cloud (Singapore) Private Limited

- 6.4.20 Palo Alto Networks (Singapore) Pte. Ltd.

- 6.4.21 Check Point Software Technologies (Singapore) Pte. Ltd.

- 6.4.22 Trend Micro (Singapore) Pte. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment

日本资讯通信技术市场:按支出、技术和地区划分,2026-2034年

日本资讯通信技术市场:按支出、技术和地区划分,2026-2034年 2026年针对政策制定者的全球数位主权市场报告

2026年针对政策制定者的全球数位主权市场报告 泰国资讯通信技术:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南资讯通信技术:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

泰国资讯通信技术:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南资讯通信技术:市场占有率分析、产业趋势与统计、成长预测(2026-2031年) 全球资讯与通讯技术(ICT)市场规模、份额、趋势及成长分析报告(2026-2034)义大利资讯通信技术市场:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)印度资讯通信技术:市场份额分析、产业趋势与统计、成长预测(2026-2031)菲律宾资讯通信技术市场:市场份额分析、行业趋势与统计、成长预测(2026-2031年)零售业先进资讯与通讯解决方案的成长机会2025-2026年资讯通讯科技(ICT)产业客户经验(CX)成长机会

全球资讯与通讯技术(ICT)市场规模、份额、趋势及成长分析报告(2026-2034)义大利资讯通信技术市场:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)印度资讯通信技术:市场份额分析、产业趋势与统计、成长预测(2026-2031)菲律宾资讯通信技术市场:市场份额分析、行业趋势与统计、成长预测(2026-2031年)零售业先进资讯与通讯解决方案的成长机会2025-2026年资讯通讯科技(ICT)产业客户经验(CX)成长机会