|

市场调查报告书

商品编码

1686174

欧洲工程塑胶:市场占有率分析、行业趋势和统计、成长预测(2024-2029 年)Europe Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

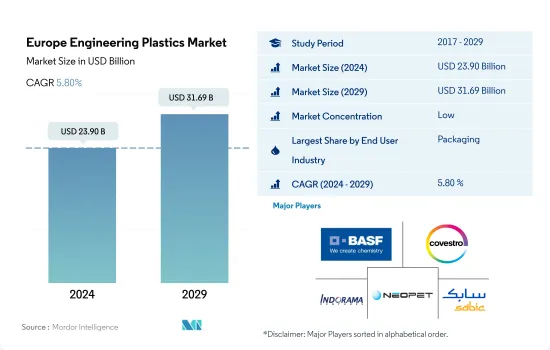

预计 2024 年欧洲工程塑胶市场规模将达到 239 亿美元,到 2029 年预计将达到 316.9 亿美元,预测期内(2024-2029 年)的复合年增长率为 5.80%。

预测期内包装将占据市场主导地位

- 工程塑胶的用途无穷,而且往往比通用塑胶或一般塑胶具有更好的机械性能和热性能。受包装、电气和电子产业需求成长的推动,欧洲工程塑胶消费量在2017年至2019年间成长了5.1%。

- 由于大量生产用于包装饮料、饮用水、个人护理、家用产品等的塑胶瓶,包装行业消耗了该地区大部分的工程塑胶。由于全球供应链中断,2020年疫情期间所有产业的消费量总合去年同期与前一年同期比较了6.2%。但预计2021年市场将復苏,2022年成长4.6%,延续稳定成长。

- 由于欧洲生产的汽车数量庞大,汽车产业是继包装产业之后工程塑胶的第二大消费产业。 2020年,受疫情封锁、出行限制及汽车工厂关闭等影响,汽车产量大幅下降,导致汽车领域消费量与前一年同期比较下降22.69%。

- 预计欧洲航太领域的支出将出现最快的成长,预测期内(2023-2029 年)的复合年增长率为 7.78%。这是因为生产飞机零件是为了满足对更轻、更省油的飞机日益增长的需求。

未来几年德国将主导市场

- 在欧洲,工程塑胶作为聚合物在各种终端使用者产业中发挥重要作用,包括包装、电气和电子、汽车、航太、工业和机械。

- 由于包装、建筑、电气电子和汽车行业的不断发展,德国是该地区最大的工程塑胶消费国。 2022年,德国包装产业的销售额占整个欧洲的18.7%。德国塑胶包装产量预计将从 2021 年的 437 万吨增加到 2022 年的 446 万吨。

- 义大利是该地区第二大工程塑胶消费国。受建设业和电气行业快速发展的推动,该国在 2022 年占欧洲树脂市场总销售额的 12%。 2022 年,义大利新建占地面积将达到 1.885 亿平方英尺,高于 2021 年的 1.672 亿平方英尺。预计未来几年,建筑业的不断发展将推动义大利对工程塑胶的需求。

- 英国是欧洲工程塑胶市场成长最快的国家,预计预测期内(2023-2029 年)的以金额为准年增长率为 6.70%。英国航太工业是世界第二大工业。 2021年,英国民用航太业的营业额约为320亿美元。英国政府计划在 2027 年将研发支出增加到 GDP 的 2.4%。预计预测期内航太工业的产量和投资增加将推动该国对工程塑胶的需求。

欧洲工程塑胶市场趋势

科技创新助力家电市场

- 2017 年至 2021 年,欧洲电气和电子设备产量的复合年增长率超过 3.8%。电子创新的快速发展推动着对更新、更快的电气和电子产品的持续需求。因此,该地区对电气和电子设备生产的需求也在增加。

- 儘管远距工作和学习导致对电脑和笔记型电脑的需求增加,但欧洲消费性电子产品领域的每位用户平均收入仍下降了 6.3%。 2020年销售额约2,521亿美元。结果导致该地区2020年电气及电子设备产量较去年与前一年同期比较2.8%。

- 2021年,欧洲电气和电子设备出口额约2,283.7亿美元,比2020年成长12.4%。因此,该地区电气和电子设备产量有所增长,2021与前一年同期比较增长11.6%。

- 预测期内,机器人、虚拟和扩增实境实境、物联网 (IoT) 和 5G 连线预计将实现成长。由于技术进步,预测期内对家用电子电器的需求预计会增加。该地区的消费电子产品销售额预计将从 2023 年的 1,211 亿美元增长到 2027 年的约 1,572 亿美元。到 2027 年,欧洲预计将成为第二大电气和电子设备生产国,占全球市场的 12.7% 左右。因此,预计未来几年家用电子电器的兴起将推动对电气和电子设备生产的需求。

欧洲工程塑胶行业概况

欧洲工程塑胶市场较为分散,前五大公司占比为37.52%。市场的主要企业是: BASF SE、Covestro AG、Indorama Ventures Public Company Limited、NEO GROUP 和 SABIC(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 最终用户趋势

- 航太

- 车

- 建筑和施工

- 电气和电子

- 包装

- 进出口趋势

- 氟树脂交易

- 聚酰胺(PA)贸易

- 聚碳酸酯(PC)贸易

- 聚对苯二甲酸乙二酯(PET)贸易

- 聚甲基丙烯酸甲酯(PMMA)贸易

- 聚甲醛(POM)贸易

- 苯乙烯共聚物(ABS 和 SAN)贸易

- 价格趋势

- 回收概述

- 聚酰胺 (PA) 回收趋势

- 聚碳酸酯 (PC) 回收趋势

- 聚对苯二甲酸乙二醇酯 (PET) 的回收趋势

- 苯乙烯共聚物(ABS、SAN)的回收趋势

- 法律规范

- EU

- 法国

- 德国

- 义大利

- 俄罗斯

- 英国

- 价值链与通路分析

第五章 市场区隔

- 最终用户产业

- 航太

- 车

- 建筑和施工

- 电气和电子

- 工业/机械

- 包装

- 其他最终用户产业

- 树脂类型

- 氟树脂

- 依亚型

- 乙烯-四氟乙烯(ETFE)

- 氟化乙丙烯 (FEP)

- 聚四氟乙烯(PTFE)

- 聚氟乙烯 (PVF)

- 聚二氟亚乙烯(PVDF)

- 其他子树脂类型

- 液晶聚合物(LCP)

- 聚酰胺(PA)

- 副树脂类型

- 芳香聚酰胺

- 聚酰胺(PA)6

- 聚酰胺(PA)66

- 聚邻苯二甲酰胺

- 聚丁烯对苯二甲酸酯(PBT)

- 聚碳酸酯(PC)

- 聚醚醚酮 (PEEK)

- 聚对苯二甲酸乙二醇酯(PET)

- 聚酰亚胺(PI)

- 聚甲基丙烯酸甲酯 (PMMA)

- 聚甲醛(POM)

- 苯乙烯共聚物(ABS 和 SAN)

- 氟树脂

- 国家

- 法国

- 德国

- 义大利

- 俄罗斯

- 英国

- 其他欧洲国家

第六章 竞争格局

- 主要策略趋势

- 市场占有率分析

- 业务状况

- 公司简介.

- Arkema

- BASF SE

- Celanese Corporation

- Covestro AG

- DSM

- DuPont

- Indorama Ventures Public Company Limited

- INEOS

- LANXESS

- Mitsubishi Chemical Corporation

- NEO GROUP

- SABIC

- Solvay

- Trinseo

- Victrex

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50097

The Europe Engineering Plastics Market size is estimated at 23.90 billion USD in 2024, and is expected to reach 31.69 billion USD by 2029, growing at a CAGR of 5.80% during the forecast period (2024-2029).

Packaging to dominate the market during the forecast period

- Engineering plastics have endless applications today and tend to have better mechanical and thermal properties than common or commodity plastics. The European engineering plastics consumption volume witnessed a growth of 5.1% from 2017 to 2019 due to increasing demand from the packaging and electrical and electronics segments.

- The packaging segment consumes most of the engineering plastics in the region due to the large-scale production of plastic bottles used in packaging beverages, drinking water, personal care, household care, etc. Due to disruptions in the global supply chain, all industries' combined consumption volume fell by 6.2% in the pandemic year 2020 compared to the previous year. However, the market recovered in 2021 and continued to grow steadily, increasing by 4.6% in 2022.

- Because of the large number of vehicles produced in Europe, the automotive segment is the second largest consumer of engineering plastics after the packaging segment. Vehicle production dropped significantly in 2020 due to lockdowns, travel restrictions, and the closure of automotive factories, resulting in a 22.69% decrease in consumption volume from the previous year in the automotive segment.

- The European aerospace segment is expected to be the fastest growing in terms of consumption value during the forecast period (2023-2029) with a CAGR of 7.78%, owing to the production of aircraft components in response to the increasing demand for lighter and more fuel-efficient aircraft.

Germany to dominate the market over the coming years

- Engineering plastics play the role of an important polymer in Europe for various end-user industries, including packaging, electrical and electronics, automotive, aerospace, and industrial and machinery.

- Germany is the largest consumer of engineering plastics in the region owing to its growing packaging, construction, electrical and electronics, and automotive industries. In 2022, the German packaging industry held a share of 18.7% by revenue compared to the entire Europe. In Germany, plastic packaging production reached 4.46 million tons in 2022 from 4.37 million tons in 2021.

- Italy is the second-largest consumer of engineering plastics in the region. The country held a share of 12% by revenue of the overall resin market in Europe in 2022 due to its rapidly growing construction and electrical industries. The new floor area in the country reached 188.5 million sq. ft in 2022 from 167.2 million sq. ft in 2021. The rising construction industry is projected to drive the demand for engineering plastic in Italy in the future.

- The United Kingdom is the fastest-growing country in the European engineering plastics market, which is expected to register a CAGR of 6.70% in terms of value during the forecast period (2023-2029). The aerospace industry in the United Kingdom is the second-largest in the world. In 2021, the UK civil aerospace turnover totaled approximately USD 32 billion. The government of the United Kingdom is planning to increase its R&D spending to 2.4% of GDP by 2027. The increasing production and investment in the aerospace industry are projected to drive the demand for engineering plastics in the country during the forecast period.

Europe Engineering Plastics Market Trends

Technological innovations to boost the consumer electronics market

- Europe's electrical and electronics production registered a CAGR of over 3.8% between 2017 and 2021. The rapid pace of electronic technological innovation is driving consistent demand for newer and faster electrical and electronic products. As a result, it has also increased the demand for electrical and electronics production in the region.

- Despite the increased demand for computers and laptops due to remote working and distance learning, the average revenue per user in the European consumer electronics segment dropped by 6.3%. It generated a revenue of around USD 252.1 billion in 2020. As a result, in 2020, the electrical and electronic production in the region decreased by 2.8% by revenue compared to the previous year.

- In 2021, Europe's electrical and electronic equipment exports were around USD 228.37 billion, 12.4% higher compared to 2020. As a result, electrical and electronic production in the region increased and registered 11.6% in 2021 compared to the previous year.

- Robotics, virtual reality and augmented reality, IoT (Internet of Things), and 5G connectivity are expected to grow during the forecast period. As a result of technological advancements, demand for consumer electronics is expected to rise during the forecast period. The consumer electronics segment in the region is projected to reach a revenue of around USD 157.2 billion in 2027 from USD 121.1 billion in 2023. By 2027, Europe is projected to be the second-largest electrical and electronics production accounting for around 12.7% of the global market. As a result, the rise in consumer electronics is projected to increase the demand for electrical and electronics production in the coming years.

Europe Engineering Plastics Industry Overview

The Europe Engineering Plastics Market is fragmented, with the top five companies occupying 37.52%. The major players in this market are BASF SE, Covestro AG, Indorama Ventures Public Company Limited, NEO GROUP and SABIC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Fluoropolymer Trade

- 4.2.2 Polyamide (PA) Trade

- 4.2.3 Polycarbonate (PC) Trade

- 4.2.4 Polyethylene Terephthalate (PET) Trade

- 4.2.5 Polymethyl Methacrylate (PMMA) Trade

- 4.2.6 Polyoxymethylene (POM) Trade

- 4.2.7 Styrene Copolymers (ABS and SAN) Trade

- 4.3 Price Trends

- 4.4 Recycling Overview

- 4.4.1 Polyamide (PA) Recycling Trends

- 4.4.2 Polycarbonate (PC) Recycling Trends

- 4.4.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.4.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.5 Regulatory Framework

- 4.5.1 EU

- 4.5.2 France

- 4.5.3 Germany

- 4.5.4 Italy

- 4.5.5 Russia

- 4.5.6 United Kingdom

- 4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Resin Type

- 5.2.1 Fluoropolymer

- 5.2.1.1 By Sub Resin Type

- 5.2.1.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4 Polyvinylfluoride (PVF)

- 5.2.1.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer (LCP)

- 5.2.3 Polyamide (PA)

- 5.2.3.1 By Sub Resin Type

- 5.2.3.1.1 Aramid

- 5.2.3.1.2 Polyamide (PA) 6

- 5.2.3.1.3 Polyamide (PA) 66

- 5.2.3.1.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate (PBT)

- 5.2.5 Polycarbonate (PC)

- 5.2.6 Polyether Ether Ketone (PEEK)

- 5.2.7 Polyethylene Terephthalate (PET)

- 5.2.8 Polyimide (PI)

- 5.2.9 Polymethyl Methacrylate (PMMA)

- 5.2.10 Polyoxymethylene (POM)

- 5.2.11 Styrene Copolymers (ABS and SAN)

- 5.2.1 Fluoropolymer

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 United Kingdom

- 5.3.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Arkema

- 6.4.2 BASF SE

- 6.4.3 Celanese Corporation

- 6.4.4 Covestro AG

- 6.4.5 DSM

- 6.4.6 DuPont

- 6.4.7 Indorama Ventures Public Company Limited

- 6.4.8 INEOS

- 6.4.9 LANXESS

- 6.4.10 Mitsubishi Chemical Corporation

- 6.4.11 NEO GROUP

- 6.4.12 SABIC

- 6.4.13 Solvay

- 6.4.14 Trinseo

- 6.4.15 Victrex

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

2025-2033年工程塑胶市场报告(按类型、性能参数、应用和地区)日本工程塑胶市场报告(按树脂类型、最终用途行业和地区)2025-2033

2025-2033年工程塑胶市场报告(按类型、性能参数、应用和地区)日本工程塑胶市场报告(按树脂类型、最终用途行业和地区)2025-2033 中东工程塑胶:市场占有率分析、产业趋势和成长预测(2024-2029)中国工程塑胶:市场占有率分析、产业趋势与统计、成长预测(2024-2029)亚太工程塑胶:市场占有率分析、产业趋势与统计、成长预测(2024-2029 年)北美工程塑胶:市场占有率分析、行业趋势和统计、成长预测(2024-2029 年)南美工程塑胶:市场占有率分析、行业趋势和统计、成长预测(2024-2029 年)印度工程塑胶市场:市场占有率分析、产业趋势与统计、成长预测(2024-2029)工程塑胶:市场占有率分析、产业趋势和成长预测(2024-2029)德国工程塑胶:市场占有率分析、行业趋势和统计、成长预测(2024-2029 年)

中东工程塑胶:市场占有率分析、产业趋势和成长预测(2024-2029)中国工程塑胶:市场占有率分析、产业趋势与统计、成长预测(2024-2029)亚太工程塑胶:市场占有率分析、产业趋势与统计、成长预测(2024-2029 年)北美工程塑胶:市场占有率分析、行业趋势和统计、成长预测(2024-2029 年)南美工程塑胶:市场占有率分析、行业趋势和统计、成长预测(2024-2029 年)印度工程塑胶市场:市场占有率分析、产业趋势与统计、成长预测(2024-2029)工程塑胶:市场占有率分析、产业趋势和成长预测(2024-2029)德国工程塑胶:市场占有率分析、行业趋势和统计、成长预测(2024-2029 年)

▼