|

市场调查报告书

商品编码

1885887

食品垃圾回收市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Food Waste Recycling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

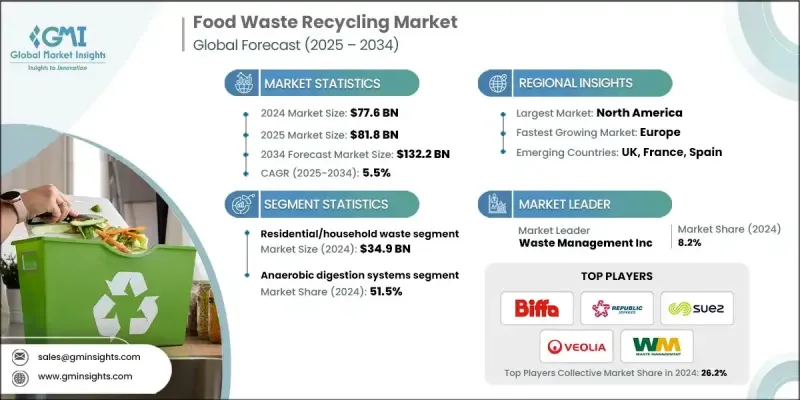

2024 年全球食品废弃物回收市场价值为 776 亿美元,预计到 2034 年将以 5.5% 的复合年增长率成长至 1,322 亿美元。

人们日益关注食物废弃物对环境的影响,包括垃圾掩埋场的甲烷排放以及日益增长的废弃物处理系统压力,这正加速全球对回收解决方案的采用。食物垃圾回收有助于将有机废弃物转化为堆肥、沼气和饲料级产品等有价值的产出,从而减少垃圾掩埋场的使用,并推动永续的废弃物管理实践。多个地区的政府持续实施鼓励大规模回收项目的政策,从而促进了该行业的成长。北美凭藉完善的基础设施和强有力的监管支持保持领先地位,而欧洲则凭藉严格的可持续发展指令和对先进废物处理技术不断增长的投资,正在迅速发展。厌氧消化、堆肥和再生能源途径的发展正在重塑营运效率,并提高回收产出的品质。人工智慧和物联网驱动的自动化和智慧监控技术正在增强可扩展性,减少营运障碍,并支援市政和私营部门更广泛地采用这些技术。这些因素共同促成了全球食物垃圾回收产业的强劲前景。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 776亿美元 |

| 预测值 | 1322亿美元 |

| 复合年增长率 | 5.5% |

2024年,住宅和家庭垃圾处理市场规模达到3,49亿美元,并持续占据主导地位,这主要归因于消费者层麵食物垃圾的大量丢弃。城市人口的成长和公众对永续生活方式意识的提高推动了这一领域的成长:社区倡议和政府支持的鼓励家庭垃圾分类的项目进一步促进了公众的广泛参与。住宅垃圾回收解决方案的经济性和便利性也吸引了希望加强在该领域推广的市场参与者。

2024年,厌氧消化系统占据了51.5%的市场。该技术能够将有机废弃物转化为再生能源和富含营养的消化液,从而巩固了其领先地位。这些系统有助于减少温室气体排放,并支持环境永续发展目标,因此在致力于降低碳足迹的地区备受青睐。强大的能源回收潜力持续加速着该领域的创新和应用。

预计2025年至2034年间,北美食品废弃物回收市场将以5.5%的复合年增长率成长。随着企业和消费者日益重视减少浪费和环保行为,食品垃圾回收的普及率正在上升。市场对能够将食品废弃物转化为有机肥料、生物能源和再生能源等可销售产品的现代化回收解决方案的需求不断增强,这反映出资源循环利用的趋势。

活跃于食品垃圾回收市场的主要公司包括 Waste Management Inc.、苏伊士集团 (SUEZ Group)、威立雅 (Veolia)、Ridan 食品垃圾堆肥公司、Republic Services、Clear Earth Recycling、Alfa Therm Limited、Skip Shapiro Enterprises LLC、Biffa 和 FoodCycler。这些公司透过扩大处理能力、整合先进的废弃物资源化技术以及采用可持续的营运模式来增强自身的竞争优势。许多公司致力于透过自动化、即时追踪工具和数位化废弃物管理平台来优化回收效率。多元化的服务产品,包括生物能源生产、有机肥料解决方案和客製化的废弃物处理方案,有助于建立长期的客户合作关係。此外,各公司还优先考虑合规性,并与市政当局合作,以获得大型合约并提高区域回收率。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 垃圾掩埋成本和限制不断上涨

- 监管指令和政策支持

- 循环经济的采用

- 产业陷阱与挑战

- 原料品质与污染问题

- 技术标准化差距

- 市场机会

- 数位平台开发

- 新兴技术整合

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按原料来源

- 未来市场趋势

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依原料来源划分,2021-2034年

- 主要趋势

- 居民/家庭垃圾

- 商业食品服务

- 餐厅和咖啡馆

- 饭店及餐饮业

- 机构厨房

- 餐饮服务

- 食品零售

- 杂货店和超市

- 便利商店

- 农夫市集

- 食品加工与製造

- 蔬果加工

- 肉类和家禽加工

- 乳製品加工

- 饮料製造

- 农业来源

- 农场作物残茬

- 牲畜粪便

- 水产养殖废料

第六章:市场估算与预测:依製程划分,2021-2034年

- 主要趋势

- 厌氧消化系统

- 堆肥系统

- 机械生物处理

- 其他的

第七章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 能源产品

- 沼气和生物甲烷

- 再生天然气(RNG)

- 发电

- 土壤改良产品

- 堆肥

- 消化物

- 生物炭

- 液态肥料

- 饲料和蛋白质产品

- 昆虫蛋白粉

- 动物饲料

- 水产饲料

- 工业产品

- 生物塑胶和聚合物

- 生物化学物质

- 包装材料

- 其他的

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- Alfa Therm Limited

- Biffa

- Clear Earth Recycling

- FoodCycler

- Republic Services

- Ridan food waste composters

- Skip Shapiro Enterprises, LLC

- SUEZ Group

- Veolia

- Waste Management Inc.

The Global Food Waste Recycling Market was valued at USD 77.6 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 132.2 billion by 2034.

Rising awareness of the environmental impact of discarded food, including methane emissions from landfills and increasing pressure on waste systems, is accelerating the adoption of recycling solutions worldwide. Food waste recycling supports the conversion of organic waste into valuable outputs such as compost, biogas, and feed-grade products, helping reduce landfill use and advancing sustainable waste management practices. Governments across multiple regions continue to implement policies that encourage large-scale recycling programs, strengthening industry growth. North America maintains a leading position due to established infrastructure and strong regulatory backing, whereas Europe is expanding rapidly with stringent sustainability directives and rising investments in advanced waste-processing technologies. Developments in anaerobic digestion, composting, and renewable energy pathways are reshaping operational efficiency and improving the quality of recycled outputs. Automation and smart monitoring technologies driven by AI and IoT are enhancing scalability, reducing operational barriers, and supporting broader adoption across municipalities and private sectors. These factors collectively contribute to a strong global outlook for the food waste recycling industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $77.6 Billion |

| Forecast Value | $132.2 Billion |

| CAGR | 5.5% |

The residential and household segment generated USD 34.9 billion in 2024 and continues to dominate because of the high volume of food discarded at the consumer level. Growth in this category is supported by rising urban populations and expanding public awareness of sustainable living practices: community initiatives and government-backed programs encouraging household waste diversion further support widespread participation. The affordability and simplicity of residential recycling solutions also attract market participants looking to strengthen outreach in this segment.

The anaerobic digestion systems captured a 51.5% share in 2024. Their leading position is reinforced by the technology's ability to convert organic waste into renewable energy and nutrient-rich digestate. These systems help reduce greenhouse gas emissions and support environmental sustainability goals, making them favored across regions focused on lowering carbon footprints. Strong energy recovery potential continues to accelerate innovation and deployment in this category.

North America Food Waste Recycling Market is expected to grow at a CAGR of 5.5% between 2025 and 2034. Adoption rates are rising as businesses and consumers increasingly prioritize waste reduction and environmentally responsible behaviors. Demand is strengthening for modern recycling solutions capable of transforming food waste into marketable products such as organic fertilizers, bioenergy, and renewable power sources, reflecting a shift toward circular resource utilization.

Key companies active in the Food Waste Recycling Market include Waste Management Inc., SUEZ Group, Veolia, Ridan food waste composters, Republic Services, Clear Earth Recycling, Alfa Therm Limited, Skip Shapiro Enterprises LLC, Biffa, and FoodCycler. Companies in the Food Waste Recycling Market reinforce their competitive edge by expanding processing capacity, integrating advanced waste-to-resource technologies, and adopting sustainable operating models. Many focus on optimizing recycling efficiency through automation, real-time tracking tools, and digitally enabled waste management platforms. Diversification of service offerings, including bioenergy production, organic fertilizer solutions, and customized waste handling programs, supports long-term client partnerships. Firms also prioritize regulatory compliance and collaborate with municipalities to secure large-scale contracts and improve regional recycling rates.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Feedstock source trends

- 2.2.2 Process trends

- 2.2.3 End Use trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising landfill costs & restrictions

- 3.2.1.2 Regulatory mandates & policy support

- 3.2.1.3 Circular economy adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Feedstock quality & contamination issues

- 3.2.2.2 Technology standardization gaps

- 3.2.3 Market opportunities

- 3.2.3.1 Digital platform development

- 3.2.3.2 Emerging technology integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By feedstock source

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Feedstock Source, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Residential/household waste

- 5.3 Commercial food service

- 5.3.1 Restaurants & cafeterias

- 5.3.2 Hotels & hospitality

- 5.3.3 Institutional kitchens

- 5.3.4 Catering services

- 5.4 Food retail

- 5.4.1 Grocery stores & supermarkets

- 5.4.2 Convenience stores

- 5.4.3 Farmers markets

- 5.5 Food processing & manufacturing

- 5.5.1 Fruit & vegetable processing

- 5.5.2 Meat & poultry processing

- 5.5.3 Dairy processing

- 5.5.4 Beverage manufacturing

- 5.6 Agricultural sources

- 5.6.1 On-farm crop residues

- 5.6.2 Livestock manure

- 5.6.3 Aquaculture waste

Chapter 6 Market Estimates and Forecast, By Process, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Anaerobic digestion systems

- 6.3 Composting system

- 6.4 Mechanical biological treatment

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Energy products

- 7.2.1 Biogas & biomethane

- 7.2.2 Renewable natural gas (RNG)

- 7.2.3 Electricity generation

- 7.3 Soil amendment products

- 7.3.1 Compost

- 7.3.2 Digestate

- 7.3.3 Biochar

- 7.3.4 Liquid fertilizers

- 7.4 Feed & protein products

- 7.4.1 Insect protein meal

- 7.4.2 Animal feed

- 7.4.3 Aquaculture feed

- 7.5 Industrial products

- 7.5.1 Bioplastics & polymers

- 7.5.2 Biochemicals

- 7.5.3 Packaging materials

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Alfa Therm Limited

- 9.2 Biffa

- 9.3 Clear Earth Recycling

- 9.4 FoodCycler

- 9.5 Republic Services

- 9.6 Ridan food waste composters

- 9.7 Skip Shapiro Enterprises, LLC

- 9.8 SUEZ Group

- 9.9 Veolia

- 9.10 Waste Management Inc.

2026年全球食品废弃物管理市场报告

2026年全球食品废弃物管理市场报告 食品废弃物衍生的植物色素市场机会、成长要素、产业趋势分析及预测(2026-2035年)

食品废弃物衍生的植物色素市场机会、成长要素、产业趋势分析及预测(2026-2035年) 全球食品废弃物管理市场规模、份额、趋势和成长分析报告(2026-2034年)

全球食品废弃物管理市场规模、份额、趋势和成长分析报告(2026-2034年) 食品废弃物管理市场-全球产业规模、份额、趋势、机会及预测(依废弃物类型、处理流程、来源、应用、地区及竞争格局划分),2021-2031年

食品废弃物管理市场-全球产业规模、份额、趋势、机会及预测(依废弃物类型、处理流程、来源、应用、地区及竞争格局划分),2021-2031年 全球升级改造宠物用品市场:预测至2032年-依材料种类、原料、形状、宠物类型、加工技术、应用及地区进行分析

全球升级改造宠物用品市场:预测至2032年-依材料种类、原料、形状、宠物类型、加工技术、应用及地区进行分析 食品废弃物管理市场规模、份额及成长分析(按废弃物类型、来源、处理流程和地区划分)-2026-2033年产业预测2032年食品废弃物减量技术市场预测:按技术类型、应用和地区分類的全球分析食品包装回收市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)全球食品废弃物管理市场-2025-2030年预测全球食品废弃物管理市场:预测至2032年-依废弃物类型、来源、服务、规模/部署方式、最终产品和地区进行分析

食品废弃物管理市场规模、份额及成长分析(按废弃物类型、来源、处理流程和地区划分)-2026-2033年产业预测2032年食品废弃物减量技术市场预测:按技术类型、应用和地区分類的全球分析食品包装回收市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)全球食品废弃物管理市场-2025-2030年预测全球食品废弃物管理市场:预测至2032年-依废弃物类型、来源、服务、规模/部署方式、最终产品和地区进行分析