|

市场调查报告书

商品编码

1934847

西班牙电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)Spain Telecom MNO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

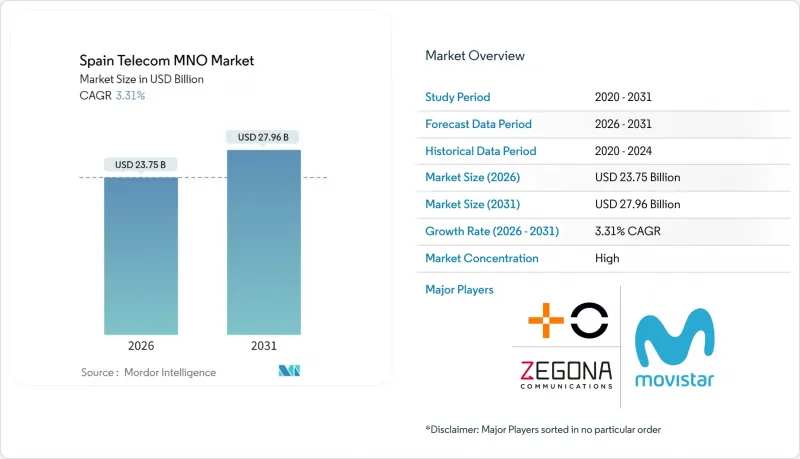

预计到 2026 年,西班牙电信行动网路营运商 (MNO) 市场的规模将达到 237.5 亿美元。

这代表着从 2025 年的 229.9 亿美元成长到 2031 年的 279.6 亿美元,2026 年至 2031 年的复合年增长率为 3.31%。

这种温和的成长反映了成熟的市场环境,营运商们正专注于以数据为中心的收入模式、高效的网路共用以及严谨的资本配置。光纤到府 (FTTH) 的普及率不断提高,目前已覆盖 95.2% 的家庭,这支撑了优质整合配套服务带来的平均每用户收入 (ARPU),即便麵临价格竞争。产业整合改变了竞争格局。由 Orange 和 MasMóvil 联盟成立的 MasOrange 已占据 42% 的用户份额,缩小了与 Telefónica 25% 的差距。新的合作模式正在涌现,例如与 Vodafone 合作的价值 900-100 亿欧元的 FiberCo 项目。能源成本的波动(占营运支出的 10-15%)以及悬而未决的频谱诉讼限制了利润率的提升。同时,一项由政府支持的 10 亿欧元独立农村 5G 基金确保了 96% 人口的 5G 网路覆盖,巩固了西班牙在先进行动技术领域的领先地位。

西班牙电信行动网路营运商市场趋势与分析

5G覆盖范围扩大和频率重组

西班牙在独立组网(SA)5G领域领先欧洲,预计到2025年将实现96%的人口覆盖率,这得益于政府为农村基地台提供的10亿欧元公共资金。 Movistar、MasOrange和沃达丰联合使用700MHz频谱将加速农村地区的部署,同时降低部署成本。 MasOrange和爱立信的开放式无线接取网路(Open RAN)专案将为具有弹性容量扩充能力的软体定义网路铺平道路。根据欧盟委员会5G观察站的数据,到2024年3月,西班牙的家庭覆盖率将达到92.3%,远高于欧盟平均水准。这些成就使通讯业者能够将资源重新分配,用于实现5G-SA在企业服务和低延迟应用方面的商业化。

行动数据需求不断增长,无限流量套餐也日益普及

以购买力平价计算,其无限流量套餐价格为17.39美元,是欧洲最便宜的套餐之一,因此在大都会圈使用率很高。 2024年初,流量成长放缓至年增12%,但通讯业者正透过分阶段推出每GB价格合理的5G提案来保障用户价值。随着价格优势日益凸显,传统业者的市占率被注重价格的新兴企业蚕食,低价品牌之间的竞争也愈演愈烈。营运商的策略性应对措施着重于透过增值套装、加值内容和忠诚度计画来提升服务质量,而不是依赖大幅折扣。

用户群已饱和

截至2025年3月,活跃SIM卡数量将达到6,162万张,相当于每百人拥有125.6条线路,这意味着用户自然成长空间有限。行动号码可携性案例较去年同期成长7.6%,凸显市场占有率竞争激烈,而非净成长。固定宽频也接近普及,促使营运商加快开发数位服务等新的收入来源。人口老化加剧了成长停滞,老年人使用数据密集型服务的可能性较低。因此,西班牙电信行动网路营运商(MNO)市场正将资金转向企业服务、物联网和边缘云端提案,以避免消费市场饱和。

细分市场分析

截至2025年,资料通讯和网路业务将占西班牙电信行动网路营运商(MNO)市场份额的50.39%,这反映了前所未有的光纤普及率和极具竞争力的无限流量移动套餐。语音服务仍主要透过融合套餐保持稳定,但简讯收入持续下降。物联网(IoT)和机器对机器(M2M)连接虽然用户基数较小,但预计将以3.40%的复合年增长率(CAGR)成为成长最快的领域,这主要得益于物流、能源和智慧城市解决方案的推动。随着卫星网路终端(NTN)消除遍远地区的覆盖障碍,西班牙面向物联网连接的电信行动网路营运商市场规模预计将稳步扩大。 OTT和付费电视服务将受益于光纤到府(FTTH)的广泛应用,使营运商能够将占用频宽的优质影片和云端游戏服务整合到现有数据套餐中。

营运商将利用西班牙电信行动网路营运商 (MNO) 市场规模中,尽力而为的 4G 网路和麵向企业用户的有保障的 5G-SA 网路之间的差异来获利。网路 API 将使开发人员能够将按需品质功能整合到他们的应用程式中,从而产生增量收入。随着云端游戏等对延迟敏感的服务日趋成熟,营运商预计高端用户群将实现两位数成长,从而抵消传统语音服务的商品化趋势。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 监理与政策框架

- 频谱环境和竞争性拥有情形

- 通讯业生态系统

- 宏观经济与外在因素

- 波特五力分析

- 竞争对手之间的竞争

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 领先行动网路营运商的关键绩效指标(2020-2025)

- 独立行动用户和渗透率

- 行动网路使用者数量和普及率

- 按接入技术分類的SIM卡连线数和渗透率

- 蜂巢式物联网/M2M连接

- 宽频连线(移动和固定)

- ARPU(每位用户平均收入)

- 每用户平均数据使用量(GB/月)

- 市场驱动因素

- 5G覆盖范围扩大和频率重组

- 行动数据和包月套餐的需求不断增长

- 光纤到府的蓬勃发展将促成融合套餐的出现

- 物联网在企业中的应用(智慧电网、物流)

- 由于有利于行动虚拟网路营运商(MVNO)的批发规则,租赁收入增加。

- 欧盟復苏基金支持农村地区5G和中立主机

- 市场限制

- 用户群已饱和

- 价格竞争和低价品牌对每位用户平均收入(ARPU)带来压力。

- 频谱使用诉讼的不确定性

- 能源成本波动推高了营运成本。

- 技术展望

- 电信业主要经营模式分析

- 定价模式和定价分析

第五章 市场规模与成长预测

- 通信总收入和每位用户平均收入

- 服务类型

- 语音服务

- 数据和网际网路服务

- 通讯服务

- 物联网和机器对机器服务

- OTT和付费电视服务

- 其他服务(附加价值服务、漫游和国际服务、企业和批发服务等)

- 最终用户

- 公司

- 一般消费者

第六章 竞争情势

- 市场集中度

- 主要供应商的策略与投资动向(2023-2025)

- 2024年行动网路营运商市场占有率分析

- Product Benchmarking Analysis for mobile network services

- MNO snapshot(subscribers, churn rate, ARPU, etc.)

- 行动网路营运商公司简介*

- Telefonica Spain(Movistar)

- MASORANGE, SL

- Zegona Communications(Vodafone Spain)

第七章 市场机会与未来展望

Spain Telecom MNO Market size in 2026 is estimated at USD 23.75 billion, growing from 2025 value of USD 22.99 billion with 2031 projections showing USD 27.96 billion, growing at 3.31% CAGR over 2026-2031.

Moderate growth reflects a mature environment where operators focus on data-centric revenues, network-sharing efficiency, and disciplined capital allocation. Intensifying fiber-to-the-home penetration, which now covers 95.2% of premises, sustains premium converged bundles that lift average revenue per user despite price competition. Consolidation has reshaped rivalry after the Orange-MasMovil tie-up created MasOrange with 42% subscriber share, narrowing the gap with Telefonica's 25% stake while prompting new partnering models such as the EUR 9-10 billion FibreCo with Vodafone. Energy-cost volatility, which absorbs 10-15% of operating expenses, and unresolved spectrum-fee litigation temper margin expansion. Meanwhile, government-backed EUR 1 billion funding for rural standalone 5G ensures 96% population coverage, reinforcing Spain's leadership in advanced mobile technology.

Spain Telecom MNO Market Trends and Insights

5G Coverage Expansion and Spectrum Refarming

Spain leads Europe in standalone 5G, achieving 96% population coverage by 2025 on the strength of EUR 1 billion public funding for rural base-stations. Joint use of the 700 MHz band by Movistar, MasOrange, and Vodafone reduces deployment cost while speeding suburban roll-outs. MasOrange's Open RAN program with Ericsson ushers in software-defined networks capable of elastic capacity scaling. The European Commission's 5G Observatory confirms Spain's 92.3% household coverage by March 2024, well ahead of the EU mean . These achievements allow operators to pivot resources toward 5G-SA monetization in enterprise and low-latency applications.

Rising Mobile-Data Demand and Unlimited Plans

Unlimited bundles priced at USD 17.39 purchasing-power-parity rank among Europe's cheapest, stimulating heavy usage in metropolitan corridors. Although traffic growth slowed to 12% year-over-year in early-2024, operators defend value through tiered 5G propositions with superior cost-per-GB economics. Competitive migration toward low-cost brands intensified, with incumbents losing share to price-focused challengers. The strategic response centers on value-added bundles, premium content, and loyalty programs that elevate perceived service quality without relying solely on heavy discounts.

Saturated Subscriber Base

Active SIMs reached 61.62 million by March 2025, equating to 125.6 lines per 100 residents and signaling limited room for organic user growth. Portability volumes climbed 7.6% year-over-year, underlining a zero-sum battle for share rather than net additions. Fixed broadband likewise nears total household penetration, intensifying operators' hunt for incremental revenue in digital services. Demographic aging compounds stagnation because older cohorts adopt fewer data-intensive offerings. Consequently, the Spain telecom MNO market shifts capital toward enterprise, IoT, and edge-cloud propositions that sidestep consumer saturation.

Other drivers and restraints analyzed in the detailed report include:

- FTTH Boom Enabling Converged Bundles

- Enterprise IoT Uptake in Smart Grids and Logistics

- ARPU Pressure from Price Wars and Low-Cost Brands

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Data and internet generated 50.39% of Spain telecom MNO market share in 2025, reflecting unmatched fiber penetration and aggressive unlimited mobile bundles. Voice remains sticky via converged offers, whereas SMS revenue declines continue. IoT and M2M lines constitute a smaller base but post the fastest 3.40% CAGR, propelled by logistics, energy, and smart-city solutions. The Spain telecom MNO market size for IoT-centric connectivity is projected to expand steadily as satellite NTNs remove rural coverage barriers. OTT and PayTV services leverage ubiquitous FTTH, enabling operators to embed premium video and cloud gaming that absorb bandwidth within existing allowances.

Operators monetize the Spain telecom MNO market size differential between best-effort 4G and guaranteed 5G-SA slices for corporate users. Network APIs open incremental revenue as developers integrate quality-on-demand features into applications. As latency-sensitive services such as cloud gaming mature, operators expect double-digit growth in premium tiers that counterbalance the commoditization of legacy voice.

The Spain Telecom MNO Market is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, Iot and M2M Services, OTT and PayTV Services, and Other Services), and End User (Enterprises, Consumer). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Telefonica Spain (Movistar)

- MASORANGE, S.L.

- Zegona Communications (Vodafone Spain)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Regulatory and Policy Framework

- 4.3 Spectrum Landscape and Competitive Holdings

- 4.4 Telecom Industry Ecosystem

- 4.5 Macroeconomic and External Drivers

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Bargaining Power of Buyers

- 4.6.5 Threat of Substitutes

- 4.7 Key MNO KPIs (2020-2025)

- 4.7.1 Unique Mobile Subscribers and Penetration Rate

- 4.7.2 Mobile Internet Users and Penetration Rate

- 4.7.3 SIM Connections by Access Technology and Penetration

- 4.7.4 Cellular IoT / M2M Connections

- 4.7.5 Broadband Connections (Mobile and Fixed)

- 4.7.6 ARPU (Average Revenue Per User)

- 4.7.7 Average Data Usage per Subscription (GB/month)

- 4.8 Market Drivers

- 4.8.1 5G coverage expansion and spectrum refarming

- 4.8.2 Rising mobile-data demand and unlimited plans

- 4.8.3 FTTH boom enabling converged bundles

- 4.8.4 Enterprise IoT uptake (smart grids, logistics)

- 4.8.5 MVNO-friendly wholesale rules boosting lease revenue

- 4.8.6 EU RRF funds for rural 5G and neutral hosts

- 4.9 Market Restraints

- 4.9.1 Saturated subscriber base

- 4.9.2 ARPU pressure from price wars and low-cost brands

- 4.9.3 Spectrum-fee litigation uncertainty

- 4.9.4 Energy-cost volatility inflating OPEX

- 4.10 Technological Outlook

- 4.11 Analysis of key business models in Telecom Sector

- 4.12 Analysis of Pricing Models and Pricing

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Overall Telecom Revenue and ARPU

- 5.2 Service Type

- 5.2.1 Voice Services

- 5.2.2 Data and Internet Services

- 5.2.3 Messaging Services

- 5.2.4 IoT and M2M Services

- 5.2.5 OTT and PayTV Services

- 5.2.6 Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.)

- 5.3 End-user

- 5.3.1 Enterprises

- 5.3.2 Consumer

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Investments by key vendors, 2023-2025

- 6.3 Market share analysis for MNOs, 2024

- 6.4 Product Benchmarking Analysis for mobile network services

- 6.5 MNO snapshot (subscribers, churn rate, ARPU, etc.)

- 6.6 Company Profiles* of MNOs (Includes Business Overview | Service Portfolio | Financials | Business Strategy and Recent Developments | SWOT Analysis)

- 6.6.1 Telefonica Spain (Movistar)

- 6.6.2 MASORANGE, S.L.

- 6.6.3 Zegona Communications (Vodafone Spain)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

行动虚拟网路营运商 (MVNO) 市场:2026-2032 年全球市场预测(按服务类型、费率方案、销售管道、最终用户产业和应用程式划分)5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测

行动虚拟网路营运商 (MVNO) 市场:2026-2032 年全球市场预测(按服务类型、费率方案、销售管道、最终用户产业和应用程式划分)5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测 2026年全球行动虚拟网路营运商(MVNO)市场报告

2026年全球行动虚拟网路营运商(MVNO)市场报告 行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年

行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年 行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分

行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分 东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)

东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)