|

市场调查报告书

商品编码

1684008

越南杀菌剂市场:份额分析、产业趋势与统计、成长预测(2025-2030)Vietnam Fungicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

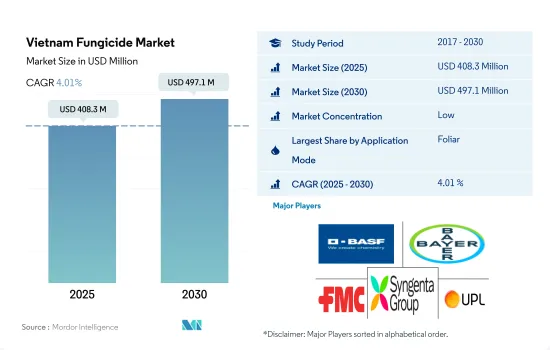

越南杀菌剂市场规模预计在 2025 年为 4.083 亿美元,预计到 2030 年将达到 4.971 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.01%。

害虫压力的增加推动了对各种施用方法的杀虫剂的需求

- 越南杀菌剂市场依用途分为化学施用、叶面喷布、熏蒸和土壤处理等多种类型。这些不同的施用方法是全国各地不同农业条件下有效施用杀菌剂的重要工具。

- 叶面喷布占据市场主导地位 预计该领域杀菌剂的市场价值在预测期内(2023-2029 年)的复合年增长率将达到 4.3%。这是因为它广泛应用于各种作物,包括谷物、谷类、水果和蔬菜,其中叶子是病害发展的主要部位。

- 越南普遍使用土壤处理方法来防治对植物健康和生产力构成重大威胁的土壤真菌。由于越来越多地采用种子处理作为避免作物损失的预防措施,预计市场将以 4.0% 的复合年增长率增长。

- 在越南,化学灌溉方法也广泛用于需要持续、可控施用的作物,例如水果和蔬菜。随着越来越多的农民采用这种方法作为向作物施用杀菌剂的有效手段,该行业预计将增长,在预测期内(2023-2029 年)的复合年增长率为 3.8%。

- 熏蒸在越南的农业实践中尤其重要,因为它有助于维持土壤健康并防止病原体传播到脆弱的作物。杀菌剂配方的改进以及熏蒸技术和设备的进步预计将促进市场的成长。新技术和改进的熏蒸方法使杀菌剂更加有效。

越南杀菌剂市场趋势

气候变迁和日益增加的疾病压力可能会推动杀菌剂的消费

- 2019 年至 2022 年间,越南的杀菌剂使用量显着增加了 31.2 克/公顷。这可以归因于多种因素,这些因素导致农业实践和植物保护对杀菌剂的需求不断增长。

- 2022年越南农业面积与前一年同期比较增加1.7%公顷。农业生产的扩大和提高作物产量和品质的愿望预计将导致杀菌剂的使用增加。越南农民正在努力满足日益增长的粮食需求并提高作物产量。

- 气候条件和环境因素的变化也预计将推动越南杀菌剂的消费。温度和湿度的变化会为真菌疾病的发生和传播创造有利条件。因此,预计农民将更多地依赖杀菌剂来降低与这些疾病相关的风险并保护他们的作物。

- 随着对疾病管理和作物保护重要性的认识和了解不断提高,越南农民开始采用杀菌剂。对疾病预防和管理态度的转变正在刺激该国对杀菌剂的需求。

- 此外,杀菌剂配方的进步和各种有效、有针对性的杀菌剂产品的出现也促进了杀菌剂使用量的增加。创新杀菌剂的开发提高了其功效和安全性,为农民控制疾病提供了更多的选择。这进一步鼓励采用杀菌剂作为综合虫害管理策略的一部分。

真菌疾病的增加以及该国对进口活性成分的依赖可能会推高活性成分的价格。

- 越南的农业气候区域范围广泛。例如,在中部和北部地区,冬季气候凉爽至寒冷,有利于温带病原体的生长。低温会阻碍一些作物的生长,并使幼苗更容易受到其他疾病的侵害。此外,每年的气候週期都包括非常潮湿和干燥的时期。这种天气会对作物造成压力,尤其容易引发由病原体引起的根部和茎部疾病。Tebuconazole、Azoxystrobin和Metalaxyl是越南常用的杀菌剂有效成分。

- Tebuconazole是一种系统性杀菌剂,2022 年的价格为每吨 8,700 美元。Tebuconazole以治疗銹病、纹枯病、叶斑病和炭疽病而闻名。越南大部分Tebuconazole从中国、德国和印度进口。

- Azoxystrobin是一种广谱杀菌剂,对属于卵菌纲、子囊菌纲、子囊菌纲和担子菌纲的真菌均有效。由于镰刀菌和木霉菌等真菌的侵染增加,Azoxystrobin的价格已从 2017 年的每吨 4,000 美元上涨至 2022 年的每吨 4,600 美元。同样,用于防治真菌引起的植物病害的系统性杀菌剂Metalaxyl在 2022 年的价格为每公吨 4,400 美元。

- 在越南,真菌疾病的增加以及对这些活性成分进口的依赖可能会推高这些活性成分的价格。

越南杀菌剂产业概况

越南杀菌剂市场较为分散,前五大企业市占率合计为29.06%。该市场的主要企业有:BASF公司、拜耳公司、FMC公司、先正达集团和UPL有限公司(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 每公顷农药消费量

- 活性成分价格分析

- 法律规范

- 越南

- 价值炼和通路分析

第五章市场区隔

- 执行模式

- 化学喷涂

- 叶面喷布

- 熏蒸

- 种子处理

- 土壤处理

- 作物类型

- 经济作物

- 水果和蔬菜

- 粮食

- 豆类和油籽

- 草坪和观赏植物

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 业务状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001710

The Vietnam Fungicide Market size is estimated at 408.3 million USD in 2025, and is expected to reach 497.1 million USD by 2030, growing at a CAGR of 4.01% during the forecast period (2025-2030).

The rising pest pressure is driving the demand for insecticides in various application methods

- The fungicide market in Vietnam is categorized by various applications, including chemigation, foliar application, fumigation, and soil treatment. These different application methods serve as important means of effectively applying fungicides in diverse agricultural contexts within the country.

- Foliar application dominates the market. Fungicide's market value in this segment is expected to register a CAGR of 4.3% during the forecast period (2023-2029) because it is widely applied in various crops, including grains, cereals, fruits, and vegetables, where the foliage is the primary site of disease occurrence.

- Soil treatment is commonly used in Vietnam to protect from soil-borne fungi that pose a significant threat to the plant's health and productivity. The market is expected to register a CAGR of 4.0% due to the rising adoption of seed treatment chemicals as a preventive measure to avoid crop losses.

- The chemigation method is also commonly used in Vietnam for crops that require a consistent and controlled application, such as fruits and vegetables. The segment is expected to grow, registering a CAGR of 3.8% during the forecast period (2023-2029) because more farmers are adopting this practice as a means to efficiently deliver fungicides to their crops.

- Fumigation is particularly important in Vietnam's agricultural practices, as it helps maintain soil health and prevent the spread of pathogens to vulnerable crops. Advancements in fumigation technologies and equipment, along with improved formulations of fungicides, are expected to contribute to the growth of the market as new technologies and improved fumigation application methods are enhancing the efficiency of fungicides.

Vietnam Fungicide Market Trends

The changing climate and rising disease pressure are expected to drive the consumption of fungicides

- The usage of fungicides in Vietnam experienced a notable increase of 31.2 grams per hectare between 2019 and 2022. This can be attributed to several factors that have contributed to the growing demand for fungicides in agricultural practices and plant protection.

- Vietnam's agricultural acreage increased by 1.7% ha in 2022 from the previous year. The expansion of agricultural production and the desire to enhance crop yields and quality are expected to increase the usage of fungicides. Farmers in Vietnam are striving to meet the growing demand for food and improve the productivity of their crops.

- Changing climatic conditions and environmental factors are also expected to drive the consumption of fungicides in Vietnam. Shifts in temperature and humidity levels can create favorable conditions for the development and spread of fungal diseases. As a result, farmers are expected to increasingly rely on fungicides to mitigate the risks associated with these diseases and safeguard their crops.

- The increasing awareness and knowledge about the importance of disease management and crop protection have driven the adoption of fungicides among farmers in Vietnam. The shift in mindset toward disease prevention and management has fueled the demand for fungicides in the country.

- Additionally, advancements in fungicide formulations and the availability of a wide range of effective and targeted fungicide products have also contributed to increased usage. The development of innovative fungicides with improved efficacy and safety profiles has provided farmers with more options for disease control. This has further encouraged the adoption of fungicides as part of their integrated pest management strategies.

Increase in the fungal diseases, coupled with the dependence on imports for these active ingredients in the country, may drive the prices of these active ingredients

- Vietnam has a wide range of agroclimatic regions. For example, the central and northern provinces experience a cool to cold winter that favors temperate pathogens. The low temperatures inhibit the growth of some crops, making them more susceptible to seedlings and other diseases. Additionally, the yearly weather cycle includes very wet and dry periods. Such weather can also lead to crop stress and favor some diseases, especially of the roots and stems caused by pathogens. Tebuconazole, azoxystrobin, and metalaxyl are commonly used fungicide-active ingredients in Vietnam.

- Tebuconazole uses a systematic fungicide valued at USD 8.7 thousand per metric ton in 2022. Tebuconazole is known to treat rust fungus, sheath blight, leaf spot, and anthracnose. Vietnam imports most of its tebuconazole from China, Germany, and India.

- Azoxystrobin is a broad-spectrum fungicide active against fungal pathogens belonging to oomycetes, ascomycetes, deuteromycetes, and basidiomycetes. Owing to the increase in infestation of fungi like Fusarium and Trichoderma, the price of azoxystrobin increased from USD 4.0 thousand per metric ton in 2017 to USD 4.6 thousand per metric ton by 2022. Similarly, metalaxyl is a systemic fungicide used to control plant diseases caused by Oomycete fungi, valued at USD 4.4 thousand per metric ton in 2022.

- An increase in fungal diseases, coupled with dependence on imports for these active ingredients, in the country may drive the prices of these active ingredients.

Vietnam Fungicide Industry Overview

The Vietnam Fungicide Market is fragmented, with the top five companies occupying 29.06%. The major players in this market are BASF SE, Bayer AG, FMC Corporation, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 Syngenta Group

- 6.4.8 UPL Limited

- 6.4.9 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

2025年杀菌剂全球市场报告

2025年杀菌剂全球市场报告 种子处理杀菌剂市场报告:趋势、预测与竞争分析(至2031年)

种子处理杀菌剂市场报告:趋势、预测与竞争分析(至2031年) 中国杀菌剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)亚太杀菌剂:市场占有率分析、产业趋势与成长预测(2025-2030)北美杀菌剂:市场占有率分析、产业趋势与成长预测(2025-2030)南美杀菌剂:市场占有率分析、行业趋势、统计数据和成长预测(2025-2030 年)印尼杀菌剂:市场占有率分析、产业趋势与成长预测(2025-2030)印度杀菌剂:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)杀菌剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)欧洲杀菌剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

中国杀菌剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)亚太杀菌剂:市场占有率分析、产业趋势与成长预测(2025-2030)北美杀菌剂:市场占有率分析、产业趋势与成长预测(2025-2030)南美杀菌剂:市场占有率分析、行业趋势、统计数据和成长预测(2025-2030 年)印尼杀菌剂:市场占有率分析、产业趋势与成长预测(2025-2030)印度杀菌剂:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)杀菌剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)欧洲杀菌剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

▼