|

市场调查报告书

商品编码

1637798

泰国石油和天然气 -市场占有率分析、行业趋势、成长预测(2025-2030 年)Thailand Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

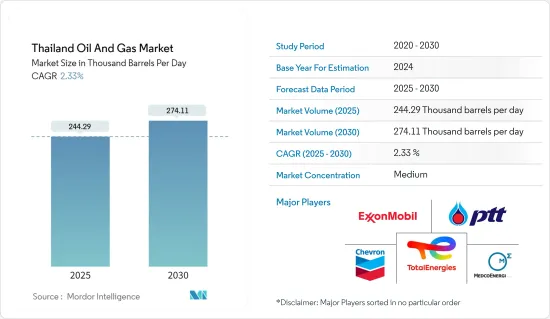

预计2025年泰国石油和天然气市场规模为244,290桶/日,预计2030年将达到274,110桶/日,预测期间(2025-2030年)复合年增长率为2.33%。

主要亮点

- 从中期来看,天然气管道容量增加和石油产品需求等因素预计将在预测期内推动泰国石油和天然气市场的发展。

- 同时,该国向可再生能源转型的新计划可能会阻碍泰国的石油和天然气市场。

- 新天然气田的发现预计将在预测期内为泰国石油和天然气市场创造多个机会。

泰国石油和天然气市场趋势

下游产业可望大幅成长

- 下游部门对应于石油和天然气运往最终客户或零售市场之前的最终过程。此製程生产的主要产品包括汽油、液化天然气、柴油和其他润滑油。

- 2022年,泰国石油产品出口量达到约191,300桶/日,较上年略有成长。同年,泰国出口的柴油比其他石油产品都多。

- 泰国的精製下游产业(精製能力和加工能力)在东南亚地区市值排名第二,仅次于新加坡。近年来,由于国内石油需求增加、油价上涨、旅游业健康发展以及稳定且较高的精製利润,精製能力不断成长。

- 另一方面,炼油厂加工能力近年来不断增加。该国目前拥有六座炼油厂,其中大部分由该国国有石油和天然气集团 PTT 部分或全部拥有。泰国正在提高精製能力,以满足不断增长的国内和地区需求。

- 泰国领先的精製泰国石油公司已决定斥资约 48 亿美元扩建其位于林查班是是拉差香甜辣椒酱炼油厂的现有原油精製。

- 扩建还包括增加渣油加氢裂解装置、真空瓦斯油加氢裂解装置、氢气製造装置、柴油加氢脱硫装置、石脑油加氢裂解装置、硫回收装置和以渣油沥青为燃料的发电厂。

- 2021 年 8 月,现代工程公司从 IRPC PCL订单了价值 2.56 亿美元的 EPC(设计、采购和施工)合同,用于维修日产位于曼谷东南约 170 公里的罗勇府的 215,000 桶炼油厂。现代汽车表示,该项目预计按照 IRPC 的计划于 2024 年初完成。

- 如上所述,由于炼油厂扩建和精製油需求增加,预计泰国的精製能力将在预测期内略有增加。

从煤炭到天然气的能源转型前景将推动市场

- 为了满足国际上对无污染燃料能源的需求,并将碳排放减少到净零,泰国已经宣布从煤炭经济转型为天然气经济。

- 泰国充分意识到其天然气蕴藏量正在耗尽,因此已经开始透过开发各种港口基础设施来涉足液化天然气(LNG)领域。最近完工的非工厂液化LNG接收站的产能为每年 750 万吨,成为该国转型为天然气的典范。

- 2022年,泰国天然气消费量达到约507亿立方米,较上年略有成长。 2022年泰国天然气消费量将成长10%。

- 泰国有多个兴建中的发电厂,包括Gulf 是拉差香甜辣椒酱发电厂(2.5吉瓦)、Hin Kong计划(1.4吉瓦)、春武里吴计划发电厂(2.6吉瓦)以及素叻府的两座发电厂(700兆瓦)每个)有几个天然气发电厂。随着这些发电厂的运作,泰国的天然气需求预计将增加。

- 2021年2月,泰国国家石油公司PTT宣布,计画2021年至2025年在所有业务上投资283亿美元。 PTT 专注于发展该国的液化天然气和天然气产业,探索未来的能源机会。

- 因此,鑑于上述情况,预计该国不断上升的能源转型将在预测期内推动石油和天然气市场的发展。

泰国石油天然气产业概况

泰国的石油和天然气市场是半固定的。市场主要企业包括(排名不分先后)PTT Public Company Limited、雪佛龙公司、埃克森美孚、TotalEnergies SE 和 MedcoEnergi。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2028年之前的原油产量预测

- 天然气产量:预测至 2028 年

- 炼油厂装置容量及预测至2028年

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 亚洲最大下游产业扩张

- 从煤炭到天然气的能源转型

- 抑制因素

- 政府采取措施转向清洁燃料

- 促进因素

- 供应链分析

- PESTLE分析

第五章市场区隔:依行业

- 上游

- 中产阶级

- 下游

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- PTT Public Company Limited

- Chevron Corporation

- MedcoEnergi

- Bangchak Corporation PCL

- Pan Orient Energy(Siam)Ltd.

- Sea Oil Energy Limited

- Royal Dutch Shell PLC

- Mitsui Oil Exploration Co. Ltd.

- TotalEnergies SE

- Exxon Mobil Corporation

第七章 市场机会及未来趋势

第八章 新天然气田发现

简介目录

Product Code: 47226

The Thailand Oil And Gas Market size is estimated at 244.29 thousand barrels per day in 2025, and is expected to reach 274.11 thousand barrels per day by 2030, at a CAGR of 2.33% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the increasing natural gas pipeline capacity and the demand for petroleum products are expected to drive the Thailand oil and gas market during the forecast period.

- On the other hand, the country's new plans to transition towards renewable energy sources might hinder the Thailand oil and gas market.

- Nevertheless, discovering new oil and gas fields is expected to create several opportunities for the Thailand oil and gas market during the forecast period.

Thailand Oil and Gas Market Trends

Downstream Segment Expected to Witness Significant Growth

- The downstream sector corresponds to the final processes before the crude oil or gas can be dispensed to the final end customers or retail market. Major refineries for crude oil and natural gas processing plants are set up for the same; the process thus generates other major side products like gasoline, liquified natural gas, diesel, and other lubricants.

- In 2022, the export volume of petroleum products from Thailand amounted to almost 191.3 thousand barrels per day, a slight increase compared to the previous year. In the same year, Thailand exported diesel fuel the most compared to other petroleum products.

- The downstream refining sector of Thailand in the Southeast Asia region (in refining capacity and throughput) is one of the largest based on market cap, just after Singapore. The refinery throughput has grown in recent years due to rising domestic petroleum demand, rising petroleum prices, healthy growth in the tourism sector, and stable and high refinery margins.

- On the other hand, the refinery throughput has been increasing in recent years. The country currently has six refinery complexes, most of which are owned partially or fully by the country's national oil and gas conglomerate PTT. The country has been increasing its refining capacity to meet its growing domestic and regional demand.

- Thai Oil, the flagship refining company from Thailand, had already decided to expand its existing crude refining facility in Sriracha Oil Refinery in Laem Chabang by fueling approximately 4.8 billion dollars.

- In addition, the expansion will also see the addition of a residue hydrocracker, a vacuum gas oil hydrocracker, a hydrogen manufacturing unit, a diesel hydrodesulfurization unit, a naphtha hydrotreater, a sulfur recovery unit, and an electric power plant fueled by residue pitch.

- In August 2021, Hyundai Engineering received a USD 256 million EPC (engineering, procurement, and construction) order from IRPC PCL to upgrade its refinery with a total capacity of 215,000 barrels per day in Rayong, about 170 km southeast of Bangkok. According to Hyundai, the facility is expected to complete in early 2024 in line with the IRPC's plan.

- Thus, with all the above mentioned, Thailand's oil refining capacity is expected to grow slightly during the forecast period due to the expansion of refineries and increased demand for refined oil.

Energy Transition from Coal to Natural Gas Expected to Drive the Market

- To cope with the international clean fuel energy requirements and reduce its carbon footprints towards net zero, Thailand has already announced its transition from a coal-based economy to a gas-based economy.

- Well aware of its depleting natural gas reserves,, Thailand has already started to venture into Liquified Natural Gas (LNG) by developing its infrastructural requirements in its various seaports. The recently completed LNG terminal in Nong Fab, with a capacity of 7.5 million mt/year, has been the nation's example as it shifts towards natural gas.

- In 2022, natural gas consumption in Thailand amounted to around 50.7 billion cubic meters, slightly inclined compared to the previous year. Natural gas consumption in Thailand witnessed an increase of 10 percent in 2022.

- The country has a few under-construction and planned natural gas power plants, such as the Gulf Sriracha power plant (2.5 GW), Hin Kong Power Project (1.4 GW), Chonburi Ng Project power station (2.6 GW), and two other power plants in Surat Thani with 700 MW each. Commissioning of these power plants is expected to increase natural gas demand in Thailand.

- In February 2021, Thailand's state-controlled oil firm, PTT, announced that it s planned an investment of USD 28.3 billion across all its operations for 2021-2025. It focuses on developing the country's LNG and natural gas industry while seeking future energy opportunities.

- Therefore, owing to the above points, the increasing energy transition in the country is expected to drive the oil and gas market during the forecast period.

Thailand Oil and Gas Industry Overview

The Thailand oil and gas market is semi consolidated. Some of the major players in the market (in no particular order) are PTT Public Company Limited, Chevron Corporation, Exxon Mobil Corporation, TotalEnergies SE, and MedcoEnergi.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Crude Oil Production Forecast, till 2028

- 4.3 Natural Gas Production Forecast, till 2028

- 4.4 Refinery Installed Capacity and Forecast, till 2028

- 4.5 Recent Trends and Developments

- 4.6 Government Policies and Regulations

- 4.7 Market Dynamics

- 4.7.1 Drivers

- 4.7.1.1 Expanding the Asia's Largest Downstream Sector

- 4.7.1.2 Energy Transition from Coal to Natural Gas

- 4.7.2 Restraints

- 4.7.2.1 Government Policies to Shift Towards Cleaner Fuels

- 4.7.1 Drivers

- 4.8 Supply Chain Analysis

- 4.9 PESTLE Analysis

5 MARKET SEGMENTATION - BY SECTOR

- 5.1 Upstream

- 5.2 Midstream

- 5.3 Downstream

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 PTT Public Company Limited

- 6.3.2 Chevron Corporation

- 6.3.3 MedcoEnergi

- 6.3.4 Bangchak Corporation PCL

- 6.3.5 Pan Orient Energy (Siam) Ltd.

- 6.3.6 Sea Oil Energy Limited

- 6.3.7 Royal Dutch Shell PLC

- 6.3.8 Mitsui Oil Exploration Co. Ltd.

- 6.3.9 TotalEnergies SE

- 6.3.10 Exxon Mobil Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 Discovery of New Oil and Gas Fields

02-2729-4219

+886-2-2729-4219

石油和天然气市场规模、份额和成长分析(按产品类型、产业类型、部署类型、应用和地区划分)-2026-2033年产业预测

石油和天然气市场规模、份额和成长分析(按产品类型、产业类型、部署类型、应用和地区划分)-2026-2033年产业预测 美国石油和天然气:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)英国石油天然气:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南石油天然气:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

美国石油和天然气:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)英国石油天然气:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南石油天然气:市场占有率分析、产业趋势与统计、成长预测(2026-2031年) 2026年全球油气市场报告

2026年全球油气市场报告 石油和天然气营运维护服务市场(按维护类型、合约类型、资产类型、交付方式、能力、服务供应商和最终用户行业划分),全球预测,2026-2032年印尼油气:市场占有率分析、产业趋势与统计、成长预测(2026-2031)马来西亚油气:市场占有率分析、产业趋势、统计数据和成长预测(2026-2031)

石油和天然气营运维护服务市场(按维护类型、合约类型、资产类型、交付方式、能力、服务供应商和最终用户行业划分),全球预测,2026-2032年印尼油气:市场占有率分析、产业趋势与统计、成长预测(2026-2031)马来西亚油气:市场占有率分析、产业趋势、统计数据和成长预测(2026-2031) 2032年油气市场预测:按产品类型、价值链、来源、运输基础设施、应用、最终用户和地区分類的全球分析2025年全球石油天然气管道及相关结构建设市场报告

2032年油气市场预测:按产品类型、价值链、来源、运输基础设施、应用、最终用户和地区分類的全球分析2025年全球石油天然气管道及相关结构建设市场报告

▼