|

市场调查报告书

商品编码

1716544

非处方宠物药品市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测OTC Pet Medication Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

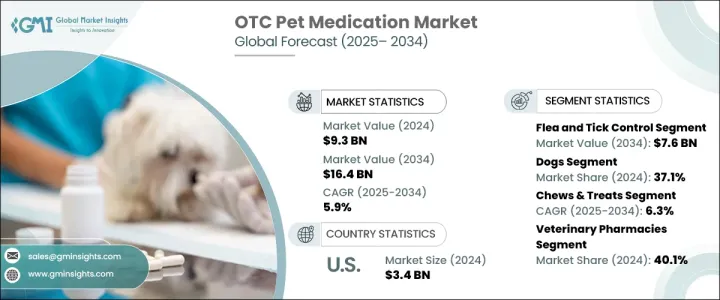

2024 年全球非处方宠物药物市场规模达到 93 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 5.9%。市场的成长主要得益于宠物主人数量的增加和宠物人性化趋势的上升。这种转变导致对更好的医疗保健解决方案和预防性保健产品的需求增加。宠物主人更积极地寻求高品质、方便且有效的非处方 (OTC) 药物来改善宠物的整体健康状况。预防保健意识的不断增强和易于管理的药物的普及极大地促进了市场扩张。

随着宠物主人越来越了解潜在的健康风险,他们正在投资解决常见疾病(如关节炎、皮肤过敏和消化问题)的产品。这一趋势在已开发地区尤其明显,这些地区的可支配收入较高且对宠物健康的高度重视推动了宠物保健支出的增加。此外,包括调味药片和咀嚼片在内的药物配方创新正在提高依从性和治疗效果,进一步刺激市场需求。电子商务平台的日益普及也使得这些产品更容易获得,为全球宠物主人提供了便利和更广泛的选择。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 93亿美元 |

| 预测值 | 164亿美元 |

| 复合年增长率 | 5.9% |

随着宠物遇到越来越多的健康问题,包括寄生虫感染、皮肤病和关节痛,对非处方药的需求也不断增加。骨关节炎是宠物中最常见的疾病之一,尤其是在老年狗和猫中,影响着相当一部分宠物群体。预计关节相关健康问题的高发性将推动对关节补充剂和其他治疗药物的持续需求。此外,人们对预防性医疗保健(如寄生虫控制和皮肤保护)的日益关注也促进了非处方药市场的成长。宠物主人正在采用自然疗法和顺势疗法来解决轻微的健康问题,从而进一步丰富了可用的非处方药产品范围。

2024 年,跳蚤和蜱虫控制领域的市场规模为 42 亿美元。跳蚤和蜱虫传播的媒介传播疾病的日益流行,刺激了对有效控制药物的需求。宠物收养率的上升,加上人们对疾病预防的日益关注,推动了这一领域的快速成长。製造商正在开发先进的配方,提供持久的保护,同时确保易于应用,有助于该领域继续占据主导地位。

非处方宠物药物市场根据宠物类型进行分类,包括狗、猫、鸟、鱼、爬行动物等。 2024 年,狗占据了 37.1% 的市场。狗的健康问题发生率很高,加上医疗支出增加和户外活动使它们更容易受到寄生虫感染,这促使製造商优先开发适合犬类健康的药物。宠物主人越来越多地寻求解决方案来确保他们的狗保持健康,从而推动该领域的持续成长。

2024 年美国非处方宠物药物市场价值为 34 亿美元,预计在整个预测期内仍将是最大的市场。人们对宠物护理和宠物人性化的认识不断提高是美国市场成长的主要驱动力,宠物主人变得更加警惕和积极主动地寻求先进的解决方案来维护宠物的健康和福祉。创新配方的出现以及电子商务平台的日益普及使得非处方宠物药物更加容易获得,确保了未来几年强劲的市场表现。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 宠物拥有率上升

- 越来越重视宠物的预防性医疗保健

- 人畜共通传染病的盛行率不断上升

- 电子商务与网路零售的扩张

- 动物保健支出不断增长

- 产业陷阱与挑战

- 严格的监管标准

- 潜在的副作用和误用

- 成长动力

- 成长潜力分析

- 监管格局

- 未来市场趋势

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按药物类型,2021 年至 2034 年

- 主要趋势

- 跳蚤和蜱虫控制

- 驱虫药和杀寄生虫药

- 止痛药和过敏药

- 皮肤和毛髮护理

- 牙科护理

- 营养补充品

- 行为和焦虑缓解药物

- 其他药物类型

第六章:市场估计与预测:按宠物类型,2021 年至 2034 年

- 主要趋势

- 狗

- 猫

- 鸟类

- 鱼类和爬虫类

- 其他宠物类型

第七章:市场估计与预测:按剂型,2021 年至 2034 年

- 主要趋势

- 咀嚼物和零食

- 胶囊

- 喷雾剂

- 软膏

- 其他剂型

第八章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 兽医药房

- 宠物专卖店

- 线上零售商

- 其他分销管道

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- AdvaCare Pharma

- Bimeda

- Boehringer Ingelheim International

- Ceva Sante Animale

- Dechra

- Elanco Animal Health

- Heska Corporation

- Merck & Co.

- Norbrook

- Nutramax Laboratories Consumer Care

- PetIQ

- Phibro Animal Health

- Vetenex Animal Health

- Vetoquinol

- Virbac

- Zoetis

The Global OTC Pet Medication Market reached USD 9.3 billion in 2024 and is expected to grow at a CAGR of 5.9% between 2025 and 2034. The market's growth is primarily fueled by the increasing number of pet owners and the rising trend of pet humanization. This shift has led to heightened demand for better healthcare solutions and preventive wellness products. Pet owners are more proactive in seeking high-quality, accessible, and effective over-the-counter (OTC) medications to improve their pets' overall health. Growing awareness of preventive care and the availability of easy-to-administer medications have significantly contributed to the market expansion.

As pet owners become increasingly informed about potential health risks, they are investing in products that address common conditions such as arthritis, skin allergies, and digestive issues. This trend is particularly prominent in developed regions, where higher disposable income and a strong emphasis on pet well-being drive higher spending on pet healthcare. Moreover, innovations in medication formulations, including flavored tablets and chewables, are enhancing compliance and treatment effectiveness, further boosting market demand. The growing presence of e-commerce platforms has also made these products more accessible, offering convenience and a broader range of options for pet owners globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.3 Billion |

| Forecast Value | $16.4 Billion |

| CAGR | 5.9% |

As pets encounter a growing range of health issues, including parasitic infections, skin disorders, and joint pain, the need for OTC medications continues to rise. Osteoarthritis is one of the most prevalent conditions in pets, particularly in aging dogs and cats, affecting a significant portion of the pet population. The high incidence of joint-related health problems is expected to drive sustained demand for joint supplements and other therapeutic medications. Additionally, the increasing focus on preventative healthcare, such as parasite control and skin protection, is contributing to the growing market for OTC solutions. Pet owners are turning to natural and homeopathic remedies to address minor health concerns, further diversifying the range of available OTC products.

The flea and tick control segment accounted for USD 4.2 billion in 2024. The increasing prevalence of vector-borne diseases transmitted by fleas and ticks has fueled the demand for effective control medications. Rising pet adoption rates, coupled with growing concerns about disease prevention, are driving this segment's rapid growth. Manufacturers are developing advanced formulations that offer long-lasting protection while ensuring ease of application, contributing to the segment's continued dominance.

The OTC pet medication market is categorized based on pet type, including dogs, cats, birds, fish, reptiles, and others. Dogs accounted for 37.1% of the market share in 2024. The high prevalence of health issues in dogs, combined with increased healthcare spending and outdoor exposure that makes them more vulnerable to parasitic infections, has led manufacturers to prioritize developing medications tailored to canine health. Pet owners are increasingly seeking solutions to ensure their dogs remain healthy, driving sustained growth in this segment.

The U.S. OTC pet medication market was valued at USD 3.4 billion in 2024 and is expected to remain the largest market throughout the forecast period. Growing awareness about pet care and the humanization of pets are key drivers of market growth in the U.S. Pet owners are becoming more vigilant and proactive in seeking advanced solutions to maintain the health and well-being of their pets. The availability of innovative formulations and increasing access to e-commerce platforms are making OTC pet medications more accessible, ensuring strong market performance in the coming years.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership rate

- 3.2.1.2 Growing emphasis on preventive healthcare for pets

- 3.2.1.3 Increasing prevalence of zoonotic diseases

- 3.2.1.4 Expansion of e-commerce & online retailing

- 3.2.1.5 Growing animal healthcare expenditure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory standards

- 3.2.2.2 Potential side effects & misuse

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Medication Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Flea and tick control

- 5.3 Dewormers & parasiticides

- 5.4 Pain relievers & allergy medications

- 5.5 Skin and coat care

- 5.6 Dental care

- 5.7 Nutritional supplements

- 5.8 Behavioral & anxiety relief medications

- 5.9 Other medication types

Chapter 6 Market Estimates and Forecast, By Pet Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Birds

- 6.5 Fishes & reptiles

- 6.6 Other pet types

Chapter 7 Market Estimates and Forecast, By Dosage Form, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Chews & treats

- 7.3 Capsules

- 7.4 Sprays

- 7.5 Ointments

- 7.6 Other dosage forms

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary pharmacies

- 8.3 Pet specialty stores

- 8.4 Online retailers

- 8.5 Other distribution channels

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AdvaCare Pharma

- 10.2 Bimeda

- 10.3 Boehringer Ingelheim International

- 10.4 Ceva Sante Animale

- 10.5 Dechra

- 10.6 Elanco Animal Health

- 10.7 Heska Corporation

- 10.8 Merck & Co.

- 10.9 Norbrook

- 10.10 Nutramax Laboratories Consumer Care

- 10.11 PetIQ

- 10.12 Phibro Animal Health

- 10.13 Vetenex Animal Health

- 10.14 Vetoquinol

- 10.15 Virbac

- 10.16 Zoetis