|

市场调查报告书

商品编码

1934835

越南资讯通信技术:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)Vietnam ICT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

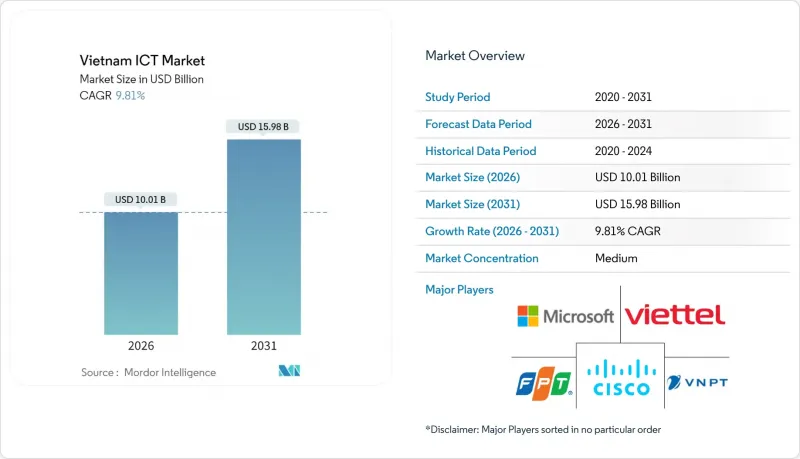

越南资讯通信技术市场规模在 2025 年达到 91.2 亿美元,预计到 2031 年将达到 159.8 亿美元,高于 2026 年的 100.1 亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 9.81%。

政府主导的数位化专案、大规模外商直接投资以及半导体生产在地化的推进,持续加速硬体、软体和服务领域的数位转型。大规模的5G部署,以及不断扩大的云端和资料中心容量,正在为通讯业者和全球超大规模资料中心业者创造新的收入来源。同时,越南48个市级政府的智慧城市建设项目,推动了对整合连接、分析和网路安全解决方案的需求。国营通讯业者与跨国技术供应商之间的竞争格局较为平衡,后者正不断深化与本地企业的伙伴关係,以满足特定产业的数位转型需求。儘管面临资金限制和省会城市高技能工程人才短缺等不利因素,但随着企业实现营运现代化并拓展新的数位化服务模式,越南资讯通信技术市场预计到2030年仍将保持两位数的成长。

越南资讯通信技术市场趋势与洞察

智慧城市基础建设发展计划

政府核准了48个市政数位化蓝图,由此催生了价值20亿美元的互联互通、感测器网路和网路安全平台专案储备。胡志明市防洪系统的升级和岘港市的永续城市规划都需要即时数据分析,推动了对边缘运算和物联网闸道的需求。公共部门至少10%的IT预算必须用于网路安全,这进一步扩大了威胁侦测供应商的潜在市场。国家数位身分识别系统「VNeID」的推出已惠及数百万公民,并正在扩展电子政府入口网站的身份验证服务。这些计划为通讯业者、云端服务供应商和系统整合商创造了协同效应,同时也将越南打造成为区域智慧城市解决方案的试验场。

工业4.0价值链中的数位转型

实施人工智慧驱动的预测维修系统的製造工厂报告称,生产效率提高了30%至50%。纺织品出口商Vinatex在实施物联网赋能的供应链分析后,连合收益成长了6.1%。三星9.2亿美元的扩张计画证实了越来越多的资金流入基于机器学习的品管和自动化物流领域。第109号法令降低了本地生产车辆的註册税,透过机器人技术和连网工厂平台加速了汽车产业的数位化。基于区块链的溯源追踪和人工智慧增强的需求预测正在帮助越南製造商赢得高利润的全球订单,同时缩短产品上市时间。

建设网路和资料中心的初始投资成本很高

5G频谱、光纤回程传输和三级资料中心建设的高资本密集度给营运商的财务状况带来了压力,尤其是在两个大都会圈以外的地区。农村地区的需求密度往往低于利用标准,导致投资者的投资回收期延长。汇率波动风险和利率上升推高了资金筹措成本,而土地使用审批也面临行政延误。儘管公私合营模式兴起,但小规模本地通讯业者和中立铁塔公司仍面临资金筹措缺口。这些限制因素可能会延缓农村宽频部署进程,并限制边缘运算的覆盖范围,而边缘运算是许多工业4.0应用场景所必需的。

细分市场分析

到2025年,IT硬体将维持越南ICT市场22.88%的份额,这主要得益于通讯业者升级基地台和资料中心设施以支援全国5G骨干网路建设。然而,随着基础建设的日益成熟,越南ICT市场硬体部分的成长速度预计将低于服务部分。同时,在咨询、系统整合和託管安全计划等需要专业知识的推动下,IT服务预计到2031年将以12.07%的复合年增长率成长。混合云端、ERP现代化和人工智慧实施需要持续的专业服务支持,这将为供应商和整合商创造稳定的收入来源。

企业对计量收费可扩展性的追求正在加速云端服务的普及,从而推动对营运商提供的连接服务和网路安全解决方案的需求。随着企业从永久授权转向基于订阅的SaaS模式,软体收入也在成长,降低了前期成本。电信服务受惠于行动数据消费的成长和企业5G应用场景的扩展。託管服务协议,尤其是网路安全监控服务,使中小企业能够外包复杂功能,并以最少的人力满足监管要求。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 智慧城市基础建设发展计划

- 工业4.0价值链中的数位转型

- 云端运算和人工智慧领域的资本支出激增

- 政府的「越南製造」数位经济蓝图

- 提高半导体自给自足能力的奖励

- 建构超大规模和区域性IDC中心

- 市场限制

- 网路和资料中心建设初期成本高昂

- 专业资讯通信技术人员短缺

- 对进口核心零件的高度依赖

- 分散网路安全合规的负担

- 价值/供应链分析

- 监管环境

- 技术展望

- 重大技术投资

- 云端运算

- 人工智慧

- 网路安全

- 数位服务

- 边缘运算和物联网

- 重大技术投资

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 生态系分析

- 产业相关人员分析

- 新冠疫情及宏观环境变化的影响及復苏

第五章 市场规模与成长预测

- 按类型

- IT硬体

- 电脑硬体

- 网路装置

- 周边设备

- IT软体

- IT服务

- 託管服务

- 业务流程服务

- 商业咨询服务

- 云端服务

- IT基础设施

- 通讯服务

- IT硬体

- 按最终用户公司规模划分

- 小型企业

- 大公司

- 按最终用户行业划分

- 政府和公共机构

- BFSI

- 能源与公共产业

- 零售、电子商务与物流

- 製造业和工业4.0

- 医疗保健和生命科学

- 石油和天然气(上游、中游、下游)

- 游戏和电子竞技

- 其他行业

- 按行业

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Microsoft Corporation

- Cisco Systems Inc.

- Viettel Group

- VNPT Group

- FPT Corporation

- CMC Corporation

- Qualcomm Technologies Inc.

- Google LLC(Alphabet Inc.)

- Fujitsu Ltd.

- Fortinet Inc.

- Vietnamobile

- D-Link Systems Inc.

- Hewlett Packard Enterprise

- Telehouse Vietnam

- Oracle Corporation

- IBM Corporation

- Samsung Electronics Vietnam

- VNG Corporation

- MobiFone

- TMA Solutions

- KMS Technology

- NashTech

- Axon Active Vietnam

- Ciena Corporation

- Ericsson Vietnam

第七章 市场机会与未来展望

The Vietnam ICT market was valued at USD 9.12 billion in 2025 and estimated to grow from USD 10.01 billion in 2026 to reach USD 15.98 billion by 2031, at a CAGR of 9.81% during the forecast period (2026-2031).

Government-led digitalization programs, sizable foreign direct investment, and the push to localize semiconductor production continue to accelerate adoption across hardware, software, and services. Large-scale 5G rollouts, paired with expanding cloud and data-center capacity, are fueling new revenue streams for telecommunications operators and global hyperscalers. At the same time, smart-city initiatives in 48 municipalities are driving demand for integrated connectivity, analytics, and cybersecurity solutions. The competitive dynamic remains balanced between state-owned carriers and multinational technology vendors that are deepening local partnerships to address industry-specific digital-transformation mandates. Although funding constraints in secondary cities and a shortage of advanced engineering talent pose headwinds, the Vietnam ICT market is expected to maintain double-digit momentum through 2030 as enterprises modernize operations and new digital-services models scale.

Vietnam ICT Market Trends and Insights

Smart-City Infrastructure Programs

Government approval of 48 municipal digitalization roadmaps has created a USD 2 billion pipeline for connectivity, sensor networks, and cybersecurity platforms. Ho Chi Minh City's flood-management upgrade and Da Nang's sustainable-city plan both require real-time data analytics, strengthening demand for edge computing and IoT gateways. Mandatory allocation of at least 10% of public-sector IT budgets to cybersecurity further expands the addressable market for threat-detection vendors. The national VNeID digital-identity roll-out already serves millions of citizens and is scaling authentication services for e-government portals. These projects generate multiplier effects for telecom carriers, cloud providers, and systems integrators while positioning Vietnam as a testbed for regional smart-city solutions.

Digital Transformation Across Industry 4.0 Value Chains

Manufacturing plants adopting AI-driven predictive-maintenance systems report production-efficiency gains of 30-50%. Textile exporters such as Vinatex have boosted consolidated revenue by 6.1% after deploying IoT-enabled supply-chain analytics. Samsung's USD 920 million expansion underscores rising capital inflows devoted to machine-learning-based quality control and automated logistics. Decree 109, which lowered registration taxes for locally produced vehicles, has accelerated automotive digitalization through robotics and connected-factory platforms. Blockchain-powered provenance tracking and AI-enhanced demand forecasting are helping Vietnamese manufacturers capture higher-margin global orders while shortening time-to-market.

High Up-Front Network and Data-Center Build Costs

The capital intensity of 5G spectrum, fiber backhaul, and Tier III data-center construction strains operator balance sheets, especially outside the two largest metros. Secondary cities often lack the demand density to hit utilization thresholds, extending payback periods for investors. Currency fluctuation risk and rising interest rates elevate funding costs, while land-use approvals add administrative delays. Although public-private-partnership models are emerging, financing gaps persist for small regional carriers and neutral-host tower companies. These constraints could defer rural broadband timelines and limit edge-computing coverage that many Industry 4.0 use cases require.

Other drivers and restraints analyzed in the detailed report include:

- Surging Cloud- and AI-Linked Capex

- "Make-in-Vietnam" Digital-Economy Roadmap

- Shortage of Specialized ICT Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IT Hardware maintained a 22.88% share of the Vietnam ICT market in 2025 as operators upgraded base-station and data-center equipment to support nationwide 5G backbones. However, the Vietnam ICT market size for hardware is expected to expand more slowly than that for services as infrastructure build-outs mature. In contrast, IT Services is on track for a 12.07% CAGR through 2031, propelled by consulting, systems integration, and managed-security projects that require specialized know-how. Hybrid cloud, ERP modernization, and AI implementation demand continuous professional-services support, creating sticky revenue streams for vendors and integrators.

Cloud-services adoption is escalating as enterprises pursue pay-as-you-go scalability; this, in turn, lifts demand for connectivity and cybersecurity offerings bundled by telecom carriers. Software revenue is also climbing as firms migrate from perpetual licenses to subscription-based SaaS, lowering up-front costs. Communication services benefit from growing mobile-data consumption and enterprise 5G use cases. Managed-services contracts, especially for cybersecurity monitoring, allow SMEs to outsource complex functions and keep headcount lean while meeting regulatory mandates.

The Vietnam ICT Market Report is Segmented by Type (IT Hardware, IT Software, IT Services, IT Infrastructure, Communication Services), End-User Enterprise Size (Small and Medium Enterprises, Large Enterprises), End-User Industry Vertical (Government and Public Administration, BFSI, Energy and Utilities, Retail, E-Commerce and Logistics, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Microsoft Corporation

- Cisco Systems Inc.

- Viettel Group

- VNPT Group

- FPT Corporation

- CMC Corporation

- Qualcomm Technologies Inc.

- Google LLC (Alphabet Inc.)

- Fujitsu Ltd.

- Fortinet Inc.

- Vietnamobile

- D-Link Systems Inc.

- Hewlett Packard Enterprise

- Telehouse Vietnam

- Oracle Corporation

- IBM Corporation

- Samsung Electronics Vietnam

- VNG Corporation

- MobiFone

- TMA Solutions

- KMS Technology

- NashTech

- Axon Active Vietnam

- Ciena Corporation

- Ericsson Vietnam

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smart-city infrastructure programmes

- 4.2.2 Digital transformation across Industry 4.0 value-chains

- 4.2.3 Surging cloud- and AI-linked capex

- 4.2.4 Government "Make-in-Vietnam" digital-economy roadmap

- 4.2.5 Semiconductor self-sufficiency incentives

- 4.2.6 Hyperscale and regional IDC hub build-out

- 4.3 Market Restraints

- 4.3.1 High up-front network and data-centre build costs

- 4.3.2 Shortage of specialised ICT talent

- 4.3.3 Heavy reliance on imported core components

- 4.3.4 Fragmented cyber-regulatory compliance burden

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 Key Technology Investments

- 4.6.1.1 Cloud Technology

- 4.6.1.2 Artificial Intelligence

- 4.6.1.3 Cyber-security

- 4.6.1.4 Digital Services

- 4.6.1.5 Edge Computing and IoT

- 4.6.1 Key Technology Investments

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Ecosystem Analysis

- 4.9 Industry Stakeholder Analysis

- 4.10 Impact and Recovery from COVID-19 and Macro Shifts

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 IT Hardware

- 5.1.1.1 Computer Hardware

- 5.1.1.2 Networking Equipment

- 5.1.1.3 Peripherals

- 5.1.2 IT Software

- 5.1.3 IT Services

- 5.1.3.1 Managed Services

- 5.1.3.2 Business Process Services

- 5.1.3.3 Business Consulting Services

- 5.1.3.4 Cloud Services

- 5.1.4 IT Infrastructure

- 5.1.5 Communication Services

- 5.1.1 IT Hardware

- 5.2 By End-User Enterprise Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By End-user Industry Vertical

- 5.3.1 Government and Public Administration

- 5.3.2 BFSI

- 5.3.3 Energy and Utilities

- 5.3.4 Retail, E-commerce and Logistics

- 5.3.5 Manufacturing and Industry 4.0

- 5.3.6 Healthcare and Life Sciences

- 5.3.7 Oil and Gas (Up-, Mid-, Down-stream)

- 5.3.8 Gaming and Esports

- 5.3.9 Other Verticals

- 5.3.10 By Industry Vertical (Value)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Cisco Systems Inc.

- 6.4.3 Viettel Group

- 6.4.4 VNPT Group

- 6.4.5 FPT Corporation

- 6.4.6 CMC Corporation

- 6.4.7 Qualcomm Technologies Inc.

- 6.4.8 Google LLC (Alphabet Inc.)

- 6.4.9 Fujitsu Ltd.

- 6.4.10 Fortinet Inc.

- 6.4.11 Vietnamobile

- 6.4.12 D-Link Systems Inc.

- 6.4.13 Hewlett Packard Enterprise

- 6.4.14 Telehouse Vietnam

- 6.4.15 Oracle Corporation

- 6.4.16 IBM Corporation

- 6.4.17 Samsung Electronics Vietnam

- 6.4.18 VNG Corporation

- 6.4.19 MobiFone

- 6.4.20 TMA Solutions

- 6.4.21 KMS Technology

- 6.4.22 NashTech

- 6.4.23 Axon Active Vietnam

- 6.4.24 Ciena Corporation

- 6.4.25 Ericsson Vietnam

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

日本资讯通信技术市场:按支出、技术和地区划分,2026-2034年

日本资讯通信技术市场:按支出、技术和地区划分,2026-2034年 2026年针对政策制定者的全球数位主权市场报告

2026年针对政策制定者的全球数位主权市场报告 新加坡资讯通信技术:市场份额分析、产业趋势与统计、成长预测(2026-2031)泰国资讯通信技术:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

新加坡资讯通信技术:市场份额分析、产业趋势与统计、成长预测(2026-2031)泰国资讯通信技术:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球资讯与通讯技术(ICT)市场规模、份额、趋势及成长分析报告(2026-2034)义大利资讯通信技术市场:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)印度资讯通信技术:市场份额分析、产业趋势与统计、成长预测(2026-2031)菲律宾资讯通信技术市场:市场份额分析、行业趋势与统计、成长预测(2026-2031年)零售业先进资讯与通讯解决方案的成长机会2025-2026年资讯通讯科技(ICT)产业客户经验(CX)成长机会

全球资讯与通讯技术(ICT)市场规模、份额、趋势及成长分析报告(2026-2034)义大利资讯通信技术市场:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)印度资讯通信技术:市场份额分析、产业趋势与统计、成长预测(2026-2031)菲律宾资讯通信技术市场:市场份额分析、行业趋势与统计、成长预测(2026-2031年)零售业先进资讯与通讯解决方案的成长机会2025-2026年资讯通讯科技(ICT)产业客户经验(CX)成长机会