|

市场调查报告书

商品编码

1693537

南美洲特种肥料:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)South America Specialty Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

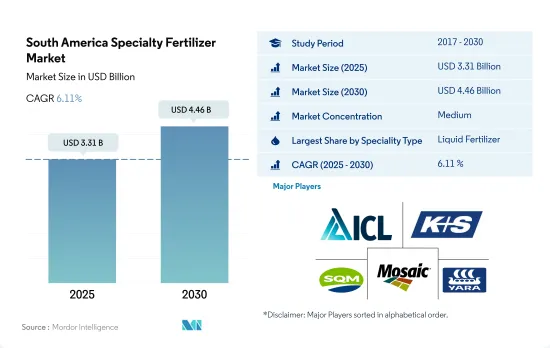

南美特种肥料市场规模预计在 2025 年为 33.1 亿美元,预计到 2030 年将达到 44.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.11%。

水溶性肥料占据市场主导地位,因为它们适用于各种农业系统

- 2022年,水溶性肥料在南美洲特种肥料市场占据42.3%的绝对份额。水溶性肥料 (WSF) 简化了营养管理,因为营养水平不受浸出或侵蚀的影响。施肥是水耕和滴灌等现代农业系统的重要组成部分,而水溶性肥料的使用使施肥变得更加容易。

- 2022年南美洲特种肥料市场中,液体肥料占51.6%的份额。该地区的种植者越来越意识到液体肥料的好处。这些肥料很容易渗透到土壤中,使植物能够快速吸收养分,同时最大限度地减少浪费。它可以用于地面或叶面,为南美洲提供了巨大的生长机会。

- 2022 年南美洲控制释放肥料市场的占有率仅为 2.8%。在控制释放肥料中,聚合物包膜性肥料占76.3%的份额。人们对开发创新且环保的控制释放肥料的兴趣日益浓厚,推动了这个市场的蓬勃发展。预计未来几年控制释放肥料市场的复合年增长率将达到 6.7%。

- 缓释肥料是指随着时间的推移逐渐释放养分的肥料,仅占南美洲特种肥料市场的 2.4%。这些肥料在水、热、阳光和土壤微生物的作用下逐渐分解,从而丰富土壤。由于特种肥料市场潜力的不断扩大,预计控释领域将在 2023 年至 2030 年间显着成长。

巴西凭藉其广阔的土地和巨大的农业潜力占据市场主导地位。

- 2022年,巴西作为全球农业领域的重要参与者,成为大米、玉米、大豆和咖啡等商品的主要出口国。巴西特种肥料市场价值18亿美元,同年消费量为200万吨。

- 阿根廷严重依赖农业,主要作物是小麦、玉米和大豆。该国的化肥消费量引人注目,平均施用量为259.4公斤/公顷。 2022年,阿根廷特种肥料消费量量占该地区的14.1%。

- 该地区特种肥料的消费量自 2017 年以来一直呈上升趋势,从 289,600 吨跃升至 2022 年的 430,200 吨。市场价值一直保持持续成长,直到 2019 年新冠疫情扰乱了贸易和供应链。鑑于该地区对化肥进口的依赖,该期间化肥价格呈现上涨趋势。

- 其余南美国家,包括智利、哥伦比亚、秘鲁、玻利维亚和巴拉圭,将在2022年总合该地区特种肥料消费量的25.9%。这些国家拥有多样化的农业,从谷物到水果和蔬菜,农业是人民的主要收入来源。

- 随着耕地面积的不断扩大以及干旱、热浪等气候风险的加剧,南美洲特种肥料市场可望实现成长。这些挑战促使人们采用更有效率的肥料。

南美洲特种肥料市场趋势

巴西政府努力实现作物生产自给自足

- 南美洲田间作物种植面积将增加 12.8%,从 2017 年的 1.116 亿公顷增加到 2022 年的 1.261 亿公顷。预计种植面积的激增将推动该地区的化肥需求。田间作物占比较大,达96.8%。到2022年,巴西将以56.9%的市占率占据主导地位,其次是阿根廷,市占率29.3%。巴西被誉为全球大豆生产和出口大国,2021年大豆产量近1.35亿吨,其中出口大豆製品1.055亿吨,其中生大豆占82%,豆饼占16%,豆油占2%。

- 在南美洲,巴西和阿根廷是大豆种植最多的国家,分别占全球种植面积的64.4%和26.1%。然而,该地区长期遭受干旱,导致主要河流水位极低。这造成了严重后果,扰乱了重要夏季作物(尤其是大豆)的收成和运输。因此,这种情况刺激了南美洲对化学肥料的需求增加。

- 近年来,由于全球需求强劲且盈利较强,南方共同市场地区的大豆种植面积迅速增加。大豆等大宗商品价格高企,鼓励生产商扩大经营,投资新土地设备,以提高规模和效率。因此,该地区田间作物种植面积将随着国内和国际市场的成长而扩大。

南美洲田间作物平均主要养分施用量约172.73公斤/公顷。

- 南美洲是大豆、玉米、小麦和玉米等田间作物的主要产地。过去二十年来,由于耕地面积增加和努力实现产量,这些作物的产量大幅增加。随着巴西等国的种植者继续扩大耕地面积,作物产量预计将进一步增加,这反过来可能导致化肥消费量增加。

- 营养物质对植物的健康、生长和作物产量起着至关重要的作用。主要营养物质对于田间作物来说尤其重要,因为它们为植物的生长提供了基本组成部分。这些营养物质包括氮、磷和钾,其中任何一种营养物质的缺乏都会对作物的产量和品质产生重大影响。 2022年南美洲田间作物主要养分平均施用量约172.7公斤/公顷。在所有主要养分中,氮施用量最高,为193.8公斤/公顷,其次是钾,为181.9公斤/公顷,磷为142.4公斤/公顷。

- 在所有田间作物中,小麦、水稻和玉米预计平均养分施用量最高。具体来说,小麦的平均养分施用量预计为231公斤/公顷,水稻和玉米的平均施用量预计分别为156公斤/公顷和149公斤/公顷。在南美洲,人口成长导致对田间作物的需求增加,从而导致主要作物的种植面积增加。因此,预计未来几年田间作物的主要养分使用量将大幅增加。

南美洲特种肥料产业概况。

南美洲特种肥料市场适度整合,前五大公司占58.59%的市场。该市场的主要企业有:ICL Group Ltd、K+S Aktiengesellschaft、Sociedad Química y Minera de Chile SA、The Mosaic Company 和 Yara International ASA(按字母顺序排列)

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 主要作物种植面积

- 田间作物

- 园艺作物

- 平均养分施用量

- 微量营养素

- 田间作物

- 园艺作物

- 主要营养素

- 田间作物

- 园艺作物

- 次要宏量营养素

- 田间作物

- 园艺作物

- 微量营养素

- 灌溉农田

- 法律规范

- 价值炼和通路分析

第五章市场区隔

- 专业类型

- CRF

- 聚合物涂层

- 聚合硫涂层

- 其他的

- 液体肥料

- SRF

- 水溶性

- CRF

- 施肥方式

- 受精

- 叶面喷布

- 土壤

- 作物类型

- 田间作物

- 园艺作物

- 草坪和观赏植物

- 原产地

- 阿根廷

- 巴西

- 南美洲其他地区

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- EuroChem Group

- Grupa Azoty SA(Compo Expert)

- Haifa Group

- ICL Group Ltd

- K+S Aktiengesellschaft

- Sociedad Quimica y Minera de Chile SA

- The Mosaic Company

- TIMAC Agro

- Yara International ASA

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

The South America Specialty Fertilizer Market size is estimated at 3.31 billion USD in 2025, and is expected to reach 4.46 billion USD by 2030, growing at a CAGR of 6.11% during the forecast period (2025-2030).

Water soluble fertilizers dominated the market due to their suitability for various agricultural systems

- In 2022, water-soluble fertilizers held a dominant share of 42.3% in South America's specialty fertilizer market. Water soluble fertilizers (WSF) simplify nutrition management because nutrient levels are not affected by leaching or erosion. Fertigation, a key component of modern agricultural systems like hydroponics and drip irrigation, is made user-friendly with water-soluble fertilizers.

- Liquid fertilizers took the lion's share of 51.6% in South America's specialty fertilizer market in 2022. Growers in the region are increasingly recognizing the benefits of liquid fertilizers. These fertilizers not only penetrate the soil easily, enabling faster nutrient absorption by plants, but also minimize waste. They can be applied to both the ground and foliage, presenting a significant growth opportunity in South America.

- The controlled-release fertilizer market in South America held a modest share of 2.8% in 2022. Among controlled-release fertilizers, polymer-coated variants dominated, commanding a 76.3% share. This market is being propelled by a rising interest in developing innovative and environmentally friendly controlled-release fertilizers. Projections indicate a 6.7% CAGR for the controlled-release fertilizer market in the coming years.

- Slow-release fertilizers, which gradually release nutrients over time, accounted for a modest 2.4% of South America's specialty fertilizer market. These fertilizers, influenced by water, heat, sunlight, and soil microbes, gradually break down and decompose, enriching the soil. Given the expanding market potential for specialty fertilizers, the slow-release segment is poised for significant growth from 2023 to 2030.

Brazil dominated the market owing to the larger area and greater agricultural potential.

- In 2022, Brazil, a significant player in the global agricultural sector, stood as a key exporter of commodities such as rice, maize, soybean, and coffee. The specialty fertilizer market in Brazil was valued at USD 1.8 billion, and it witnessed a consumption of 2.0 million metric ton in the same year.

- Argentina heavily relies on its agricultural sector, with wheat, corn, and soybean being prominent crops. The country's fertilizer consumption is notable, with an average application rate of 259.4 kg/ha. In 2022, Argentina accounted for 14.1% of the region's specialty fertilizer consumption.

- Specialty fertilizer consumption in the region has been on the rise since 2017, surging from 289.6 thousand metric ton to 430.2 thousand metric ton in 2022. The market value showed consistent growth until 2019 when the COVID-19 pandemic disrupted trade and supply chains. Given the region's reliance on fertilizer imports, prices saw an upward trend during the period.

- The remaining South American countries, including Chile, Colombia, Peru, Bolivia, and Paraguay, collectively represented 25.9% of the region's specialty fertilizer consumption in 2022. These countries boast a diverse agricultural landscape, spanning from cereals to fruits and vegetables, with agriculture serving as a primary income source for their populations.

- With an expanding cultivation area and escalating climate risks like droughts and heatwaves, the South American specialty fertilizer market is poised for growth. These challenges are driving the adoption of more efficient fertilizers.

South America Specialty Fertilizer Market Trends

The Brazilian government's initiatives to achieve self-sufficiency in crop production

- The cultivation area for field crops in South America witnessed a 12.8% increase, rising from 111.6 million ha in 2017 to 126.1 million ha in 2022. This surge in cultivation area is projected to drive up the demand for fertilizers in the region. Field crops dominated the landscape, occupying a significant 96.8% share. In 2022, Brazil held the lion's share of the market at 56.9%, with Argentina trailing at 29.3%. Brazil, renowned as the global leader in soy production and exports, saw its soy output reach nearly 135 million tonnes in 2021. Out of this, a substantial 105.5 million tonnes of soy products were exported, with 82% in raw soybean form, 16% as soybean cake, and 2% as soybean oil.

- Soybean cultivation reigns supreme in South America, with Brazil and Argentina leading the pack, accounting for 64.4% and 26.1% of the cultivated area, respectively. However, the region is grappling with an extended drought, resulting in alarmingly low water levels in major rivers. This has severe repercussions, hampering both harvests and the transportation of crucial summer crops, especially soybeans. Consequently, the prevailing conditions are amplifying the demand for increased fertilizer application in South America.

- The Mercosur region has witnessed a surge in soybean cultivation, driven by robust global demand and the crop's attractive profitability in recent years. The surge in commodity prices, including soy, has incentivized producers to expand their operations, investing in new lands and equipment to enhance scale and efficiency. As a result, the field crop cultivation area in the region is poised to expand in tandem with the growing domestic and international markets.

The average rate of primary nutrient application for field crops in the South American region is about 172.73 kg/hectare

- South America is a major producer of field crops such as soybeans, corn, wheat, and maize. Over the last two decades, the production of these crops has experienced a significant rise due to an increase in cultivated land and efforts to achieve higher yields. As growers in countries like Brazil continue to expand their cultivated areas, it is expected that crop production will further increase, which, in turn, may lead to a rise in fertilizer consumption.

- Nutrients play a crucial role in plant health, growth, and crop production output. Primary nutrients, in particular, are essential for field crops as they provide the basic building blocks for plant development. These nutrients include nitrogen, phosphorus, and potassium, and a deficiency in any of them can have a significant impact on crop yield and quality. The average rate of primary nutrient application for field crops in South America was about 172.7 kg/hectare in 2022. Among all the primary nutrients, nitrogen had the highest application rate of 193.8 kg/hectare, followed by potassium with 181.9 kg/hectare, while phosphorous had an application rate of 142.4 kg/hectare.

- Among all the field crops, wheat, rice, and corn/maize are predicted to have the highest average nutrient application rate. Specifically, wheat is projected to have an average nutrient application rate of 231 kg/ha, while rice and corn/maize are estimated to have average rates of 156 kg/ha and 149 kg/ha, respectively. In South America, the demand for field crops has been on the rise due to the growing population, leading to an increase in the area harvested under major food crops. As a result, the use of primary nutrients in field crops is expected to increase significantly in the coming years.

South America Specialty Fertilizer Industry Overview

The South America Specialty Fertilizer Market is moderately consolidated, with the top five companies occupying 58.59%. The major players in this market are ICL Group Ltd, K+S Aktiengesellschaft, Sociedad Quimica y Minera de Chile SA, The Mosaic Company and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Speciality Type

- 5.1.1 CRF

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 SRF

- 5.1.4 Water Soluble

- 5.1.1 CRF

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Country

- 5.4.1 Argentina

- 5.4.2 Brazil

- 5.4.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 EuroChem Group

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Haifa Group

- 6.4.4 ICL Group Ltd

- 6.4.5 K+S Aktiengesellschaft

- 6.4.6 Sociedad Quimica y Minera de Chile SA

- 6.4.7 The Mosaic Company

- 6.4.8 TIMAC Agro

- 6.4.9 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

晶体肥料市场:2026-2032年全球市场预测(依养分类型、应用、形态、作物类型、作用机制与销售管道)特种肥料市场:2026-2032年全球市场预测(依产品形式、作物类型、养分类型、施用方法、通路和最终用途划分)

晶体肥料市场:2026-2032年全球市场预测(依养分类型、应用、形态、作物类型、作用机制与销售管道)特种肥料市场:2026-2032年全球市场预测(依产品形式、作物类型、养分类型、施用方法、通路和最终用途划分) 特种肥料市场规模、份额和趋势分析报告:按技术、作物、类型、应用、地区和细分市场预测(2026-2033 年)

特种肥料市场规模、份额和趋势分析报告:按技术、作物、类型、应用、地区和细分市场预测(2026-2033 年) 特种肥料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

特种肥料:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球特种肥料市场规模、份额、趋势和成长分析报告(2026-2034)

全球特种肥料市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球特种肥料市场报告

2026年全球特种肥料市场报告 特种肥料市场规模、份额和成长分析(按类型、技术、形态、作物类型、应用方法和地区划分)-2026-2033年产业预测全球特种肥料市场规模(依特种肥料类型、作物类型、施用方法、区域范围及预测)

特种肥料市场规模、份额和成长分析(按类型、技术、形态、作物类型、应用方法和地区划分)-2026-2033年产业预测全球特种肥料市场规模(依特种肥料类型、作物类型、施用方法、区域范围及预测) 特种肥料市场 - 全球产业规模、份额、趋势、机会和预测,按作物类型、形式、应用方式、技术、地区和竞争细分,2020-2030 年中东和非洲特种肥料:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)

特种肥料市场 - 全球产业规模、份额、趋势、机会和预测,按作物类型、形式、应用方式、技术、地区和竞争细分,2020-2030 年中东和非洲特种肥料:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)