|

市场调查报告书

商品编码

1940819

越南公路货运:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Vietnam Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

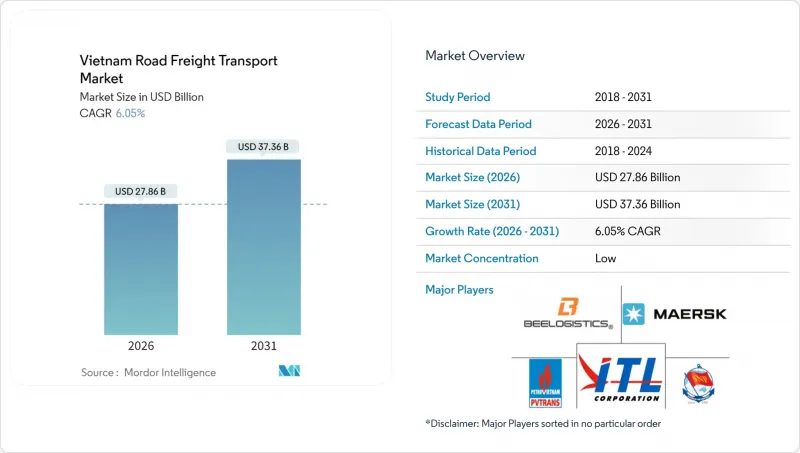

越南公路货运市场在 2025 年的价值为 262.7 亿美元,预计到 2031 年将达到 373.6 亿美元,高于 2026 年的 278.6 亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 6.05%。

这项扩张反映了持续的基础设施投资、不断扩大的产业丛集以及加速数位化应用共同作用,旨在提高货运效率,并将货物可视性树立为新的行业标准。基于国家5000公里目标的高速公路建设正在稳步推进,这将缩短南北运输时间,为出口商提供可预测的前置作业时间,并为製定具有竞争力的路线策略奠定基础。随着托运人对即时运价搜寻、即时追踪和动态路线优化等功能的需求日益增长,数位化货运平台正迅速发展。同时,在主要都会区试运行电动卡车标誌着向低排放运输的逐步转型。即使在DSV和DB Schenker于2025年4月合併之后,竞争格局依然分散,因为本地专家仍然掌握着详尽的路线信息,并与越南製造业保持着紧密的联繫。 「智慧门户」计划的跨境改革进一步巩固了越南作为连接中国和东协贸易路线门户的地位。

越南公路货运市场趋势及展望

到2030年,高速公路网将迅速扩张至5,000公里。

越南计划在2030年建成总长5,000公里的高速公路网,其中包括一条耗资250亿美元、全长1,811公里的南北高速公路。这条高速公路将使河内和胡志明市之间的通行时间缩短多达40%。专用货运车道将缓解目前90%的货车通行量所占国道的拥挤状况,使运输公司能够提高装载率并降低燃油成本。沿线製造商将能够更灵活地调整零件到货时间和生产计画,从而减少库存积压。通往边境口岸的新支线将促进与中国和寮国的贸易往来,使越南成为东协与中国之间货运的首选陆路桥樑。完善的实体网络,结合收费站的互通性和4G/5G网路覆盖,将支援即时车辆诊断和路线优化。

快速发展的电子商务和零售物流

预计到2025年,线上零售额将达到570亿美元,将推动物流公司转向枢纽辐射式营运模式和城市微型仓配中心。配送频率不断提高,而平均包裹尺寸却在缩小,这促使车队多元化发展,包括小型货车和用于生鲜食品订单的冷藏最后一公里配送车。越南电信邮政(ViettelPost)已扩展其跨境小包裹服务,并整合了API介面的追踪功能,以实现关键边境口岸的自动清关。投资人正大力投资仓储机器人技术和基于人工智慧的路线规划器,以减少配送失败率。区域扩张策略正在二、三线城市增设配送中心,扩大潜在需求,但营运商在维持成本效益方面面临挑战。

物流成本占GDP的比例持续居高不下。

到2024年,越南物流成本占GDP的比例将达到16.8%,远高于已开发经济体10-11%的水准。运输方式分散、回程传输匹配不佳以及繁琐的海关手续推高了交货成本,并限制了中小企业使用公路货运。尤其是在农村地区,遵守ISO 22000和HACCP标准增加了文书工作和低温运输设备的成本,而基础设施支援不足。出口商为了因应前置作业时间的不确定性而持有额外的缓衝库存,这增加了营运资金需求,并削弱了其在价格敏感型农产品领域的竞争力。

细分市场分析

到2025年,製造业将占越南货运量的35.12%,反映出越南公路货运市场正向该国的电子和机械组装丛集转型。受製造业主导的货运需求推动,越南公路货运市场规模预计将稳定成长,这得益于工厂使用率的提高和国内零件采购的深入。同时,受电子商务的驱动,批发和零售业预计将在2026年至2031年间以6.55%的复合年增长率增长,这将刺激高频补货需求,并推动运输网络扩展至郊区配送中心。该领域的趋势有利于那些能够提供SKU级别可视性和温控能力的生鲜食品运输业者。在公路和港口发展的支撑下,建筑材料货运量将保持稳定。此外,石油和天然气计划将需要运输专用管道和钻机零件,而目前很少有重型运输业者能够提供此类服务。随着水产品和水果出口的可追溯性法规日益严格,农产品运输商正在投资物联网托盘和隔热帘式拖车,以通过欧盟和日本的严格检查。

在越南公路货运市场,结合仓储设施和运输服务的公私合营正为製造商提供一站式物流解决方案。高价值电子产品货物依赖即时定位追踪和紧急通知技术,以降低窃盗率为代价,但也导致保全成本上升。多个货运交易平台应运而生,用于对接中部地区的回程传输货物,有助于减少空驶里程,并略微降低该行业的成本占GDP比重。同时,以往依赖海运进行东协内部货物运输的製造商,越来越多地采用道路运输,以缓解港口拥堵,更快地抵达区域枢纽,从而提升国内货运公司的运力。

越南南北区域特征和两个大都会圈支撑着消费需求,预计2025年,国内货运市场份额将维持在63.45%。然而,国际货运预计在2026年至2031年间将以7.10%的复合年增长率增长,这表明市场对避免多次港口转运的门到门道路运输解决方案的需求将会增加。友义海关的数位化计画旨在2030年实现高达50%的文书工作自动化,从而缩短清关时间,并鼓励越南托运人选择跨境卡车运输而非多式联运路线。目前,越南国际公路道路运输市场规模与越南和中国政府同步进行的监管更新密切相关,两国都在试验基于区块链技术的原产地证书。

在国内,高速公路的发展缩短了前置作业时间,使零售商能够将库存集中到少数几个区域配送中心,同时仍能保证当日送达。在国际航运方面,GEODIS已将越南纳入亚洲公路网,提供保税卡车运输服务至新加坡。凭藉可靠的运输时间保障,空运的高价优势受到挑战。向曼谷和金边出口水果和家具的中小型企业越来越多地选择温控或毛毯包裹的卡车运输服务,其收费系统低于短途航线的同等海运货柜运费。

到2025年,整车运输(FTL)将占80.98%的市场份额,主要受大宗货物运输和合约製造运输的推动。然而,线上零售固有的小额订单正在推动零担运输(LTL)的成长,预计2026年至2031年的复合年增长率将达到6.82%。儘管整车运输在越南公路货运市场仍占据主导地位,但技术赋能的零担共乘模式正日益受到托运人的青睐,他们希望在不牺牲交货时间的前提下降低成本。路线优化演算法将提货点集中在河内和胡志明市附近,然后透过夜间运输的方式将货物拼装到高速公路拖车上,进行南北向的调度。

整车运输业者受益于电子产品和服装出口商提供的稳定货运量,这些出口商拥有年度卡车配额,从而能够根据车辆配置进行定价,以保障利润率。零担运输业者则以自动化分类中心和灵活的交货时间窗口脱颖而出,满足消费者的期望。随着承运商采用数位货运匹配系统,以往未充分利用的卡车货厢空间正被充分利用,逐步提升整个产业的装载率和每吨公里二氧化碳排放。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 按经济活动分類的GDP分配

- 按经济活动分類的GDP成长

- 经济表现及概览

- 电子商务产业的趋势

- 製造业趋势

- 运输和仓储业的GDP

- 物流绩效

- 道路长度

- 出口趋势

- 进口趋势

- 燃油价格趋势

- 卡车运输营运成本

- 按车型分類的卡车拥有数量

- 主要卡车供应商

- 公路货运量趋势

- 公路货运价格趋势

- 透过交通方式分享

- 通货膨胀

- 法律规范

- 价值炼和通路分析

- 市场驱动因素

- 到2030年,高速公路网将迅速扩张至5,000公里。

- 快速发展的电子商务和零售物流

- 电子元件供应链近岸外包外国直接投资激增

- 製造业产出快速成长和工业园区扩张

- 国际金融公司支持的20亿美元基金,用于中小企业物流数位化

- 将电动车和替代燃料卡车引入市政合约

- 市场限制

- 物流成本占GDP的比例持续居高不下。

- 卡车车队老化(90%的车辆车龄超过5年)

- 中老边境等待时间出现瓶颈

- 燃油价格波动和炼油厂停产导致运费上涨

- 市场创新

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 终端用户产业

- 农业、渔业、林业

- 建造

- 製造业

- 石油天然气、采矿和采石

- 批发和零售

- 其他的

- 目的地

- 国内的

- 国际的

- 卡车装载规范

- 整车运输 (FTL)

- 低于100%的运费(零担运输)

- 货柜运输

- 货柜运输

- 非货柜运输

- 距离

- 长途

- 短程交通

- 货物类型

- 液体货物

- 固态货物

- 温度控制

- 非温控型

- 温度控制

第六章 竞争情势

- 市场集中度

- 关键策略倡议

- 市占率分析

- 公司简介

- AP Moller-Maersk

- ASG Corporation

- Aviation Logistics Corporation

- Bee Logistics Corporation

- CMA CGM Group(Including CEVA Logistics)

- DHL Group

- Expeditors International of Washington, Inc.

- Gemadept

- GEODIS

- Hop Nhat International Joint Stock Company

- Indo Trans Logistics Corporation

- Kintetsu Group Holdings Co., Ltd.

- Linfox Pty Ltd.

- MACS Maritime Joint Stock Company

- MP Logistics

- Nguyen Ngoc Logistics Corporation

- Nippon Express Holdings

- NYK(Nippon Yusen Kaisha)Line

- PetroVietnam Transportation Corporation(PVTrans)

- Royal Cargo, Inc.

- Saigon Newport Corporation

- Transimex

- U&I Logistics Corporation

- VNT Logistics

- Viet Total Logistics Co., Ltd.

- Vietnam Foreign Trade Logistics Joint Stock Company(VINATRANS)

- ViettelPost(including Viettel Logistics)

第七章 市场机会与未来展望

The Vietnam road freight transport market was valued at USD 26.27 billion in 2025 and estimated to grow from USD 27.86 billion in 2026 to reach USD 37.36 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031).

This expansion reflects sustained infrastructure spending, expanding industrial clusters, and accelerating digital adoption that collectively improve freight productivity and make shipment visibility the new industry baseline. Continued expressway build-out under the 5,000 km national target compresses north-south transit times, supports predictable lead times for exporters, and underpins competitive routing strategies. Digital freight platforms gain ground as shippers demand instantaneous rate discovery, real-time tracking, and dynamic route optimization, while electric truck pilots in major metro areas signal a gradual shift toward low-emission haulage. Competition remains fragmented even after the April 2025 DSV-DB Schenker merger because local specialists retain intimate route knowledge and strong relationships with Vietnamese manufacturers. Cross-border reforms at smart gate projects further widen the country's gateway role between China and ASEAN trade lanes.

Vietnam Road Freight Transport Market Trends and Insights

Rapid Expressway Expansion to 5,000 Km by 2030

Vietnam aims to complete 5,000 km of expressways by 2030, including the USD 25 billion, 1,811 km North-South backbone that will slash travel time between Hanoi and Ho Chi Minh City by up to 40%. Dedicated freight lanes alleviate congestion on national highways where 90% of trucks currently operate, allowing carriers to boost payload utilization and cut fuel costs. Manufacturers along the corridor gain flexibility to synchronize inbound component flows with production timetables, thereby reducing buffer inventories. New spur links to border checkpoints unlock trade potential with China and Laos, positioning Vietnam as a preferred overland bridge for ASEAN-China cargo. The improved physical network, when paired with tolling interoperability and 4G/5G coverage, supports real-time vehicle diagnostics and route optimization.

Booming E-Commerce and Retail Logistics

Online retail sales are projected to reach USD 57 billion in 2025, a figure that pushes carriers toward hub-and-spoke models and urban micro-fulfillment centers. Average shipment sizes fall even as delivery frequency rises, prompting fleet diversification into smaller vans and refrigerated last-mile vehicles for fresh grocery orders. ViettelPost expanded its cross-border parcel service and embedded API-driven tracking that automates customs clearance at major crossings. Investors fund warehouse robotics and AI-based route planners that reduce failed delivery attempts. Rural outreach strategies add second- and third-tier city spokes to networks, broadening addressable demand while challenging operators to maintain cost efficiency.

Persistently High Logistics-to-GDP Cost Ratio

Vietnam's 16.8% logistics cost-to-GDP ratio in 2024 significantly exceeds the 10-11% levels seen in developed economies. Fragmented transport modes, limited backhaul matching, and cumbersome customs processes inflate delivered-goods pricing and limit road freight adoption among SMEs. Compliance with ISO 22000 and HACCP adds paperwork and cold-chain hardware expenses without matching infrastructure support, especially in rural districts. Exporters incur additional buffer inventories to hedge against uncertain lead times, inflating working capital requirements and weakening competitiveness on price-sensitive agricultural goods.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Near-Shoring FDI for Electronics Supply Chains

- Manufacturing Output Surge and Industrial-Park Build-Out

- Aging Truck Fleet Exceeding Five Years for 90% of Vehicles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing represented 35.12% of 2025 shipments, underscoring how the Vietnam road freight transport market mirrors the nation's pivot into electronics and machinery assembly clusters. Vietnam road freight transport market size for manufacturing-driven consignments is forecast to scale consistently as plant utilization rises and component sourcing deepens domestically. Wholesale and retail trade, propelled by e-commerce, is set to expand faster at a 6.55% CAGR between 2026-2031, stimulating high-frequency replenishment demand that stretches carrier networks into suburban fulfillment nodes. The segment dynamics reward operators that offer SKU-level visibility and temperature-controlled capacity to meet fresh grocery deliveries. Construction cargoes remain stable, anchored by road and port developments, whereas oil and gas projects mandate specialized tubular and rig-component transport that only a handful of heavy-haul carriers can furnish. As traceability mandates tighten in seafood and fruit exports, agriculture shippers invest in IoT-enabled pallets and insulated curtainsider trailers to pass stringent EU and Japanese inspections.

The Vietnam road freight transport market benefits from public-private partnerships that bundle warehouse property with trucking services, giving manufacturers a one-stop logistics solution. High-value electronics consignments rely on real-time geofencing and panic-button technology, elevating security costs but reducing pilferage rates. Multiple freight exchanges arise to match backhaul loads from central provinces, helping reduce empty-run kilometers and slightly easing the sector's cost-to-GDP ratio. At the same time, manufacturers that previously leaned on sea freight for intra-ASEAN moves now deploy road to bridge port congestion or reach regional hubs faster, expanding addressable tonnage for domestic carriers.

Domestic traffic retained a 63.45% share in 2025 as north-south linear geography and two mega-cities anchor consumer demand clusters. Yet international consignments posting a 7.10% CAGR between 2026-2031 point to rising appetite for door-to-door road solutions that circumvent multiple port hand-offs. Customs digitalization at Hữu Nghị is designed to automate up to 50% of paperwork by 2030, cutting clearance time benchmarks and encouraging Vietnamese shippers to book cross-dock truck runs instead of multimodal routings. Vietnam road freight transport market size for cross-border loads is now tied to synchronized regulatory upgrades between Vietnamese and Chinese authorities who trial blockchain-based certificates of origin.

Domestically, the expressway roll-out compresses lead times, enabling retailers to consolidate inventory into fewer regional DCs while still honoring same-day delivery promises. For international moves, GEODIS stitched Vietnam into its Asia Road Network, offering bonded trucking to Singapore with hard transit commitments that challenge airfreight's price premium. SMEs exporting fruit or furniture to Bangkok and Phnom Penh increasingly book temperature-regulated or blanket-wrapped truck services as rates undercut comparable ocean box-rates on short-haul corridors.

Full-truck-load (FTL) commands 80.98% share in 2025 thanks to bulk commodity flows and manufacturing contract carriage. However, fragmented order sizes inherent in online retail lift the LTL growth trajectory to 6.82% CAGR between 2026-2031. Vietnam road freight transport market share for FTL remains high but tech-enabled LTL pooling gains trust among shippers seeking cost savings without sacrificing delivery windows. Route-optimization algorithms cluster pickups around Hanoi and Ho Chi Minh City belts before dispatching consolidated line-haul trailers south- and northbound overnight.

FTL operators enjoy predictable volumes from electronics and apparel exporters that secure annual truck quotas, enabling asset-specific pricing that protects margins. LTL specialists differentiate via automated sortation hubs and configurable delivery slots that satisfy consumer-side expectations. As carriers adopt digital freight matching, previously under-utilized truck deck space is monetized, gradually improving industry load factors and CO2 per-ton-kilometer metrics.

The Vietnam Road Freight Transport Market Report is Segmented by End User Industry (Manufacturing, and More), Destination (Domestic and International), Truckload Specification (FTL and LTL), Distance (Long Haul and Short Haul), Goods Configuration (Fluid Goods and Solid Goods), Temperature Control (Non-Temperature and Temperature Controlled), and by Containerization. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- A.P. Moller-Maersk

- ASG Corporation

- Aviation Logistics Corporation

- Bee Logistics Corporation

- CMA CGM Group (Including CEVA Logistics)

- DHL Group

- Expeditors International of Washington, Inc.

- Gemadept

- GEODIS

- Hop Nhat International Joint Stock Company

- Indo Trans Logistics Corporation

- Kintetsu Group Holdings Co., Ltd.

- Linfox Pty Ltd.

- MACS Maritime Joint Stock Company

- MP Logistics

- Nguyen Ngoc Logistics Corporation

- Nippon Express Holdings

- NYK (Nippon Yusen Kaisha) Line

- PetroVietnam Transportation Corporation (PVTrans)

- Royal Cargo, Inc.

- Saigon Newport Corporation

- Transimex

- U&I Logistics Corporation

- VNT Logistics

- Viet Total Logistics Co., Ltd.

- Vietnam Foreign Trade Logistics Joint Stock Company (VINATRANS)

- ViettelPost (including Viettel Logistics)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 GDP Distribution by Economic Activity

- 4.3 GDP Growth by Economic Activity

- 4.4 Economic Performance and Profile

- 4.4.1 Trends in E-Commerce Industry

- 4.4.2 Trends in Manufacturing Industry

- 4.5 Transport and Storage Sector GDP

- 4.6 Logistics Performance

- 4.7 Length of Roads

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Pricing Trends

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Road Freight Tonnage Trends

- 4.15 Road Freight Pricing Trends

- 4.16 Modal Share

- 4.17 Inflation

- 4.18 Regulatory Framework

- 4.19 Value Chain and Distribution Channel Analysis

- 4.20 Market Drivers

- 4.20.1 Rapid Expressway Expansion to 5,000 Km by 2030

- 4.20.2 Booming E-Commerce and Retail Logistics

- 4.20.3 Surge in Near-Shoring FDI for Electronics Supply Chains

- 4.20.4 Manufacturing Output Surge and industrial-Park Build-Out

- 4.20.5 IFC-Backed USD 2 Billion Fund for SME Logistics Digitalization

- 4.20.6 Adoption of Electric/Alt-Fuel Trucks in Municipal Contracts

- 4.21 Market Restraints

- 4.21.1 Persistently High Logistics-to-GDP Cost Ratio

- 4.21.2 Aging Truck Fleet >5 Yrs for 90 % of Vehicles

- 4.21.3 Border-Crossing Dwell-Time Bottlenecks with China and Laos

- 4.21.4 Volatile Fuel Prices and Refinery Disruptions Raise Haulage Rates

- 4.22 Technology Innovations in the Market

- 4.23 Porter's Five Forces Analysis

- 4.23.1 Threat of New Entrants

- 4.23.2 Bargaining Power of Buyers

- 4.23.3 Bargaining Power of Suppliers

- 4.23.4 Threat of Substitutes

- 4.23.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 A.P. Moller-Maersk

- 6.4.2 ASG Corporation

- 6.4.3 Aviation Logistics Corporation

- 6.4.4 Bee Logistics Corporation

- 6.4.5 CMA CGM Group (Including CEVA Logistics)

- 6.4.6 DHL Group

- 6.4.7 Expeditors International of Washington, Inc.

- 6.4.8 Gemadept

- 6.4.9 GEODIS

- 6.4.10 Hop Nhat International Joint Stock Company

- 6.4.11 Indo Trans Logistics Corporation

- 6.4.12 Kintetsu Group Holdings Co., Ltd.

- 6.4.13 Linfox Pty Ltd.

- 6.4.14 MACS Maritime Joint Stock Company

- 6.4.15 MP Logistics

- 6.4.16 Nguyen Ngoc Logistics Corporation

- 6.4.17 Nippon Express Holdings

- 6.4.18 NYK (Nippon Yusen Kaisha) Line

- 6.4.19 PetroVietnam Transportation Corporation (PVTrans)

- 6.4.20 Royal Cargo, Inc.

- 6.4.21 Saigon Newport Corporation

- 6.4.22 Transimex

- 6.4.23 U&I Logistics Corporation

- 6.4.24 VNT Logistics

- 6.4.25 Viet Total Logistics Co., Ltd.

- 6.4.26 Vietnam Foreign Trade Logistics Joint Stock Company (VINATRANS)

- 6.4.27 ViettelPost (including Viettel Logistics)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

2026-2030年全球公路货运市场

2026-2030年全球公路货运市场 2026年全球公路货运市场报告

2026年全球公路货运市场报告 陆上货运市场:2026-2032年全球市场预测(依服务类型、货物类型、所有权、车辆类型及最终用途划分)

陆上货运市场:2026-2032年全球市场预测(依服务类型、货物类型、所有权、车辆类型及最终用途划分) 公路货运服务市场机会、成长驱动因素、产业趋势分析、预测(2026-2035年)

公路货运服务市场机会、成长驱动因素、产业趋势分析、预测(2026-2035年) 美国公路货运:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)义大利公路货运:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)北美公路货运市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)印度公路货运:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

美国公路货运:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)义大利公路货运:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)北美公路货运市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)印度公路货运:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本公路货运市场报告(依产品类型、目的地、整车规格、货柜化、距离、温控、最终用户和地区划分,2026-2034年)日本公路货运:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

日本公路货运市场报告(依产品类型、目的地、整车规格、货柜化、距离、温控、最终用户和地区划分,2026-2034年)日本公路货运:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)