|

市场调查报告书

商品编码

1683929

欧洲汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Europe Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

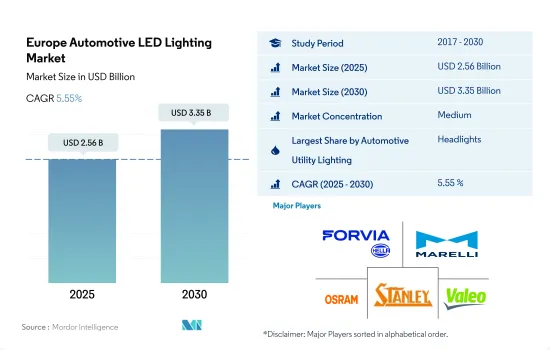

预计2025年欧洲汽车LED照明市场规模为25.6亿美元,到2030年将达到33.5亿美元,预测期间(2025-2030年)的复合年增长率为5.55%。

製造商预计将获得 LED 外部照明的批准,汽车製造商预计将在道路安全、技术数位化方面进行投资,以增加 LED 照明的使用。

- 就金额份额而言,头灯将在 2023 年占据大部分份额,其次是其他灯光和转向信号灯。车头灯减少了日常的死亡和事故。随着该国从疫情中復苏,去年道路交通事故死亡人数约为 20,600 人,比 2021 年增加了 3%。不过,与疫情爆发前的 2019 年相比,道路交通死亡人数减少了 2,000 人(下降了 10%)。欧盟和联合国已设定目标,在2030年前减少道路交通事故死亡人数,因此预计汽车将配备LED大灯,以减少现有的道路交通事故死亡人数。

- 从销售份额来看,2023年转向信号灯将占据最大份额,其次是头灯和其他灯光。预计这些灯的市场占有率将保持稳定,波动不大。大众、戴姆勒、博世、采埃孚等汽车製造商以及其他欧洲国家供应商将在未来几年在数位化、电动车和驾驶、氢技术和道路安全方面投入 1,619 亿美元。这将增加信号灯的使用,从而增加该国的 LED 灯的使用。

- 市场各大汽车製造商均致力于扩大电动车市场。为此,欧洲议会和理事会于 2009 年 4 月 23 日通过了第 443/2009 号理事会条例 (EC),制定了新型乘用车排放气体标准,作为减少轻型商用车二氧化碳排放的欧共体综合方针的一部分。两家製造商联合申请批准高效能 LED 外部照明,作为无需外部充电的内燃机汽车和混合动力汽车的创新技术。这扩大了国产LED照明的市场占有率。

预计减少汽车二氧化碳排放的法规不断加强以及磁力马达的发展将增加电动车的需求,从而推动市场成长。

- 在这一领域,预计到 2023 年其他欧洲国家将占据 30% 以上的市场占有率,其次是德国(占 20% 以上)和西班牙(占 15% 以上的市场占有率)。这是由于商用车、两轮车和乘用车数量的增加。预计电动车的日益普及也将与欧洲其他地区的市场成长相匹配。

- 2021年,波兰的非常老旧的乘用车比例最高,41.3%的乘用车车龄超过20年。 2023年新兴国家乘用车的积极发展也反映在国家层面。成长最强劲的是西班牙(+51.4%)和义大利(+19.0%),其次是法国(+8.8%),成长速度较慢但较为稳定。混合动力电动车 (HEV) 在 2021 年也取得了强劲开局。销量成长 22.1% 至 197,982 辆。推动这一成长的主要因素是该地区四大市场的两位数成长:西班牙(成长 59.3%)、义大利(成长 24.7%)、德国(成长 19.0%)和法国(成长 12.5%)。结果,市场占有率为 26.0%,比 2022 年 1 月提高了 2.3 个百分点。

- 旨在减少汽车二氧化碳排放的政府法规可能会进一步鼓励欧洲汽车製造商采用 LED 光源。汽车製造商也推出了许多新计划来为永续性做出贡献。例如,一项新的欧洲研发计画将于 2023 年启动,旨在开发用于电动车 (EV) 的更便宜、更有效率、更高功率的永磁电动马达。蒙德拉贡大学领导着一个由八个欧洲合作伙伴组成的联盟,其中包括 GKN Automotive。

欧洲汽车 LED 照明市场趋势

电动车销售成长可望推动欧洲 LED 市场

- 预计2022年韩国汽车总产量将达1,767万辆,2023年将达1,833万辆。中国首批工厂关闭,扰乱了欧洲汽车产业的供应链。欧盟成员国汽车工厂平均停工时间为30天,其中瑞典停工时间最短(15天),义大利停工时间最长(41天)。 2020年上半年,欧盟汽车产业产量减少360万辆,损失累计1,000亿欧元(1,079亿美元)。截至2020年9月底,这一数字上升至4,024,036辆,占欧盟2020年产量的22.3%。欧洲产量下降最终对汽车领域的LED照明产生了负面影响。

- 大众集团、Stellantis、梅赛德斯-奔驰、宝马、保时捷、Hurtan、GTA Motors、奥迪和标緻是该地区的主要汽车製造商。电动车的兴起和车辆燃料类型的技术进步正在改变该地区的汽车产业。目前,欧盟的电池式电动车销量正在快速成长。例如,2022 年欧盟市场上销售的 910 万辆汽车中,12.1% 将是纯电动车,而 2019 年这一比例仅为 1.9%,2021 年为 9.1%。约 22.6% 的销量为混合动力电动车,9.4% 为更新、更环保的插电混合动力汽车。随着电动车越来越普及,车载照明用半导体和LED因其高效率而需求旺盛。

电动车註册数量的增加和政府推广电动车的政策可能会推动 LED 市场的成长

- 整个欧洲范围内电动车的普及正在迅速增长。欧洲电动车 (BEV、PHEV、EREV 和 FCEV) 销量为 259 万辆,较 2021 年成长 15%,较 2020 年成长 92%。 2022 年欧洲电动车销售份额最高的国家将是挪威 (79%)、瑞典 (33%)、荷兰 (23%) 和丹麦 (21%),其次是芬兰、瑞士和德国,各占 18%。就 2022 年的市场占有率而言,电池式电动车(BEV) 将占总市场份额的 12.1%,高于 2021 年的 9.1% 和 2019 年的 1.9%。

- 2016 年,英国道路上有 30,669 辆纯电动车,到 2023 年 5 月将上升到 784,968 辆。 2022 年註册的纯电动车超过 265,000 辆,比 2021 年增加 40%。英国政府大力支持人们选择电动车,以增加在英国註册的电动车数量。购买者可以享受插电式补贴,购买新型电动车可享受高达 2,500 欧元(2,699 美元)的折扣。在苏格兰,我们也为购买新旧电动车提供无息贷款。

- 作为重组汽车产业战略的一部分,法国曾计划在2020年5月增加补贴。主要原因是新冠疫情导致销售下降。当时,最高补贴额从6,479美元提高到7,558.8美元。 2021年年中,限额从7,558.8美元降至6,478.9美元。 2023 年,政府将从 2023 年 1 月起将电动车补助从 6,478.9 美元减少到 5,399 美元。该公司还设定了到 2030 年每年生产 200 万辆电动车的目标。由于这些市场的进步,该地区对汽车 LED 的需求预计在未来几年将增加。

欧洲汽车LED照明产业概况

欧洲汽车LED照明市场格局适度整合,前五大厂商占比达48.57%。该市场的主要企业是:HELLA GmbH & Co. KGaA、Marelli Holdings、OSRAM GmbH.、Stanley Electric 和 Valeo(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 汽车产量

- 人口

- 人均收入

- 汽车贷款利率

- 充电站数量

- 汽车持有量

- LED进口总量

- 家庭数量

- 道路网络

- 渗透率

- 法律规范

- 法国

- 德国

- 西班牙

- 英国

- 价值链与通路分析

第五章 市场区隔

- 汽车实用照明

- 日间行车灯 (DRL)

- 转向指示灯

- 头灯

- 倒车灯

- 红绿灯

- 尾灯

- 其他的

- 汽车照明

- 二轮车

- 商用车

- 搭乘用车

- 国家名称

- 法国

- 德国

- 西班牙

- 英国

- 其他欧洲国家

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- HELLA GmbH & Co. KGaA

- HYUNDAI MOBIS

- KOITO MANUFACTURING CO., LTD.

- Marelli Holdings Co., Ltd.

- OSRAM GmbH.

- Phoenix Lamps Ltd(Suprajit Engineering Ltd)

- Signify(Philips)

- Stanley Electric Co., Ltd.

- Valeo

- ZKW Group

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001627

The Europe Automotive LED Lighting Market size is estimated at 2.56 billion USD in 2025, and is expected to reach 3.35 billion USD by 2030, growing at a CAGR of 5.55% during the forecast period (2025-2030).

Manufacturers are expected to get approval for exterior vehicle lighting with LED and automakers are expected to invest in road safety, technology, and digitization to increase the use of LED lights

- In terms of value share, in 2023, headlights accounted for the majority, followed by other lights and directional signal lights. Headlights have reduced daily fatalities and accidents. About 20,600 people died in road crashes the previous year, up by 3% from 2021 as traffic recovered from the pandemic. However, this represented 2,000 fewer road fatalities (10% less) compared to the pre-pandemic year of 2019. The goal of reducing road fatalities by 2030 was set by the EU and UN. Hence, it is expected that vehicles will be fitted with LED headlights to reduce the existing rate of road fatalities.

- In terms of volume share, in 2023, directional signal lights accounted for the majority, followed by headlights and other lights. The market share of these lights is expected to remain the same with little fluctuation. Automakers such as Volkswagen, Daimler, Bosch, ZF, and other top European suppliers will spend (USD 161.9 billion) over the next few years on digitalization, electromobility and driving, hydrogen technology, and road safety. This will increase the use of signal lights, thus increasing the use of LED lights in the country.

- The major automakers in the market are focusing on expanding the electric vehicle market. To this end, the European Parliament and Council of 23 April 2009 set emissions standards for new passenger cars as part of the community's integrated approach to reducing CO2 emissions from light commercial vehicles under Council Regulation (EC) No. 443/2009. Manufacturers jointly applied for the approval of efficient exterior vehicle lighting with LED as an innovative technology for vehicles with internal combustion engines and hybrid electric vehicles that do not require external charging. This factor increased the market share of domestic LED lighting.

Increasing regulations to reduce vehicle CO2 emissions and the development of magnetic electric motors to boost EV demand are expected to boost the market's growth

- In this segment, the Rest of Europe is expected to occupy a market share of more than 30% in 2023, followed by Germany and Spain, with market shares of more than 20% and 15%, respectively. This is due to an increase in the number of commercial vehicles, two-wheelers, and passenger cars. An increase in electric vehicle adoption is also anticipated to correspond to the market's growth in other parts of Europe.

- In 2021, Poland had the highest proportion of very old passenger cars, with 41.3% of passenger cars being over 20 years old. The positive development of passenger cars in the region in 2023 was reflected at the country level. The strongest growth was recorded in Spain (+51.4%) and Italy (+19.0%), followed by France (+8.8%), which had slow but steady growth. Hybrid electric vehicles (HEVs) also got off to a strong start in 2021. Sales increased by 22.1% to 197,982 units. This was driven by double-digit growth in the region's four largest markets: Spain (+59.3%), Italy (+24.7%), Germany (+19.0%), and France (+12.5%). This resulted in a market share of 26.0%, an improvement of 2.3 points compared to January 2022.

- Government regulations aimed at reducing vehicle CO2 emissions will further encourage the adoption of LED light sources by European automakers. Automakers are also launching a number of new programs to contribute to sustainability. For example, a new European R&D program to develop cheaper, more efficient, and power-dense permanent magnet electric motors for electric vehicles (EVs) was expected to start in 2023. Mondragon University leads the consortium of eight European partners and includes GKN Automotive.

Europe Automotive LED Lighting Market Trends

Increasing EV sales are expected to drive the LED market in Europe

- The total automobile vehicle production in South Korea was 17.67 million units in 2022, and it is expected to reach 18.33 million units in 2023. The first Chinese factory closures disrupted the supply chains of the European automotive sectors. The average downtime for automotive plants throughout EU Member States was 30 days, with Sweden experiencing the most minor downtime (15 days) and Italy experiencing the highest (41 days). The EU automobile sector lost 3.6 million vehicles from production in the first half of 2020, amounting to a loss of EUR 100 billion (USD 107.9 billion). This number climbed to 4,024,036 motor vehicles by the end of September 2020, accounting for 22.3% of the EU's 2020 production. Such production loss in Europe ultimately had a negative impact on LED lights in the automotive sector.

- Volkswagen Group, Stellantis, Mercedes-Benz, BMW, Porsche, Hurtan, GTA Motors, Audi, and Peugeot are the major automotive car manufacturers in the region. With the rise in EVs and technological advancements in the fuel types utilized in vehicles, the region is seeing a significant transformation in its automotive industry. Battery electric vehicle sales in the EU are still rising quickly. For instance, 12.1% of the 9.1 million vehicles sold in EU markets in 2022 were fully battery electric vehicles, as compared to a share of just 1.9% in 2019 and 9.1% in 2021. About 22.6% of sales were made up of hybrid electric cars, and 9.4% of sales were made up of the more recent and eco-friendly plug-in hybrids. With the growing usage of EVs, the demand for semiconductors and LEDs in vehicle lighting is high due to their efficiency.

Increasing EV registrations and government policies for EV adoption may drive the growth of the LED market

- The adoption of EVs across Europe is growing rapidly. In Europe, sales of electric vehicles (BEVs, PHEVs, EREVs, and FCEVs) totaled 2.59 million units, up by 15% from 2021 and by 92% from 2020. Norway (79%), Sweden (33%), the Netherlands (23%), and Denmark (21%) had the highest market shares of EV sales in Europe in 2022, followed by Finland, Switzerland, and Germany, with an 18% share of EV registrations each in Europe in 2022. In 2022, battery electric vehicles (BEVs) accounted for 12.1% of the total market share, up from 9.1% in 2021 and 1.9% in 2019.

- In 2016, the number of battery-electric cars in the United Kingdom was 30,669, and by May 2023, this number reached 784,968. More than 265,000 battery-electric vehicles were registered in 2022, a 40% increase over 2021. The British government strongly supports the people who are choosing EVs to increase the number of registered electric vehicles in the United Kingdom. Buyers can benefit from the Plug-In Grant, which offers a discount of up to EUR 2,500 (USD 2,699) on new EVs. Scotland also offers interest-free loans on purchases of new and used EVs.

- As part of a restructuring strategy for the automotive industry, France planned to raise subsidy rates in May 2020. The main reason was a drop in sales caused by the COVID-19 pandemic. The maximum subsidy rate was increased from USD 6,479 to USD 7,558.8 at the time. In mid-2021, the maximum rate was reduced from USD 7,558.8 to USD 6,478.9. In 2023, the government reduced subsidies for electric cars to USD 5,399 from USD 6,478.9, effective from January 2023. It also set a target of producing two million electric vehicles per year by 2030. These advancements in the market are expected to drive the demand for automotive LEDs in the region in the coming years.

Europe Automotive LED Lighting Industry Overview

The Europe Automotive LED Lighting Market is moderately consolidated, with the top five companies occupying 48.57%. The major players in this market are HELLA GmbH & Co. KGaA, Marelli Holdings Co., Ltd., OSRAM GmbH., Stanley Electric Co., Ltd. and Valeo (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 France

- 4.11.2 Germany

- 4.11.3 Spain

- 4.11.4 United Kingdom

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Spain

- 5.3.4 United Kingdom

- 5.3.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 HELLA GmbH & Co. KGaA

- 6.4.2 HYUNDAI MOBIS

- 6.4.3 KOITO MANUFACTURING CO., LTD.

- 6.4.4 Marelli Holdings Co., Ltd.

- 6.4.5 OSRAM GmbH.

- 6.4.6 Phoenix Lamps Ltd (Suprajit Engineering Ltd)

- 6.4.7 Signify (Philips)

- 6.4.8 Stanley Electric Co., Ltd.

- 6.4.9 Valeo

- 6.4.10 ZKW Group

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

全球汽车LED市场(2025年)- 照明与显示产品趋势

全球汽车LED市场(2025年)- 照明与显示产品趋势 全球汽车LED尾灯市场:未来预测(2025-2030)

全球汽车LED尾灯市场:未来预测(2025-2030) 汽车用LED照明的全球市场:车辆类别,各销售管道,各应用类型,各地区,机会,预测,2018年~2032年

汽车用LED照明的全球市场:车辆类别,各销售管道,各应用类型,各地区,机会,预测,2018年~2032年 中东和非洲汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)中国汽车 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)亚太地区汽车 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)北美汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)南美汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)印度汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)德国汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

中东和非洲汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)中国汽车 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)亚太地区汽车 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)北美汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)南美汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)印度汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)德国汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

▼