|

市场调查报告书

商品编码

1959294

食品废弃物衍生的植物色素市场机会、成长要素、产业趋势分析及预测(2026-2035年)Plant-based Colors from Food Waste Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

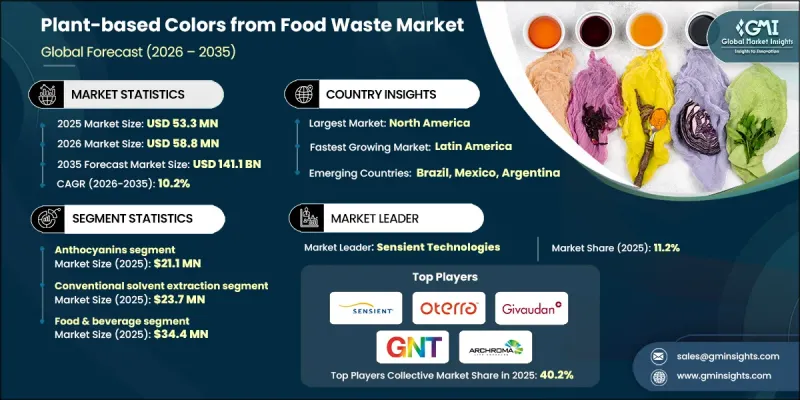

2025 年全球食品废弃物衍生植物色素市场价值为 5,330 万美元,预计到 2035 年将达到 1.411 亿美元,年复合成长率为 10.2%。

该市场专注于从食品加工和收穫后后处理过程中产生的植物废弃物中回收的天然色素。这些色素提取自未充分利用的植物成分,并转化为可用于各行业的商业性原料。主要色素类别包括花青素、类胡萝卜素、叶绿素和甜菜碱,它们采用专门的加工技术进行回收,以保持色彩强度和功能稳定性。将植物来源的废弃物转化为天然着色剂,有助于实现循环经济目标,减少掩埋负担,并降低对合成染料的依赖。除了环境效益外,这些色素通常还含有具有抗氧化和抗菌特性的生物活性化合物,从而提升了其提案。这种方法提高了资源利用效率,同时为农业和食品加工产业创造了新的收入来源。消费者对透明度、洁净标示配方和无毒成分的需求日益增长,正在加速食品、纺织、化妆品和包装应用领域的采用。随着永续性成为品牌形象的核心,源自食品废弃物的植物色素在全球供应链中正发挥越来越重要的策略作用。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 5330万美元 |

| 预测金额 | 1.411亿美元 |

| 复合年增长率 | 10.2% |

随着消费者寻求环保且可生物降解的合成染料替代品,天然食品废弃物衍生的染料正日益受到欢迎。洁净标示标籤的兴起、合成添加剂管制的放鬆以及消费者对产品安全意识的增强,都在推动这一转变。与传统的合成色素不同,植物来源染料更符合环保品牌概念和健康消费习惯。其可再生资源和较低的环境影响,使其成为专注于永续创新的製造商的理想选择。

预计到2025年,传统溶剂萃取市场规模将达2,370万美元。由于其操作简便、成本效益高且资本投入相对较低,此方法仍被广泛应用。它继续支持大规模染料回收,尤其是在基础设施受限、技术应用受限的新兴市场。然而,业内相关人员正日益评估先进的萃取技术,以提高回收率、减少溶剂残留并最大限度地减少对环境的影响,同时保持染料的品质和稳定性。

预计到2025年,食品饮料产业将创造3,440万美元的收入。该产业的强劲成长主要得益于消费者对原材料透明度和可追溯来源的需求。製造商正将源自食品废弃物的植物性色素添加到产品配方中,以取代合成色素并符合监管标准。这些天然色素不仅能为饮料、乳製品、点心和糖果甜点等产品带来鲜艳的视觉效果,还能提升产品的永续性。随着品牌优先考虑负责任的采购和清洁的配方,食品饮料行业的需求仍然强劲。

预计到2035年,北美食品废弃物衍生植物色素市场规模将从2025年的2,200万美元成长至5,080万美元。这一区域扩张的驱动力在于消费者对天然成分日益增长的认知以及产业对环境管理的坚定承诺。食品、饮料和化妆品製造商正投资于将农产品转化为高价值色素的技术,以推进循环生产目标。旨在减少合成添加剂使用的监管措施也进一步推动了市场成长。凭藉成熟的供应链和创新主导的经营模式,北美有望成为全球收入成长的主要贡献者。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 对天然颜料的需求日益增长

- 扩大植物来源和洁净标示产品的范围

- 技术进步

- 产业潜在风险与挑战

- 高昂的生产成本

- 来自合成染料的竞争压力

- 市场机会

- 融入化妆品和製药业

- 与食品加工公司合作

- 功能色彩创新

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依颜料类型

- 未来市场趋势

- 专利状态

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 考虑碳足迹

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 市场估算与预测:依颜料类型划分,2022-2035年

- 花青素

- 贝塔兰

- 类胡萝卜素

- 叶绿素

- 藻胆蛋白

第六章 市场估算与预测:依萃取技术划分,2022-2035年

- 传统溶剂萃取

- 超音波辅助拔牙(UAE)

- 微波辅助萃取(MAE)

- 超临界流体萃取(SFE)

- 酵素辅助萃取(EAE)

- 脉衝场法(PEF)

- 加压液体萃取(PLE)

- 精准发酵和生物技术

- 混合整合萃取系统

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 食品/饮料

- 化妆品和个人护理

- 纺织与时尚

- 药品和营养补充剂

- 其他的

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- Sensient Technologies Corporation

- Chr. Hansen Holdings(Oterra)

- Givaudan SA

- Givaudan Sense Colour

- GNT Group

- Archroma(EarthColors)

- Prodalim(Upcycled Colors)

- E. &J. Gallo Winery(Natural Colorants Division)

- KAIKU(UK)

The Global Plant-based Colors from Food Waste Market was valued at USD 53.3 million in 2025 and is estimated to grow at a CAGR of 10.2% to reach USD 141.1 million by 2035.

The market focuses on natural pigments recovered from discarded plant materials generated during food processing and post-harvest handling. These colorants are extracted from underutilized plant fractions and transformed into commercially viable ingredients for multiple industries. Key pigment groups include anthocyanins, carotenoids, chlorophylls, and betalains, which are recovered through specialized processing techniques designed to preserve color intensity and functional stability. Converting plant-based waste streams into natural color solutions supports circular economy objectives by reducing landfill burden and lowering reliance on synthetic dyes. In addition to environmental benefits, these pigments often contain bioactive compounds with antioxidant and antimicrobial properties, enhancing their value proposition. The approach creates new revenue channels for agricultural and food-processing industries while improving resource efficiency. Rising consumer demand for transparency, clean-label formulations, and non-toxic ingredients is accelerating adoption across food, textile, cosmetic, and packaging applications. As sustainability becomes central to brand identity, plant-based colors sourced from food waste are gaining strategic importance in global supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $53.3 Million |

| Forecast Value | $141.1 Million |

| CAGR | 10.2% |

Natural pigments derived from food waste are increasingly preferred as consumers seek environmentally responsible and biodegradable alternatives to artificial dyes. Clean-label positioning, regulatory shifts away from synthetic additives, and growing awareness of product safety are reinforcing this transition. Unlike conventional synthetic colorants, plant-based pigments align with eco-conscious branding and wellness-driven purchasing behavior. Their renewable origin and reduced environmental footprint make them attractive to manufacturers focused on sustainable innovation.

The conventional solvent extraction segment accounted for USD 23.7 million in 2025. This method remains widely utilized due to its operational simplicity, cost-effectiveness, and relatively low capital requirements. It continues to support large-scale pigment recovery, particularly in emerging markets where infrastructure constraints influence technology adoption. However, industry participants are increasingly evaluating advanced extraction approaches to improve yield efficiency, reduce solvent residues, and minimize environmental impact while maintaining pigment quality and stability.

The food & beverage segment generated USD 34.4 million in 2025. Strong growth in this sector is driven by consumer demand for ingredient transparency and traceable sourcing. Manufacturers are incorporating food waste-derived plant-based colors into product formulations to replace synthetic alternatives and meet regulatory standards. These natural pigments deliver vibrant visual appeal across beverages, dairy products, snacks, and confectionery applications while reinforcing sustainability narratives. As brands emphasize responsible sourcing and cleaner formulations, demand within the food and beverage industry continues to strengthen.

North America Plant-based Colors from Food Waste Market is projected to grow from USD 22 million in 2025 to USD 50.8 million by 2035. Regional expansion is supported by heightened consumer awareness regarding natural ingredients and strong industry commitment to environmental stewardship. Food, beverage, and cosmetic manufacturers are investing in technologies that convert agricultural by-products into high-value pigments to advance circular production goals. Regulatory initiatives aimed at reducing synthetic additive usage further stimulate market growth. Established supply chains and innovation-driven business models position North America as a key contributor to global revenue expansion.

Major companies operating in the Global Plant-based Colors from Food Waste Market include GNT Group, Sensient Technologies Corporation, Chr. Hansen Holdings (Oterra), Givaudan SA, Givaudan Sense Colour, Archroma (EarthColors), Prodalim (Upcycled Colors), E. & J. Gallo Winery (Natural Colorants Division), and KAIKU (UK). These organizations are actively developing advanced pigment extraction technologies and expanding sustainable ingredient portfolios to strengthen their competitive presence. Companies in the plant-based colors from food waste market are reinforcing their market position through investment in research and development to improve pigment stability, color intensity, and application versatility. Strategic collaborations with food processors and agricultural suppliers secure consistent raw material streams and enhance traceability. Many firms are adopting proprietary extraction technologies that increase yield efficiency while reducing environmental impact. Sustainability certifications and transparent sourcing practices are being leveraged to build brand credibility and consumer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Pigment Type

- 2.2.2 Extraction Technology

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for natural colors

- 3.2.1.2 Expansion of plant-based and clean-label products

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Competitive pressure from synthetic colors

- 3.2.3 Market opportunities

- 3.2.3.1 Integration into cosmetic and pharmaceutical industries

- 3.2.3.2 Collaborations with food processing companies

- 3.2.3.3 Innovation in functional colors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By Pigment type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Pigment Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Anthocyanins

- 5.3 Betalains

- 5.4 Carotenoids

- 5.5 Chlorophylls

- 5.6 Phycobiliproteins

Chapter 6 Market Estimates and Forecast, By Extraction Technology, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Conventional solvent extraction

- 6.3 Ultrasound-assisted extraction (UAE)

- 6.4 Microwave-assisted extraction (MAE)

- 6.5 Supercritical fluid extraction (SFE)

- 6.6 Enzyme-assisted extraction (EAE)

- 6.7 Pulsed electric field (PEF)

- 6.8 Pressurized liquid extraction (PLE)

- 6.9 Precision fermentation & biotechnology

- 6.10 Hybrid & integrated extraction systems

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Cosmetics & personal care

- 7.4 Textile & fashion

- 7.5 Pharmaceutical & nutraceutical

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Sensient Technologies Corporation

- 9.2 Chr. Hansen Holdings (Oterra)

- 9.3 Givaudan SA

- 9.4 Givaudan Sense Colour

- 9.5 GNT Group

- 9.6 Archroma (EarthColors)

- 9.7 Prodalim (Upcycled Colors)

- 9.8 E. & J. Gallo Winery (Natural Colorants Division)

- 9.9 KAIKU (UK)

2026年全球食品废弃物管理市场报告

2026年全球食品废弃物管理市场报告 全球食品废弃物管理市场规模、份额、趋势和成长分析报告(2026-2034年)

全球食品废弃物管理市场规模、份额、趋势和成长分析报告(2026-2034年) 食品废弃物管理市场-全球产业规模、份额、趋势、机会及预测(依废弃物类型、处理流程、来源、应用、地区及竞争格局划分),2021-2031年

食品废弃物管理市场-全球产业规模、份额、趋势、机会及预测(依废弃物类型、处理流程、来源、应用、地区及竞争格局划分),2021-2031年 全球升级改造宠物用品市场:预测至2032年-依材料种类、原料、形状、宠物类型、加工技术、应用及地区进行分析

全球升级改造宠物用品市场:预测至2032年-依材料种类、原料、形状、宠物类型、加工技术、应用及地区进行分析 食品废弃物管理市场规模、份额及成长分析(按废弃物类型、来源、处理流程和地区划分)-2026-2033年产业预测2032年食品废弃物减量技术市场预测:按技术类型、应用和地区分類的全球分析

食品废弃物管理市场规模、份额及成长分析(按废弃物类型、来源、处理流程和地区划分)-2026-2033年产业预测2032年食品废弃物减量技术市场预测:按技术类型、应用和地区分類的全球分析 食品垃圾回收市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)食品包装回收市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)全球食品废弃物管理市场-2025-2030年预测全球食品废弃物管理市场:预测至2032年-依废弃物类型、来源、服务、规模/部署方式、最终产品和地区进行分析

食品垃圾回收市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)食品包装回收市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)全球食品废弃物管理市场-2025-2030年预测全球食品废弃物管理市场:预测至2032年-依废弃物类型、来源、服务、规模/部署方式、最终产品和地区进行分析