|

市场调查报告书

商品编码

1687072

塑胶瓶和容器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Plastic Bottles and Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

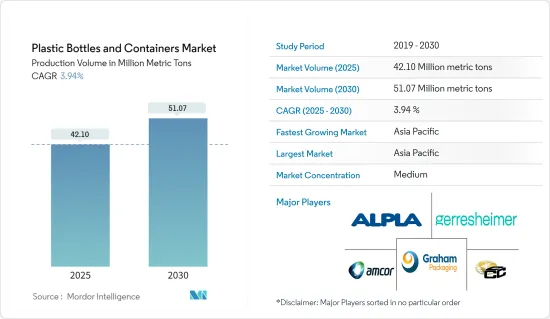

根据生产量计算,塑胶瓶和容器的市场规模预计将从 2025 年的 4,210 万吨扩大到 2030 年的 5,107 万吨,预测期内(2025-2030 年)的复合年增长率为 3.94%。

由聚对苯二甲酸乙二酯、聚丙烯和聚乙烯等材料製成的塑胶瓶和容器因其重量轻、抗破碎、易于物料输送而广泛应用。甚至製造商也更喜欢塑胶包装,因为它的生产成本低。在预计预测期内,成本效益和对包装加工食品以及各种食品和饮料产品的高度依赖将对塑胶瓶和容器市场产生影响。

塑胶因其重量轻的特性而越来越多地被采用,因为轻质塑胶包装可以在运输包装货物时节省能源并减少排放。

塑胶瓶和容器市场价值链正以策略方针实现显着发展。这些策略倡议旨在加强对分销、供应链和生产流程的控制,展现对市场需求的动态响应和对永续成长的追求。该产业可能会透过横向整合、培育规模经济和增强竞争优势来实现进一步整合。

生质塑胶和再生材料等环保材料的迅速普及正在根据循环经济措施和全球环境目标重塑行业格局。

技术进步将重新定义包装功能,用于可追溯性的二维码和最佳保质期标籤等智慧功能将变得越来越普遍。塑胶包装中融入的抗菌特性解决了日益增长的卫生问题,尤其是对于药瓶而言。

随着人们对塑胶污染的担忧日益加剧,製造商和消费者也开始转向其他具有环保特性的包装材料。由于铝和玻璃环保且可回收性高,其消费量可能会增加。

塑胶製造业依赖原料(包括原油和天然气)的成本和供应。这些价格的任何波动都可能影响该行业的盈利和永续性。根据Lindum Packaging Limited介绍,石油是广泛用于包装材料的原料。因此,如果需求激增、供应链出现问题或价格上涨,包装製造商将面临挑战。

塑胶瓶和容器的市场趋势

饮料业将经历显着成长

- 由于瓶装水和非酒精饮料的需求不断增加,饮料行业的塑胶瓶市场预计将扩大。瓶装水的需求源自于消费者对高品质饮用水的倾向、对感染疾病(尤其是饮用受污染的自来水后)的担忧,以及瓶装水的便携性和便利性。

- 宝特瓶水市场的发展受到全球消费者对包装饮用水日益增长的需求的推动,因为与其他包装方式相比,包装饮用水更具成本效益、保质期更长、使用更方便。

- 根据印度饮料协会统计,印度的宝特瓶回收率和再利用率最高,分别为85%和7%。大多数宝特瓶饮用水都以 PET 产品的形式出售,因此用户的成本非常低。

- 碳酸饮料、果汁饮料、果汁、运动饮料、能量饮料等各个类别对宝特瓶的需求都很高,其中水瓶在印度显示出潜在份额,有助于宝特瓶市场的成长。

- 印度铁路餐饮和旅游有限公司推出了其宝特瓶水品牌“Rail Neer”,将在火车上和火车站销售,预计收入将从 2021 年的 5.724 亿印度卢比(693 万美元)大幅增加到 2023 年的 31.5 亿印度卢比(3814 万美元),表明该地区对宝特瓶水的需求呈现有机趋势。

亚太地区预计将占据主要市场占有率

- 过去几年来,该地区的饮料包装市场取得了显着成长。全部区域饮料包装趋势的快速变化是市场成长的主要驱动力。饮料包装的新趋势集中在结构变化、消费后回收等再生材料的开发、顾客接受度、安全性、较新的填充技术、耐热宝特瓶的开发为市场提供了新的可能性和选择,并提高了一些饮料的保质期。

- 百事印度公司宣布,其产品百事黑可乐将于 2023 年 7 月成为印度首个采用 100% 再生宝特瓶生产的碳酸饮料产品。此项措施不包括在完全再生的瓶子上使用百事黑可乐标籤和瓶盖。

- 中国等国家已大幅提高宝特瓶的回收率,并制定了多种策略来适应循环经济,包括替代材料、投资开发生物基塑胶以及设计包装以形成循环。

- 中国糖果零食公司玛氏箭牌于2023年2月推出了首款消费后再生石油PET(rPET)包装。玛氏箭牌采用了本土巧克力品牌翠香的包装。 216 克容器的包装由 100% rPET 製成,符合当地的回收法律和措施。

塑胶瓶和容器市场概况

塑胶瓶和容器市场是一个半固态市场。主要参与者包括 Alpla Group、Amcor Group GmbH、Gerresheimer AG、加拿大 Graham Packaging and Container Corporation。食品和饮料需求增加等因素预计将为塑胶瓶和容器市场提供巨大的成长机会。

2024 年 1 月,ALPLA 收购了位于波多黎各的 Fortiflex。两家公司一直合作为加勒比海和中美洲市场生产包装产品。透过收购 Fortiflex,ALPLA 将加强其于 2023 年成立的大容量包装解决方案工业部门,并扩大其作为完整客户供应商的产品服务。 2023年,ALPLA和Fortiflex将在哥斯大黎加建立一条新的铲斗生产线。

2023年9月,Berry Global为欧洲高端水品牌NEUE Water开发了100%可回收的rPET塑胶瓶。瓶子设计用于包装NEUE Artesian矿泉水,可再填充和重复使用。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 产业价值链分析

- 评估地缘政治趋势的影响

第五章 市场动态

- 市场驱动因素

- 越来越多地采用轻量化包装方法

- 市场挑战/限制

- 与塑胶使用相关的环境问题

第六章 市场细分

- 按材质

- 聚对苯二甲酸乙二醇酯(PET)

- 聚丙烯(PP)

- 低密度聚乙烯(LDPE)

- 高密度聚苯乙烯(HDPE)

- 其他材料

- 按最终用户产业

- 饮料

- 食物

- 化妆品

- 药品

- 家居用品

- 其他行业

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- ALPLA Group

- Amcor Group Gmbh

- Gerresheimer AG

- Graham Packaging

- Container Corporation of Canada

- Altium Packaging

- Apex Plastics(Container Services, Inc.)

- Plastipak Holdings Inc.

- Resilux NV

- Greiner Packaging International Gmbh

- Comar

- Berry Global Inc.

- Retal Industries Limited

- Silgan Holdings Inc.

- Nampak Ltd

第八章投资分析

第九章 市场机会与未来趋势

The Plastic Bottles and Containers Market size in terms of production volume is expected to grow from 42.10 million metric tons in 2025 to 51.07 million metric tons by 2030, at a CAGR of 3.94% during the forecast period (2025-2030).

Plastic bottles and containers that are made of polyethylene terephthalate, polypropylene, polyethylene, etc., are widely used as the material is lightweight and unbreakable, making it easier to handle. Even manufacturers prefer to use plastic packaging, owing to the lower cost of production. The cost-effective nature and dependence on packaged, processed food and various beverages are anticipated to influence the plastic bottles and containers market during the forecast period.

Plastics have been increasingly adopted due to their lightweight properties because lightweight plastic packaging can preserve energy in transporting packed goods and lower emissions.

The value chain of the plastic bottles and containers market is poised for notable developments driven by strategic approaches. These strategic moves aim to enhance control over distribution, supply chains, and production processes, indicating a dynamic response to market demands and a pursuit of sustainable growth. The industry may witness increased consolidation through horizontal integration, fostering economies of scale and bolstering competitiveness.

A surge in adopting eco-friendly materials, such as bioplastics and recycled content, is poised to reshape the industry landscape, aligning with circular economy initiatives and global environmental goals.

Technological advancements will redefine packaging functionality, with smart features like QR codes for traceability and shelf-life indicators becoming prevalent. Anti-microbial properties integrated into plastic packaging will address heightened hygiene concerns, particularly in pharmaceutical bottles.

With growing concerns about plastic pollution, manufacturers and consumers are also inclining themselves toward other packaging materials that offer environment-friendly properties. The consumption of aluminum and glass might witness rising adoption rates owing to their eco-friendly nature and high recyclability.

The plastic manufacturing industry depends on the cost and availability of raw materials, including crude oil and natural gas. Any changes in these prices can impact the industry's profitability and sustainability. According to Lindum Packaging Limited, oil is the raw material used for a broad range of packaging materials. So, when there is an upsurge in demand, a problem with the supply chain or increased prices is where packaging manufacturers will face difficulties.

Plastic Bottles and Containers Market Trends

Beverage Segment to Witness Major Growth

- With the rising demand for bottled water and non-alcoholic beverages, the plastic bottle market in the beverage industry is expected to expand. The demand for bottled water is due to customers' predisposition to want high-quality drinking water, specifically concern about contracting diseases after drinking tainted tap water and the portability and convenience of bottled water.

- The market for bottled water packaging in plastic bottles is driven by the rising demand for packaged drinking water among consumers worldwide because they are more cost-effective than other packaging options, have a longer shelf life, and are easier to use.

- According to the Indian Beverage Association, PET bottles have the greatest recycling and reuse rates in India, at 85% and 7%, respectively. Most packaged drinking water bottles are sold as PET products, which keeps the cost of the product very low for the user.

- Plastic bottles have a significant demand in India in various categories, such as carbonated soft drinks, juice drinks, fruit juices, and sports and energy drinks, out of which water bottles show a potential share in the country, aiding the growth of the plastic bottle market.

- Indian Railways Catering and Tourism Corporation Limited launched a pet bottled water brand, "Rail Neer," which is sold on trains and railway stations, showing significant growth in revenue from INR 572.40 million (USD 6.93 million) in 2021 to INR 3,150 million (USD 38.14 million) in 2023, indicating the organic trend in demand for plastic bottled water in the region.

Asia-Pacific is Expected to Hold Significant Market Share

- The market for beverage packaging has grown significantly over the last few years in the region. Rapid changes in beverage packaging trends across the region are key factors for market growth. The new trends in the packaging of beverages focus on structural changes, and the development of recycled materials like Post-consumer recycling, customer acceptance, safety, newer filling technologies, and the development of heat-resistant PET bottles provided new possibilities and options in the market and improved preservation of several drinks.

- PepsiCo India has announced that its product Pepsi Black will introduce the first 100 % recycled PET plastic bottles in the carbonated beverages category to be manufactured in India in July 2023. The manufacturer does not include the Pepsi Black label and cap for a completely recycled bottle in this initiative.

- Countries like China are witnessing significant recycling rates in plastic bottles, and multiple strategies have been developed to deal with the circular economy, which includes substituting for alternative materials, investments toward the development of bio-based plastics, and designing packaging to make the circular loop.

- Mars Wrigley, the Chinese confectionery company, released its first post-consumer recycled petrified PET (rPET) packaging in February 2023. Mars Wrigley has adopted the packaging of the local chocolate brand Cui Xiang. The packaging of the 216g container is 100% rPET to meet the recycling laws and initiatives in the region.

Plastic Bottles and Containers Market Overview

The plastic bottles and containers market is semi-consolidated in nature. Some of the major players are Alpla Group, Amcor Group GmbH, Gerresheimer AG, Graham Packaging, and Container Corporation of Canada., among others. Factors, including the increasing demand for food and beverages, are expected to provide considerable growth opportunities in the plastic bottles and containers market.

In January 2024, ALPLA acquired the Puerto Rico-based Fortiflex. The two companies have been working together to produce packaging products for Caribbean and Central American markets. ALPLA will reinforce its industrial division for large-volume packaging solutions, which was established in 2023 by acquiring Fortiflex and expanding its offering as a complete customer provider. In 2023, ALPLA and Fortiflex installed a new production line for buckets in Costa Rica.

In September 2023, Berry Global developed a 100% recycled rPET plastic bottle for NEUE Water, a European luxury water brand. The bottle is designed to package NEUE's artesian mineral water and is designed to be refillable and reusable.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of Geopolitical Developments

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Lightweight Packaging Methods

- 5.2 Market Challenges/Restraints

- 5.2.1 Environmental Concerns Regarding Use of Plastics

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Polyethylene Terephthalate (PET)

- 6.1.2 Polypropylene (PP)

- 6.1.3 Low-density Polyethylene (LDPE)

- 6.1.4 High-density Polyethylene (HDPE)

- 6.1.5 Other Material Types

- 6.2 By End-user Vertical

- 6.2.1 Beverages

- 6.2.2 Food

- 6.2.3 Cosmetics

- 6.2.4 Pharmaceuticals

- 6.2.5 Household Care

- 6.2.6 Other End-user Verticals

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ALPLA Group

- 7.1.2 Amcor Group Gmbh

- 7.1.3 Gerresheimer AG

- 7.1.4 Graham Packaging

- 7.1.5 Container Corporation of Canada

- 7.1.6 Altium Packaging

- 7.1.7 Apex Plastics (Container Services, Inc.)

- 7.1.8 Plastipak Holdings Inc.

- 7.1.9 Resilux NV

- 7.1.10 Greiner Packaging International Gmbh

- 7.1.11 Comar

- 7.1.12 Berry Global Inc.

- 7.1.13 Retal Industries Limited

- 7.1.14 Silgan Holdings Inc.

- 7.1.15 Nampak Ltd

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

吹塑成型塑胶瓶市场:依最终用途产业、材料类型、製造技术、产能、瓶型和瓶盖类型划分-全球预测,2025-2032年塑胶瓶和容器市场:按树脂来源、分销管道、产品类型、材料类型和最终用途产业划分-全球预测,2025-2032年

吹塑成型塑胶瓶市场:依最终用途产业、材料类型、製造技术、产能、瓶型和瓶盖类型划分-全球预测,2025-2032年塑胶瓶和容器市场:按树脂来源、分销管道、产品类型、材料类型和最终用途产业划分-全球预测,2025-2032年 亚太地区塑胶瓶和容器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)欧洲塑胶瓶和容器市场:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)

亚太地区塑胶瓶和容器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)欧洲塑胶瓶和容器市场:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年) 塑胶瓶市场规模、份额和成长分析(按材料、数量、技术、最终用途行业和地区)- 2025-2032 年行业预测

塑胶瓶市场规模、份额和成长分析(按材料、数量、技术、最终用途行业和地区)- 2025-2032 年行业预测 药用塑胶瓶市场:按材料、瓶子类型、应用和地区划分

药用塑胶瓶市场:按材料、瓶子类型、应用和地区划分 吹塑成型塑胶瓶市场报告:2031 年趋势、预测与竞争分析中东和非洲:塑胶瓶和容器市场占有率分析、产业趋势和成长预测(2025-2030)北美塑胶瓶和容器:市场占有率分析、行业趋势、统计数据和成长预测(2025-2030)北美塑胶瓶市场:份额分析、产业趋势、成长预测(2025-2030)

吹塑成型塑胶瓶市场报告:2031 年趋势、预测与竞争分析中东和非洲:塑胶瓶和容器市场占有率分析、产业趋势和成长预测(2025-2030)北美塑胶瓶和容器:市场占有率分析、行业趋势、统计数据和成长预测(2025-2030)北美塑胶瓶市场:份额分析、产业趋势、成长预测(2025-2030)