|

市场调查报告书

商品编码

1940662

亚太地区低温运输物流:市占率分析、产业趋势与统计、成长预测(2026-2031年)Asia-Pacific Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

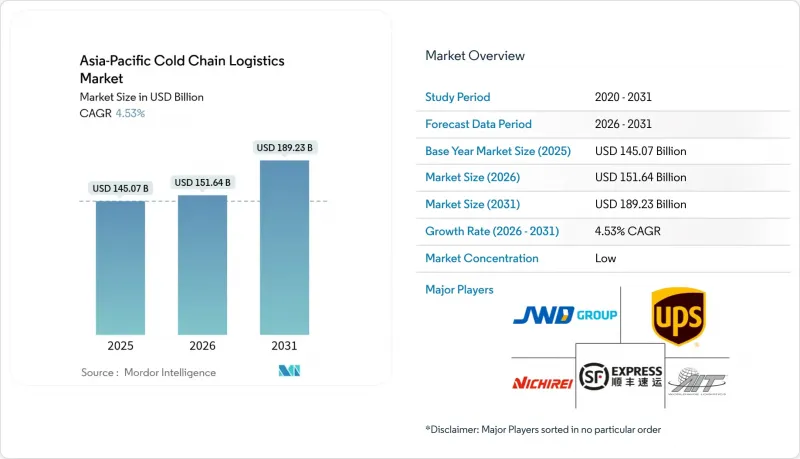

亚太地区低温运输物流市场预计将从 2025 年的 1,450.7 亿美元成长到 2026 年的 1,516.4 亿美元,预计到 2031 年将达到 1,892.3 亿美元,2026 年至 2031 年的复合年增长率为 4.53%。

在可支配收入成长、生鲜电商快速普及以及医药供应链日益成熟的推动下,需求持续稳定上升。同时,仓储建设整体上正从快速扩张转向技术主导的高效优化。儘管中国在规模上仍保持主导,但印度分散式仓库的快速发展标誌着向基于地理位置的网路模式的重大转变,从而实现当日送达。营运商正在采用人工智慧、机器人和自然冷冻系统来降低能耗和人工成本,将卓越营运转化为亚太低温运输物流市场新的成长动力。竞争格局仍保持适度分散,全球整合商正加速併购以确保技术实力。同时,区域性专业企业正利用其来之不易的本地资质和「第一公里」配送经验来巩固自身市场地位。

亚太地区低温运输物流市场趋势与洞察

加工食品和冷冻食品的消费量不断增加

亚洲中等收入家庭对速食、冷冻水产品和多日份蛋白质包的需求日益增长,为亚太低温运输物流市场创造了持续的核心需求。为此,超级市场超市正在调整库存单位(SKU),例如冷冻主菜和半成品麵团,这些产品需要从工厂到商店严格控制在-18°C的温度下。仓储设施业主正在高层仓库部署自动化穿梭系统,以分离冷藏、冷冻和超低温托盘,从而减少运输时间和能源损耗。智慧标籤记录时间-温度曲线,使零售商能够在展示商品前筛选出有风险的批次,从而减少废弃物并提高食品安全合规性。都市区家庭规模持续缩小,推动了独立包装产品的消费。这些产品在仓储网路中的配送週期更快,提高了托盘週转率,并带来了更高的每立方公尺收益。

电子商务食品宅配的成长

即时配送平台承诺15-30分钟送达,并正推动下一代微型仓配「暗店」的模组化冷却模式发展。节能型变速压缩机结合人工智慧驱动的空调系统,在严格控制温度±0.5°C的前提下,可降低30%的电力消耗。混合被动式和主动式凝胶包装盒确保冰淇淋即使在曼谷潮湿的午后也能经受住Scooter配送的考验。物联网监控器将资料传输至消费者应用程序,使温度透明度成为信任的象征。随着生鲜杂货应用程式向二线城市扩张,需求正从城市边缘的大型仓库转向嵌入人口密集郊区的辐射式配送中心,从而扩大亚太地区低温运输物流市场的规模。

冷冻设施的能源和房地产成本不断上涨

电力成本通常占营运成本的70%,在东京和悉尼,资料中心需求的不断增长给电网带来了巨大压力,导致电价上涨,挤压了仓库的利润空间。虽然太阳能板维修可以降低25%的电费,但由于需要大量的资本投资和漫长的批准流程,目前仅限于大规模屋顶和新建计划。同时,城市中心10公里范围内的地价飞涨,迫使开发商将开发地点转移到郊区。这意味着价格较低的土地需要更长的运输距离,从而增加燃料成本。节能隔热板和可变排气量压缩机可以部分抵消不断上涨的电费,但投资回收期超过五年,这使得小规模企业难以计算投资回报率。

细分市场分析

截至2025年,冷藏仓库占亚太地区低温运输物流市场的40.55%。现代化的高层冷藏仓库高度可达40米,穿梭机器人可在60秒内完成托盘运输,在保持仓库内精确温度控制的同时,将人事费用降低一半。营运商正在部署预测性维护软体,该软体可监测压缩机振动和冷媒压力,从而将非计划性运作减少15%。

附加价值服务虽然规模较小,但复合年增长率最高,达4.71%,这主要得益于品牌所有者将重新包装、速冻和产品调理等环节外包给单一第三方物流(3PL) 服务商。服务捆绑模式减少了交接环节,最大限度地降低了温度偏差和责任纠纷的风险。公共仓库根据货物停留时间和温度范围提供灵活的部位定价,这吸引了那些希望按不规则时间表发货的中小型食品出口商。同时,专用的私人设施也吸引了疫苗生产商,他们需要检验的布局和全天候的审核权限。从孤立的仓储模式转向承包解决方案的转变,标誌着亚太地区低温运输物流市场正朝着全面的供应链协调方向发展。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 加工食品和冷冻食品的消费量增加

- 电子商务生鲜配送的成长

- 扩大药品低温运输

- 协调SPS电子认证和无纸化清关一体化

- 零售商主导的专用冷藏仓库

- 透过多边基础设施走廊扩大冷冻能力

- 市场限制

- 冷冻设施的能源和房地产成本不断上涨

- 农村地区缺乏首公里基础设施

- 低全球暖化潜势冷媒工程师短缺

- 关于排放的ESG资讯揭露负担存在差异

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 排放标准对产业产生影响

- 新冠疫情与地缘政治事件对市场的影响

第五章 市场规模与成长预测

- 按服务类型

- 冷藏保管

- 公共仓库

- 私人仓储

- 冷藏运输

- 路

- 铁路

- 海

- 航空邮件

- 附加价值服务

- 冷藏保管

- 按温度类型

- 冷藏(0-5℃)

- 冷冻(-18 至 0°C)

- 环境的

- 超低温冷冻(低于-20°C)

- 透过使用

- 水果和蔬菜

- 肉类/家禽

- 鱼贝类

- 乳製品和冷冻甜点

- 麵包糖果甜点

- 调理食品

- 药品和生技药品

- 疫苗和临床试验用品

- 化学品/特殊材料

- 其他生鲜产品

- 按国家/地区

- 中国

- 日本

- 印度

- 韩国

- 印尼

- 泰国

- 澳洲

- 新加坡

- 马来西亚

- 亚太其他地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- United Parcel Service(UPS)

- JWD Group

- Nichirei Logistics Group Inc

- SF Express

- AIT Worldwide Logistics Inc

- CWT Pte Ltd

- Rokin Logistics

- Lineage Logistics

- Kerry Logistics Network Ltd

- Snowman Logistics Ltd

- ColdEX Logistics Pvt Ltd

- Linfox Pty Ltd

- Yusen Logistics Co Ltd(Part of NYK Line)

- Kuehne+Nagel

- DHL Group

- DSV

- Nippon Express

- Yamato Transport Co. Ltd

- CEVA Logistics

- Konoike Transport Co., Ltd

第七章 市场机会与未来展望

The Asia-Pacific Cold Chain Logistics Market is expected to grow from USD 145.07 billion in 2025 to USD 151.64 billion in 2026 and is forecast to reach USD 189.23 billion by 2031 at 4.53% CAGR over 2026-2031.

Rising disposable incomes, rapid e-grocery penetration, and pharmaceutical supply-chain upgrades keep demand on a steady upward course even as overall warehouse builds move from hyper-expansion to disciplined, technology-led optimization. China retains scale leadership, yet India's faster build-out of distributed depots signals a decisive pivot toward proximity-based networks designed for same-day fulfillment. Operators embed AI, robotics, and natural-refrigerant systems to compress energy intensity and labor exposure, turning operational excellence into the new growth lever for the Asia-Pacific cold chain logistics market. Competition remains moderately fragmented; global consolidators accelerate M&A to secure tech capabilities while regional specialists leverage hard-won local permits and first-mile know-how to guard niche positions.

Asia-Pacific Cold Chain Logistics Market Trends and Insights

Rising Consumption of Processed & Frozen Foods

Asia's middle-income households increasingly favor quick-prep meals, frozen seafood, and multi-day protein packs, creating a durable core of throughput for the Asia-Pacific cold chain logistics market. Supermarket chains respond by shifting stock-keeping units toward frozen entrees and par-baked dough that demand precise -18 °C handling from plant to shelf. Facility owners retrofit high-bay zones with automatic shuttle systems to segregate chilled, frozen, and deep-frozen pallets, trimming travel time and energy loss. Smart labels record time-temperature curves, letting retailers cull at-risk lots before display, which reduces write-offs and tightens food-safety compliance. Urban family sizes continue to shrink, spurring purchases of portioned packs that cycle through storage networks faster, raising pallet-turn velocity and amplifying revenue per cubic meter.

Growth in E-Commerce Grocery Delivery

Instant delivery platforms pledge 15- to 30-minute drop-offs, propelling a new generation of micro-fulfillment "dark" stores furnished with modular coolers. Energy-saving variable-speed compressors paired with AI-driven HVAC trim power draw by 30% while preserving tight +-0.5 °C bands. Hybrid passive-active gel-pack boxes allow ice-cream to survive scooter rides across humid Bangkok afternoons, and IoT monitors feed data to consumer apps, turning temperature transparency into a trust signal. As grocery apps expand into Tier-2 cities, demand shifts from mega-warehouses on city fringes to spoke depots embedded in densely populated suburbs, broadening the Asia-Pacific cold chain logistics market footprint.

High Energy & Real-Estate Cost of Cold Facilities

Electricity often represents 70% of opex, and data-center demand crowds grids across Tokyo and Sydney, driving tariff spikes that erode warehouse margins. Solar-panel retrofits cut bills 25% but entail high capex and lengthy permitting, restricting adoption to larger rooftops or greenfield projects. In parallel, land prices within 10 km of CBDs climb steeply, forcing developers outward where cheaper plots lengthen final-mile legs and elevate fuel spend. Energy-efficient insulation panels and variable-capacity compressors partially offset power hikes, but payback stretches past five years, complicating ROI math for smaller operators.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Pharmaceutical Cold Chain

- Harmonised SPS e-Certification & Paperless Customs Integration

- Rural First-Mile Infrastructure Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerated storage contributed 40.55% to the Asia-Pacific cold chain logistics market in 2025. Modern high-bay freezers now rise 40 meters, using shuttle robots to pull pallets in under 60 seconds, halving manual labor and maintaining chamber integrity. Operators invest in predictive maintenance software that monitors compressor vibration and coolant pressure, cutting unplanned downtime by 15%.

Value-added services, though smaller, capture the strongest 4.71% CAGR as brand owners outsource repackaging, blast-freezing, and product conditioning to a single 3PL. Service bundling reduces handoffs, thereby minimizing temperature excursions and liability disputes. Public warehouses embrace flexible slot-pricing based on dwell time and temperature band, appealing to SME food exporters eyeing sporadic shipments. Conversely, private dedicated sites attract vaccine manufacturers that demand validated layouts and 24/7 audit access. The shift from siloed warehousing to turnkey solutions underscores how the Asia-Pacific cold chain logistics market pivots toward holistic supply-chain orchestration.

The Asia-Pacific Cold Chain Logistics Market Report is Segmented by Service Type (Refrigerated Storage, Refrigerated Transportation, and Value-Added Services), Temperature Type (Chilled, Frozen, Ambient, and Deep-Frozen/Ultra-Low), Application (Fruits & Vegetables, Meat & Poultry, Fish & Seafood, and More), Country (China, Japan, India, South Korea, Indonesia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- United Parcel Service (UPS)

- JWD Group

- Nichirei Logistics Group Inc

- SF Express

- AIT Worldwide Logistics Inc

- CWT Pte Ltd

- Rokin Logistics

- Lineage Logistics

- Kerry Logistics Network Ltd

- Snowman Logistics Ltd

- ColdEX Logistics Pvt Ltd

- Linfox Pty Ltd

- Yusen Logistics Co Ltd (Part of NYK Line)

- Kuehne + Nagel

- DHL Group

- DSV

- Nippon Express

- Yamato Transport Co. Ltd

- CEVA Logistics

- Konoike Transport Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising consumption of processed & frozen foods

- 4.2.2 Growth in e-commerce grocery delivery

- 4.2.3 Expansion of pharmaceutical cold chain

- 4.2.4 Harmonised SPS e-Certification & Paperless Customs Integration

- 4.2.5 Retailer-led captive cold warehousing

- 4.2.6 Multilateral Infrastructure Corridors Expanding Refrigerated Capacity

- 4.3 Market Restraints

- 4.3.1 High energy & real-estate cost of cold facilities

- 4.3.2 Rural first-mile infrastructure gaps

- 4.3.3 Shortage of low-GWP refrigerant engineers

- 4.3.4 Divergent ESG disclosure burdens on emissions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Emission Standards on the Industry

- 4.9 Impact of COVID-19 and Geo-Political Events on the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Refrigerated Storage

- 5.1.1.1 Public Warehousing

- 5.1.1.2 Private Warehousing

- 5.1.2 Refrigerated Transportation

- 5.1.2.1 Road

- 5.1.2.2 Rail

- 5.1.2.3 Sea

- 5.1.2.4 Air

- 5.1.3 Value-Added Services

- 5.1.1 Refrigerated Storage

- 5.2 By Temperature Type

- 5.2.1 Chilled (0-5 °C)

- 5.2.2 Frozen (-18-0 °C)

- 5.2.3 Ambient

- 5.2.4 Deep-Frozen / Ultra-Low (less than-20 °C)

- 5.3 By Application

- 5.3.1 Fruits & Vegetables

- 5.3.2 Meat & Poultry

- 5.3.3 Fish & Seafood

- 5.3.4 Dairy & Frozen Desserts

- 5.3.5 Bakery & Confectionery

- 5.3.6 Ready-to-Eat Meals

- 5.3.7 Pharmaceuticals & Biologics

- 5.3.8 Vaccines & Clinical Trial Materials

- 5.3.9 Chemicals & Specialty Materials

- 5.3.10 Other Perishables

- 5.4 By Country

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 South Korea

- 5.4.5 Indonesia

- 5.4.6 Thailand

- 5.4.7 Australia

- 5.4.8 Singapore

- 5.4.9 Malaysia

- 5.4.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 United Parcel Service (UPS)

- 6.4.2 JWD Group

- 6.4.3 Nichirei Logistics Group Inc

- 6.4.4 SF Express

- 6.4.5 AIT Worldwide Logistics Inc

- 6.4.6 CWT Pte Ltd

- 6.4.7 Rokin Logistics

- 6.4.8 Lineage Logistics

- 6.4.9 Kerry Logistics Network Ltd

- 6.4.10 Snowman Logistics Ltd

- 6.4.11 ColdEX Logistics Pvt Ltd

- 6.4.12 Linfox Pty Ltd

- 6.4.13 Yusen Logistics Co Ltd (Part of NYK Line)

- 6.4.14 Kuehne + Nagel

- 6.4.15 DHL Group

- 6.4.16 DSV

- 6.4.17 Nippon Express

- 6.4.18 Yamato Transport Co. Ltd

- 6.4.19 CEVA Logistics

- 6.4.20 Konoike Transport Co., Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

低温运输物流市场:依服务类型、温度区域和最终用途划分-2026-2032年全球市场预测低温运输市场:2026-2032年全球市场预测(依温度范围、设备类型、服务模式、最终用户及通路划分)

低温运输物流市场:依服务类型、温度区域和最终用途划分-2026-2032年全球市场预测低温运输市场:2026-2032年全球市场预测(依温度范围、设备类型、服务模式、最终用户及通路划分) 2026年全球低温运输市场报告2026年全球冷冻食品物流市场报告2026年全球低温运输物流市场报告RAP冷藏货柜市场:依货柜类型、冷却系统类型、隔热材料、容量、温度范围、应用、最终用户划分,全球预测,2026-2032年

2026年全球低温运输市场报告2026年全球冷冻食品物流市场报告2026年全球低温运输物流市场报告RAP冷藏货柜市场:依货柜类型、冷却系统类型、隔热材料、容量、温度范围、应用、最终用户划分,全球预测,2026-2032年 2026-2030年全球低温运输市场

2026-2030年全球低温运输市场 低温运输市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、设备、解决方案、最终用户划分

低温运输市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、设备、解决方案、最终用户划分 西班牙低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

西班牙低温运输物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026-2034年全球低温运输物流市场规模、份额、趋势及成长分析报告

2026-2034年全球低温运输物流市场规模、份额、趋势及成长分析报告