|

市场调查报告书

商品编码

1687178

欧洲塑胶瓶和容器市场:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)Europe Plastic Bottles And Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

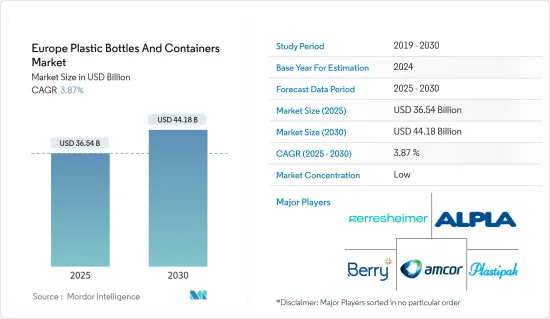

预计 2025 年欧洲塑胶瓶和容器市场规模为 365.4 亿美元,到 2030 年将达到 441.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.87%。

关键亮点

- 由聚对苯二甲酸乙二醇酯、聚丙烯和聚乙烯等材料製成的塑胶瓶和容器占据了包装行业的主导地位。它重量轻且耐用,製造商主要因为其成本效益而选择它。再加上世界对食品和饮料的依赖,这将为未来几年塑胶瓶和容器市场产生重大影响奠定基础。

- 塑胶的快速普及与其轻质特性直接相关。这不仅有助于节省运输过程中的能源,还能减少排放。与玻璃等较重且需要更多运输的替代品相比,塑胶的重量优势更加明显。

- 塑胶瓶和容器由多种材料製成,但由聚对苯二甲酸乙二醇酯 (PET) 製成的塑胶瓶和容器因其耐用性、多功能性和成本效益而脱颖而出。随着欧洲食品、餐饮和製药业的扩张和创新,对塑胶包装,尤其是宝特瓶的需求也随之成长。推出多种口味和包装风格的新饮料的行业趋势进一步推动了对硬质塑胶瓶的需求。

- 饮料业尤其严重依赖宝特瓶宝特瓶,这得益于对瓶装水和非酒精饮料的持续需求。消费者选择瓶装水是因为他们想避免可能受污染的自来水,并且重视瓶装水提供的便利性和便携性。

- 欧盟委员会的一项关注环境问题的研究表明,海洋垃圾中含有大量宝特瓶及其瓶盖。作为回应,欧洲理事会推出了严格的法规,旨在限制一次性塑胶的使用并设定雄心勃勃的回收目标。

- 随着对塑胶污染的担忧日益加剧,製造商和消费者都在探索环保的包装替代品。这种变化明显体现在铝和玻璃的采用日益增加,这两种材料都因其可回收和环保的特性而受到重视。

- 作为这一趋势的体现,2024年3月,欧洲的Brookfield Drinks宣布推出一款100%不含海洋塑胶的瓶子,引起了广泛关注。这款创新瓶是该公司 NEO WTR 系列的一部分,将在 250 家 Tesco超市有售。 Brookfield Drinks 的倡议标誌着一个重要的里程碑,它超越了主要的软性饮料品牌,推出了一系列新的泉水,采用业内首个完全回收的海洋塑胶瓶,配有可回收的瓶盖和标籤。

欧洲塑胶瓶和容器市场趋势

饮料业预计将占据主要市场占有率

- 饮料业正在推动受调查市场的显着成长。塑胶容器和瓶子在这一领域越来越受欢迎,鼓励製造商满足饮料以外的其他终端用户行业的需求。轻量化包装因其具有经济高效和环境友好的双重优势,在包装行业中变得极为重要。由于重量较轻,塑胶瓶和容器在运输过程中所需的能量较少,从而减少燃料消耗、减少碳排放并降低经销商和零售商的成本。

- 根据英国软性饮料协会2024年年度报告,2023年英国瓶装水消费量将达到30.27亿公升,其中塑胶瓶将占95.2%的绝对份额。随着瓶装水消费量的增加,饮料领域对硬质塑胶瓶的需求预计将激增。

- 宝特瓶因其成本效益和阻隔性占据英国饮料市场的主导地位。根据英国软性饮料协会统计,它占软性饮料的68%,碳酸饮料的53%,稀释饮料的95%,运动和能量饮料的42%。

- 欧洲塑胶瓶和容器市场正在显着增加永续性措施。这包括转向更永续的原料,如生质塑胶,并将再生材料整合到产品线中,所有这些都是为了推动创新。 《一次性塑料指令》雄心勃勃地设定了目标,即到 2025 年使用 25% 的再生塑料,到 2030 年使用 30% 的再生塑料,这将彻底改变该行业。这迫使製造商投资回收技术,并表明了对永续性的坚定承诺。

- 随着饮料消费量的增加,瓶装水、碳酸饮料、牛奶等宝特瓶和宝特瓶的需求激增。例如,在德国,人均软性饮料消费量预计将从2020年的114.7公升增加到2023年的124.9公升,凸显了该国对塑胶包装的强劲需求。

德国:预计成长强劲

- 由于解决方案提供者和最终用户的前瞻性倡议,德国对塑胶包装解决方案的采用正在成长。 「德国製造」产品享有很高的消费者认知度,该地区的软包装公司对该产品尤其看好。

- 德国政府对塑胶包装产业实施了严格的监管。虽然宝特瓶在各个领域都很流行,但聚乙烯 (PE) 瓶在饮料、化妆品、卫生和清洁剂领域占据主导地位。

- 随着化妆品消费量的激增和塑胶包装技术的不断创新,市场有望实现成长。塑胶以其重量轻、经济高效和卫生的特性而闻名,特别适合保质期较短的化妆品。透明、密封、高抗压强度且易于成型的宝特瓶正在增强高端化妆品的视觉吸引力,预示着该领域前景光明。

- PET 通常用于製造瓶子和罐子,尤其适用于製造刺激性的化妆品。另一方面,聚氯乙烯(PVC) 通常会被避开,因为它可能与材料反应并导致变形,更不用说它与有害成分有关。该研究涵盖了多种应用,包括护肤、头髮护理、口腔护理、化妆、除臭剂和香水。

- 德国拥有强劲且快速成长的美容和个人护理市场。根据个人护理和洗涤剂行业协会的数据。 V.,市场规模将从 2021 年的 147.229 亿美元飙升至 2023 年的 171.569 亿美元。个人护理市场的扩张凸显了德国在塑胶瓶和容器成长中的重要性。

欧洲塑胶瓶和容器行业概况

研究市场分为以下几个部分:主要参与企业为 Alpha Group、Amcor PLC、Gerresheimer AG、Berry Global Inc.、Plastipak Holdings Inc.、Graham Packaging Company LP 等。

- 2023 年 10 月 - Berry Global Group 为其高端水品牌 NEUE 专门推出了 rPET 瓶。此次发布标誌着 Berry Global 向消费者推出采用 100% 再生宝特瓶NEUE 优质自流矿泉水迈出了重要一步。 NEUE Water 的设计充分考虑了现代快节奏的生活方式。除了环保结构外,该瓶子的创新扁平格式还使其易于携带,并可无缝放入各种运输口袋、包和座椅靠背中。

- 2023 年 10 月 - Plastipak 和 PVG Liquids 合作设计了一种适用于 20L 可堆迭容器的 375G 预製件,可在未来几年内显着减少 500 吨 PET消费量。预计这项技术创新每年将减少二氧化碳排放量约200吨。 Plastipac 在义大利韦尔巴尼亚的工厂进行生产是减少运输过程中排放的策略性倡议。容器本身由新型低结晶质树脂与创新预製件结合而成。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 产业价值链分析

第五章市场动态

- 市场驱动因素

- 轻量化包装方法的采用日益增多

- 人口和生活方式的变化

- 市场限制

- 人们对塑胶使用的环境担忧日益加剧

- 贸易情景

- 进出口资料

- 贸易分析(前五大出口/进口国家、价格分析、主要港口等)

- 贸易分析(前五大出口/进口国家、价格分析、主要港口等)

- 行业法规、政策和标准

- 科技

- 价格趋势分析

- 塑胶树脂(当前价格和历史趋势)

第六章市场区隔

- 按树脂

- 聚乙烯(PE)

- 聚对苯二甲酸乙二醇酯(PET)

- 聚丙烯(PP)

- 其他树脂类型(聚苯乙烯、聚氯乙烯、聚碳酸酯等)

- 按产品

- 瓶子

- 瓶子

- 罐

- 盒子

- 加仑

- 标籤

- 其他的

- 按最终用途行业

- 食物

- 饮料

- 瓶装水

- 碳酸饮料

- 牛奶

- 其他饮料

- 製药

- 个人护理和盥洗用品

- 工业的

- 日用化学品

- 画

- 其他的

- 按国家

- 法国

- 德国

- 义大利

- 英国

- 西班牙

- 波兰

第七章竞争格局

- 公司简介

- Amcor Group GmbH

- Gerresheimer AG

- Plastipak Holdings Inc.

- ALPLA Group

- Berry Global Inc.

- Alpha Packaging Inc.

- Graham Packaging

- Resilux NV

- Greiner Packaging International GmbH

- Comar LLC

- 热图分析

- 竞争对手分析-新兴企业vs. 现有公司

第八章 回收与永续性前景

第九章:市场的未来

The Europe Plastic Bottles And Containers Market size is estimated at USD 36.54 billion in 2025, and is expected to reach USD 44.18 billion by 2030, at a CAGR of 3.87% during the forecast period (2025-2030).

Key Highlights

- Plastic bottles and containers manufactured from materials like polyethylene terephthalate, polypropylene, and polyethylene, dominate the packaging landscape. Their lightweight and durable nature makes them a preferred choice for manufacturers, primarily due to their cost-effectiveness. This, coupled with the global reliance on packaged foods and beverages, sets the stage for a significant impact on the plastic bottles and containers market in the coming years.

- The surge in plastic adoption is directly tied to its lightweight properties. This not only aids in energy conservation during transportation but also reduces emissions. Plastic's weight advantage becomes even more apparent when compared to heavier alternatives like glass, which necessitate more trips for transportation.

- While plastic bottles and containers can be crafted from various materials, those made from polyethylene terephthalate (PET) stand out for their durability, versatility, and cost-efficiency. As Europe's food, beverage, and pharmaceutical sectors expand and innovate, the demand for plastic packaging, especially PET bottles, rises in tandem. The industry's trend of introducing new beverages in diverse flavors and packaging styles further bolsters the demand for rigid plastic bottles.

- The beverage sector, in particular, heavily leans on plastic bottles, driven by the perpetual demand for bottled water and non-alcoholic drinks. Consumers seek bottled water for its perceived purity, shunning potentially contaminated tap water, and valuing the convenience and portability it offers.

- Highlighting environmental concerns, a European Commission study underscored the prevalence of PET bottles and their lids in ocean debris. In response, the European Council has rolled out stringent regulations, aiming to curb the use of single-use plastics and set ambitious recycling targets.

- Amid mounting worries over plastic pollution, both manufacturers and consumers are exploring eco-friendlier packaging alternatives. This shift is evident in the rising adoption rates of aluminum and glass, lauded for their recyclability and environmentally conscious attributes.

- Illustrating this trend, in March 2024, Europe's Brookfield Drinks made waves by announcing the launch of a 100% Prevented Ocean Plastic bottle. This innovative bottle, part of their NEO WTR range, is set to debut in 250 Tesco superstores. Brookfield Drinks' initiative marks a significant milestone, outpacing major soft drink brands by introducing a new spring water range in the industry's first fully recycled ocean-bound plastic bottle, complete with a recyclable cap and label.

Europe Plastic Bottles and Containers Market Trends

The Beverages Segment is Expected to Hold a Significant Market Share

- The beverage industry is driving significant growth in the market under study. Plastic containers and bottles are gaining popularity within this sector, prompting manufacturers to cater not only to beverages but also to other end-user industries. Lightweight packaging has emerged as a pivotal force in the packaging industry, owing to its dual benefits: economic efficiency and environmental friendliness. Given their lightweight nature, plastic bottles and containers reduce energy consumption during transportation, leading to lower fuel usage, reduced carbon emissions, and decreased costs for distributors and retailers.

- As per the 2024 Annual Report by the British Soft Drink Association, the United Kingdom consumed 3,027 million liters of bottled water in 2023, with plastic bottles representing a dominant 95.2% share. With bottled water consumption on the rise, the demand for rigid plastic bottles in the beverage sector is set to surge.

- Plastic bottles, due to their cost-effectiveness and barrier properties, hold a lion's share in the United Kingdom's beverage landscape. They make up 68% of soft drink consumption, 53% of carbonated drinks, 95% of dilutables, and 42% of sports and energy drinks, as highlighted in the British Soft Drink Association's findings.

- Across the European plastic bottles and containers market, there's a notable uptick in sustainability initiatives. These include a shift towards sustainable raw materials like bioplastics and integrating recycled content into product lines, all aimed at fostering innovation. The ambitious targets set by the Single-Use-Plastic Directive - 25% recycled content by 2025 and 30% by 2030 - are poised to revolutionize the industry. Manufacturers are thus compelled to invest in recycling technologies, signaling a steadfast commitment to sustainability.

- With beverage consumption on the rise, the demand for plastic bottles and containers for bottled water, carbonated drinks, or milk is surging. Germany, for instance, saw its per capita soft drink consumption climb from 114.7 liters in 2020 to a projected 124.9 liters in 2023, underscoring the country's robust appetite for plastic packaging.

Germany is Expected to Witness Significant Growth

- Germany is increasingly embracing plastic packaging solutions, driven by advancements from both solution providers and end users. The renowned consumer perception of "Made in Germany" products has notably favored the region's flexible packaging companies.

- The German government has implemented stringent regulations for the plastic packaging industry. While PET bottles are prevalent across various sectors, polyethylene (PE) bottles dominate sales in beverages, cosmetics, sanitary, and detergent segments.

- With a surge in cosmetic consumption and continuous innovation in plastic packaging technology, the market is poised for growth. Plastic, known for its lightweight, cost-effectiveness, and hygienic properties, is particularly well-suited for cosmetics, especially those with shorter shelf lives. Transparent, airtight, and easily moldable with good compressive strength, PET plastic bottles are enhancing the visual appeal of high-end cosmetics, indicating a promising future for this segment.

- PET finds common use in both bottles and jars, especially favored for aggressive cosmetics. On the other hand, polyvinyl chloride (PVC) is generally shunned due to its potential to react with and distort materials, not to mention its association with hazardous components. The study covers a range of applications, including skincare, haircare, oral care, makeup, deodorants, fragrances, and more.

- Germany boasts a robust beauty and personal care market, witnessing rapid growth. According to the Personal Care and Detergent Industry Association e. V., the market value surged from USD 14,722.9 million in 2021 to USD 17,156.9 million in 2023. This expanding personal care market underscores Germany's significance in the growth of plastic bottles and containers.

Europe Plastic Bottles and Containers Industry Overview

The market studied is fragmented, with some significant players such as Alpha Group, Amcor PLC, Gerresheimer AG, Berry Global Inc., Plastipak Holdings Inc., and Graham Packaging Company LP. These companies increase their market shares by launching new products and forming partnerships and mergers. Some of the recent developments are:

- October 2023 - Berry Global Group introduced a rPET bottle specifically for the upscale water brand, NEUE. This launch marks a significant step as Berry Globalprovides 100% recycled PET bottles for NEUE's premium artesian mineral water. NEUE Water is designed with the contemporary, fast-paced lifestyle in mind. In addition to its eco-friendly composition, the bottle's innovative flat shape ensures convenient portability, fitting seamlessly into pockets, bags, and even seatback storage on various modes of transport.

- October 2023 - Plastipak and PVG Liquids have jointly engineered a 375g preform tailored for a 20-liter stackable container, designed to significantly slash PET consumption by 500 tons in the coming years. This innovation is projected to curtail CO2 emissions by approximately 200 tons annually. The production, situated at Plastipak's Verbania plant in Italy, is a strategic move to minimize emissions during transit. The container itself is crafted from a novel low-crystallinity resin, paired with the innovative preform.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Lightweight Packaging Methods

- 5.1.2 Changing Demographic and Lifestyle Factors

- 5.2 Market Restraints

- 5.2.1 Growing Environmental Concerns Over the Use of Plastics

- 5.3 Trade Scenario

- 5.3.1 EXIM Data

- 5.3.2 Trade Analysis (Top 5 Import-Export Countries, Price Analysis, and Key Ports, Among others)

- 5.4 Trade Analysis (Top 5 Import-Export Countries, Price Analysis, and Key Ports, Among others)

- 5.5 Industry Regulation, Policy and Standards

- 5.6 Technology Landscape

- 5.7 Pricing Trend Analysis

- 5.7.1 Plastic Resins (Current Pricing and Historic Trends)

6 MARKET SEGMENTATION

- 6.1 By Resin

- 6.1.1 Polyethylene (PE)

- 6.1.2 Polyethylene Terephthalate (PET)

- 6.1.3 Polypropylene (PP)

- 6.1.4 Other Resin Type (Polystyrene, PVC, Polycarbonate, etc.)

- 6.2 By Product

- 6.2.1 Bottles

- 6.2.2 Jars

- 6.2.3 Canisters

- 6.2.4 Boxes

- 6.2.5 Gallons

- 6.2.6 Tubs

- 6.2.7 Other Products

- 6.3 By End-use Industries

- 6.3.1 Food

- 6.3.2 Beverage

- 6.3.2.1 Bottled Water

- 6.3.2.2 Carbonated Soft Drinks

- 6.3.2.3 Milk

- 6.3.2.4 Other Beverages

- 6.3.3 Pharmaceuticals

- 6.3.4 Personal Care & Toiletries

- 6.3.5 Industrial

- 6.3.6 Household Chemicals

- 6.3.7 Paints & Coatings

- 6.3.8 Other End-use Industries

- 6.4 By Country

- 6.4.1 France

- 6.4.2 Germany

- 6.4.3 Italy

- 6.4.4 United Kingdom

- 6.4.5 Spain

- 6.4.6 Poland

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Gerresheimer AG

- 7.1.3 Plastipak Holdings Inc.

- 7.1.4 ALPLA Group

- 7.1.5 Berry Global Inc.

- 7.1.6 Alpha Packaging Inc.

- 7.1.7 Graham Packaging

- 7.1.8 Resilux NV

- 7.1.9 Greiner Packaging International GmbH

- 7.1.10 Comar LLC

- 7.2 Heat Map Analysis

- 7.3 Competitor Analysis - Emerging vs. Established Players

8 RECYCLING & SUSTAINABILITY LANDSCAPE

9 FUTURE OF THE MARKET

塑胶瓶和容器市场:2026-2032年全球市场预测(按树脂原料、产品类型、材料类型、分销管道和最终用途行业划分)

塑胶瓶和容器市场:2026-2032年全球市场预测(按树脂原料、产品类型、材料类型、分销管道和最终用途行业划分) 吹塑成型瓶市场-2026-2031年预测

吹塑成型瓶市场-2026-2031年预测 塑胶瓶和容器:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)

塑胶瓶和容器:市场份额分析、行业趋势和统计数据、成长预测(2026-2031) 塑胶瓶市场规模、份额和成长分析(按材料、销售、技术、终端用途产业和地区划分)-2026-2033年产业预测亚太地区塑胶瓶和容器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

塑胶瓶市场规模、份额和成长分析(按材料、销售、技术、终端用途产业和地区划分)-2026-2033年产业预测亚太地区塑胶瓶和容器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 吹塑成型塑胶瓶市场报告:2031 年趋势、预测与竞争分析中东和非洲:塑胶瓶和容器市场占有率分析、产业趋势和成长预测(2025-2030)北美塑胶瓶和容器:市场占有率分析、行业趋势、统计数据和成长预测(2025-2030)北美塑胶瓶市场:份额分析、产业趋势、成长预测(2025-2030)塑胶瓶:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

吹塑成型塑胶瓶市场报告:2031 年趋势、预测与竞争分析中东和非洲:塑胶瓶和容器市场占有率分析、产业趋势和成长预测(2025-2030)北美塑胶瓶和容器:市场占有率分析、行业趋势、统计数据和成长预测(2025-2030)北美塑胶瓶市场:份额分析、产业趋势、成长预测(2025-2030)塑胶瓶:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)