|

市场调查报告书

商品编码

1693539

非洲特种肥料:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Africa Specialty Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

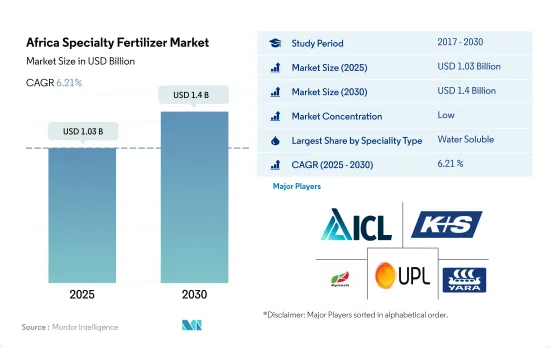

预计 2025 年非洲特种肥料市场规模为 10.3 亿美元,到 2030 年将达到 14 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.21%。

与传统肥料相比,特种肥料的各种优势预计将推动市场成长。

- 2022年,控制释放肥料(CRF)占特种肥料市场的7.4%。控释肥的稳定成长归因于其相对于传统肥料的独特优势以及人们对高效耕作方法的认识不断提高。 CRF 在很长一段时间内逐渐释放养分,确保为植物稳定供应养分。这不仅减少了营养物质的浪费,而且还最大限度地降低了传统肥料中常见的浸出和蒸发风险。

- 水溶性肥料的市场占有率为 47.8%,在 2022 年特种肥料市场中排名第二。使用水溶性肥料显示出减少种植健康植物所需的水和肥料的潜力。

- 受灌溉系统进步和水耕、鱼菜共生等先进栽培技术的日益普及的推动,液体肥料市场有望实现成长。预计 2023 年至 2030 年间液体肥料市场价值的复合年增长率为 5.8%。

- 采用缓效肥料不仅为农民带来经济效益,还有节省用水、防止氮挥发和淋溶、减少处理肥料所需劳动力等环境效益。由于这些因素,缓释肥料的市场价值预计在 2023 年至 2023 年间将成长 5.4%。

- 鑑于特种肥料的益处,例如精确释放养分、减少施肥量以及为农民带来经济效益,特种肥料市场在未来几年有望实现成长。

政府措施和农民对提高生产力的关注预计将推动市场成长

- 2022 年,尼日利亚在非洲特种肥料市场占有 27.0% 的主导份额。该国的农业部门面临着复杂的土地所有权问题、灌溉基础设施不足、气候变迁的不利影响以及逐步采用尖端农业技术等挑战,但政府的倡议使市场得以成长。这些政策包括农业促进政策(APP)、尼日利亚-非洲贸易和投资促进计划、国家农业技术和创新计划(NATIP)和锚定借款人计划(ABP),所有这些政策都有助于提高农业生产力。

- 南非是非洲大陆最先进、最丰饶、最多样化的农业地区。 2022 年,强劲的农业部门占据了非洲特种肥料市场总量的 37.0% 的份额。预计预测期内市场复合年增长率将达到 6.7%。这一预期成长主要是由于人们越来越需要透过采用更有效率的肥料解决方案来减轻长期干旱和极端高温等气候相关风险的影响。

- 由于人口快速增长、可耕地面积减少、迫切需要提高现有农地的产量以及努力提高全部区域的农业生产率,非洲特种肥料市场预计将扩大。预计 2023 年至 2030 年的复合年增长率将达到 6.0%。

非洲特种肥料市场趋势

由于国内需求不断增长,预计不久的将来农业产量将翻倍。

- 非洲的农业生态区从每年降雨两次的茂密热带雨林到降雨稀少的干旱沙漠。该地区的主要田间作物包括玉米、高粱、小麦和水稻。到2022年,这些作物的种植面积将达到2.248亿公顷,占该地区农业用地的95%以上。由于玉米库存过剩抑制了价格,南非玉米种植者在2018-19年度将玉米种植面积减少了10%,至210万公顷。结果,该国玉米产量下降了11%,从1300万吨下降到1200万吨,而出口量从250万吨下降到100万吨。这种转变促使农民将更多土地分配给作物,尤其是大豆,导致2018-2019年非洲各地玉米种植面积下降。

- 尼日利亚是非洲最大的高粱生产国,紧随其后的是衣索比亚。高粱占尼日利亚谷物总产量的50%,约占尼日利亚谷物种植面积的45%。高粱以其耐旱、耐涝而闻名,能够在各种土壤条件下生长。这些特性使高粱成为非洲干旱地区的主要作物,确保了粮食安全和收入安全。

- 肯亚、索马利亚和衣索比亚大部分地区正面临严重的粮食安全危机。过去十年,非洲的农业和可耕地面积不断扩大,但其粮食进口支出却增加了近两倍。

油菜是氮消费量最高的作物

- 油菜籽钾、磷施用量最高,分别为162.4公斤/公顷、281.7公斤/公顷。同时,非洲田间作物平均施氮量为364.9公斤/公顷。 2022年,非洲田间作物占一次养分总消费量的87.1%,达55.61万吨。这项优势得益于用于田间作物的土地面积广阔。其中,氮、磷、钾养分平均施用量分别为每作物223.2公斤、125.3公斤、155.3公斤。

- 尼日利亚的几内亚大草原为玉米生产提供了适当的环境条件。然而,儘管有这样的潜力,该地区的农民仍然在为低产量而苦苦挣扎。主要原因是由于土地集约利用导致土壤劣化和养分耗尽(主要是氮)。田间作物优先施用氮肥,因为氮肥具有多种益处,包括犁地、增加叶面积、形成籽粒、灌浆和促进蛋白质合成。氮在提高作物产量和品质方面也发挥着重要作用。

- 主要营养成分对于作物生长至关重要,由于对土壤枯竭和氮气淋失的担忧,预计未来几年主要营养成分的施用率将大幅增加。

非洲特种肥料产业概况

非洲特种肥料市场较分散,前五大企业占29.76%。市场的主要企业有:ICL Group Ltd、K+S Aktiengesellschaft、Kynoch Fertilizer、UPL Limited 和 Yara International ASA(按字母顺序排列)

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 主要作物种植面积

- 田间作物

- 园艺作物

- 平均养分施用量

- 微量营养素

- 田间作物

- 园艺作物

- 主要营养素

- 田间作物

- 园艺作物

- 次要宏量营养素

- 田间作物

- 园艺作物

- 微量营养素

- 灌溉农田

- 法律规范

- 价值炼和通路分析

第五章市场区隔

- 专业类型

- CRF

- 聚合物涂层

- 聚合硫涂层

- 其他的

- 液体肥料

- SRF

- 水溶性

- CRF

- 施肥方式

- 受精

- 叶面喷布

- 土壤

- 作物类型

- 田间作物

- 园艺作物

- 草坪和观赏植物

- 原产地

- 奈及利亚

- 南非

- 其他非洲国家

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- Gavilon South Africa(MacroSource, LLC)

- Haifa Group

- ICL Group Ltd

- K+S Aktiengesellschaft

- Kynoch Fertilizer

- UPL Limited

- Yara International ASA

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 92604

The Africa Specialty Fertilizer Market size is estimated at 1.03 billion USD in 2025, and is expected to reach 1.4 billion USD by 2030, growing at a CAGR of 6.21% during the forecast period (2025-2030).

The various advantages of using specialty fertilizers over conventional fertilizers is expected to bolster the growth of the market

- In 2022, controlled-release fertilizers (CRFs) held a 7.4% share of the specialty fertilizer market. The steady growth of CRFs can be attributed to their distinct advantages over traditional fertilizers and the increasing awareness of efficient agricultural practices. CRFs gradually release nutrients over an extended period, ensuring a consistent nutrient supply to plants. This not only reduces nutrient wastage but also minimizes the risk of leaching or evaporation, which is common with conventional fertilizers.

- Water-soluble fertilizers, with a 47.8% market share, ranked second in the specialty fertilizer market in 2022. The use of water-soluble fertilizers has shown potential in reducing both water and fertilizer requirements for cultivating healthy plants.

- The liquid fertilizer market is poised for growth, propelled by advancements in irrigation systems and the rising adoption of advanced cultivation techniques such as hydroponics and aquaponics. The market value of liquid fertilizers is projected to witness a CAGR of 5.8% during 2023-2030.

- The adoption of slow-release fertilizers offers farmers not only economic benefits but also environmental advantages, such as water conservation, prevention of nitrogen volatilization and leaching, and reduced labor in fertilizer handling. These factors are expected to drive a 5.4% growth in the market value of slow-release fertilizers during 2023-20230.

- Given the benefits of specialty fertilizers, including precise nutrient release, reduced application rates, and economic advantages for farmers, the specialty fertilizer market is poised for growth in the coming years.

Government initiatives and farmers' focus on increasing productivity are expected to bolster the growth of the market

- In 2022, Nigeria held a commanding 27.0% value share in the African specialty fertilizer market. The country's agricultural sector, while facing challenges such as complex land tenure issues, inadequate irrigation infrastructure, the adverse effects of climate change, and the gradual adoption of cutting-edge agricultural technologies, has seen growth in the market supported by government initiatives. These include the Agriculture Promotion Policy (APP), the Nigeria-Africa Trade and Investment Promotion Programme, the National Agricultural Technology and Innovation Plan (NATIP), and the Anchor Borrowers Program (ABP), all of which have been instrumental in enhancing agricultural productivity.

- South Africa distinguishes itself as the continent's most advanced, productive, and diverse agricultural region. In 2022, its robust agricultural sector held a substantial 37.0% share of the total African specialty fertilizer market. The market is expected to record a CAGR of 6.7% during forecast period. This anticipated growth is largely due to the increasing need to mitigate the effects of climate-related risks, such as prolonged droughts and intense heat waves, by adopting more efficient fertilizer solutions.

- The African specialty fertilizer market is set to expand, driven by a rapidly growing population, the diminishing availability of arable land, the urgent necessity to improve yields on existing farmland, and concerted efforts to enhance agricultural productivity across the region. Thus, the market is forecasted to witness a CAGR of 6.0% from 2023 to 2030.

Africa Specialty Fertilizer Market Trends

The rising domestic demand will lead to double the agricultural production in the near future

- The agro-ecological zones in Africa span from dense rainforests with bi-annual rainfall to arid deserts with minimal precipitation. Key field crops in the region include corn, sorghum, wheat, and rice. In 2022, the cultivation area for these crops reached 224.8 million hectares, accounting for over 95% of the region's agricultural land. In response to a surplus of corn stocks leading to price suppression, South African corn farmers scaled back their planting by 10% to 2.1 million hectares in the 2018-19 season. Consequently, corn production in the country dipped by 11% from 13 million to 12 million tonnes, and exports fell from 2.5 million to 1 million tonnes. This shift prompted producers to allocate more of their fields to oilseed crops, particularly soybeans, resulting in an overall decline in corn cultivation across Africa in 2018-2019.

- Nigeria takes the lead as the largest sorghum producer in Africa, closely followed by Ethiopia. Sorghum, accounting for 50% of the total cereal output, dominates about 45% of Nigeria's cereal crop land. Known for its drought and waterlogging tolerance, sorghum thrives in diverse soil conditions. These attributes position sorghum as the go-to staple crop in Africa's drier regions, ensuring both food and income security.

- Kenya, Somalia, and significant parts of Ethiopia are grappling with the looming specter of severe food shortages. Over the past decade, Africa's spending on food imports has nearly tripled, even as its agricultural industry and cultivated land have continued to expand.

Rapeseed is the highest nitrogen consuming crop

- Rapeseed crops have the highest potassium and phosphorous application rates, accounting for 162.4 kg/hectare and 281.7 kg/hectare, respectively. Meanwhile, the average nitrogen application rate for field crops in Africa stands at 364.9 kg/hectare. In 2022, field crops in Africa accounted for 87.1% of the total primary nutrient consumption, which amounted to 556.1 thousand metric tons. This dominance can be attributed to the extensive land area dedicated to field crops. Specifically, the average nutrient application rates for nitrogen, phosphorous, and potassium in these crops were 223.2 kg/ha, 125.3 kg/ha, and 155.3 kg/ha, respectively.

- The Guinea savannas in Nigeria offer favorable environmental conditions for maize production. However, despite this potential, farmers in the region struggle with low yields. The primary culprits are soil degradation and nutrient depletion, primarily nitrogen, resulting from intensified land use. Field crops prioritize nitrogen application due to its multiple benefits, including promoting tillering, leaf area development, grain formation, filling, and protein synthesis. Nitrogen also plays a crucial role in enhancing both grain yield and quality.

- Given that primary nutrients are vital for crop growth and with concerns over soil depletion and nitrogen leaching, the application rates for primary nutrients are expected to witness significant growth in the coming years.

Africa Specialty Fertilizer Industry Overview

The Africa Specialty Fertilizer Market is fragmented, with the top five companies occupying 29.76%. The major players in this market are ICL Group Ltd, K+S Aktiengesellschaft, Kynoch Fertilizer, UPL Limited and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Speciality Type

- 5.1.1 CRF

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 SRF

- 5.1.4 Water Soluble

- 5.1.1 CRF

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Country

- 5.4.1 Nigeria

- 5.4.2 South Africa

- 5.4.3 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Gavilon South Africa (MacroSource, LLC)

- 6.4.2 Haifa Group

- 6.4.3 ICL Group Ltd

- 6.4.4 K+S Aktiengesellschaft

- 6.4.5 Kynoch Fertilizer

- 6.4.6 UPL Limited

- 6.4.7 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

特种肥料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

特种肥料:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球特种肥料市场规模、份额、趋势和成长分析报告(2026-2034)

全球特种肥料市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球特种肥料市场报告

2026年全球特种肥料市场报告 特种肥料市场规模、份额和成长分析(按类型、技术、形态、作物类型、应用方法和地区划分)-2026-2033年产业预测

特种肥料市场规模、份额和成长分析(按类型、技术、形态、作物类型、应用方法和地区划分)-2026-2033年产业预测 按养分类型、应用、形态、作物类型、作用机制和销售管道的晶体肥料市场—2025-2032年全球预测特种肥料市场(依作物类型、产品形态、营养类型、施用方法、通路和最终用途)-2025-2032 年全球预测

按养分类型、应用、形态、作物类型、作用机制和销售管道的晶体肥料市场—2025-2032年全球预测特种肥料市场(依作物类型、产品形态、营养类型、施用方法、通路和最终用途)-2025-2032 年全球预测 特种肥料市场规模、份额、趋势分析报告:按技术、作物类型、应用、地区、细分市场预测,2025-2030 年全球特种肥料市场规模(依特种肥料类型、作物类型、施用方法、区域范围及预测)

特种肥料市场规模、份额、趋势分析报告:按技术、作物类型、应用、地区、细分市场预测,2025-2030 年全球特种肥料市场规模(依特种肥料类型、作物类型、施用方法、区域范围及预测) 特种肥料市场 - 全球产业规模、份额、趋势、机会和预测,按作物类型、形式、应用方式、技术、地区和竞争细分,2020-2030 年中东和非洲特种肥料:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)

特种肥料市场 - 全球产业规模、份额、趋势、机会和预测,按作物类型、形式、应用方式、技术、地区和竞争细分,2020-2030 年中东和非洲特种肥料:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)

▼