|

市场调查报告书

商品编码

1939061

数位电子看板:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Digital Signage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

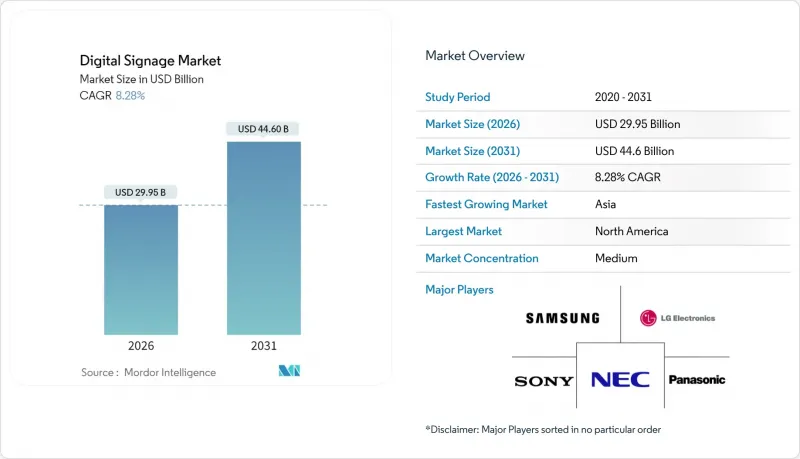

数位电子看板市场预计到 2026 年价值 299.5 亿美元,高于 2025 年的 276.6 亿美元,预计到 2031 年将达到 446 亿美元。

预计2026年至2031年年复合成长率(CAGR)为8.28%。

这一成长得益于人工智慧驱动的内容引擎的广泛应用、5G边缘网路的部署以及节能型微型LED萤幕的普及。大型企业正在利用互联显示器统一混合办公环境中的通信,而市政当局则将互动式电子白板融入智慧城市基础设施,以提高交通出行和公共倡议的效率。随着受众分析平台将商店萤幕转化为创收的零售媒体资产,零售商正在加大投资。同时,交通运营商正在部署即时乘客资讯系统以提升服务品质。

全球数位电子看板市场趋势与洞察

人工智慧驱动的受众分析推动动态内容个人化

零售商正逐渐摒弃千篇一律的循环显示,转而采用人工智慧引擎,根据消费者的接近即时调整讯息。电脑视觉模组能够测量年龄层、性别和停留时间,从而触发创新变化,转换率可望提升高达 30%。美国、英国、德国和法国的连锁零售商正利用这些洞察,结合会员应用程式数据,打造全通路宣传活动。广告代理商愿意为这种精准曝光支付高额的 CPM,将门市网路转化为高利润的媒体管道。儘管 GDPR 合规性正在影响欧洲的部署速度,但供应商正在采用「隐私纳入设计」工作流程,在分析前对影片帧进行本地匿名化处理。这些因素正推动数位电子看板市场在中期内保持强劲成长动能。

利用 5G 和边缘运算实现户外即时串流传输

东京、首尔、新加坡和雪梨的交通部门正在利用毫米波5G骨干网,为户外LED显示器提供超低延迟的影片和紧急警报。板载边缘伺服器预先快取高解析度影片片段,从而降低资料传输成本,并可根据交通感测器的峰值变化即时调整宣传活动内容。亚洲交通枢纽的研究表明,当5G取代传统光纤时,生产力可提高52%至245%,成本节省高达90%。随着更多大都会地区部署独立的5G核心网,数位电子看板市场必将迎来蓬勃发展。

内容管理系统(CMS)标准分散化,导致多个供应商之间的互通性变得复杂。

全球零售商通常经营多个品牌的萤幕,但目前尚无通用的调度或分析通讯协定。电讯(ITU) 警告称,缺乏互通性会减缓技术普及速度并增加整体拥有成本。这迫使许多公司依赖单一供应商生态系统,限制了竞争性竞标。产业组织正在努力开发应用程式介面 (API),但由于各供应商的蓝图不同,进展缓慢。这种情况限制了数位电子看板市场短期内的扩充性。

细分市场分析

到2025年,电视墙将占据27.65%的收入份额,凭藉其在控制室和旗舰店中营造的沉浸式效果,继续保持主导地位。数位电子看板市场持续强调品牌剧院和企业大会等活动的规模需求。快餐店对数位海报的需求也保持稳定,因为加盟商优先考虑的是易于更新的内容。

另一方面,随着消费者接受自助结帐系统、导航和会员註册,自助服务终端预计到2031年将以9.1%的复合年增长率快速成长。数位电子看板市场的零售商正在部署人工智慧模组,以便在结帐时推荐其他产品,从而提高平均购买价值。透明液晶显示器在奢侈品商店和汽车展示室中占据了一席之地,将产品展示与数据迭加相结合。製造商目前正在尝试为交通枢纽开发混合型设备,将多面板电视墙与自助服务终端互动结合。

到2025年,硬体组件将占总收入的60.12%,并将继续构成数位电子看板市场的基础,其中包括LED显示器、媒体播放机和安装套件。像素成本的下降将使资本支出在4-5年的更新週期内保持在可控范围内。

随着企业意识到内容编配与分析能够提升投资报酬率,软体收入正以10.39%的复合年增长率(两位数)成长。云端仪錶板透过远距离诊断确保设备运作,人工智慧调度器提升宣传活动的针对性,供应商正在整合播放证明帐本,使广告主能够审核曝光情况,从而增强了数位电子看板市场的信心。

区域分析

到2025年,北美将占全球营收的33.08%,这主要得益于美国企业升级改造,将大厅转型为数位展示空间。加拿大零售商正在加速收银系统的现代化,从而稳定了区域需求。该地区的数位电子看板市场受益于成熟的云端基础设施,降低了采用门槛。

亚太地区正以8.42%的复合年增长率成长,这主要得益于中国的城市丛集计划、日本的技术出口热潮、印度的购物中心蓬勃发展以及东南亚旅游业的復苏。面板和积体电路的一体化供应链正在降低单价,为该地区的买家提供了定价空间,并促进了数位电子看板市场的渗透。

受生态设计法规和强劲购买力的推动,欧洲市场正保持稳定成长。儘管历史街区的标誌限制增加了合规负担,但德国和斯堪的纳维亚半岛的企业正在采用节能的A级显示屏,以应对旅游目的地增长停滞的局面。东欧机场正竞相利用身临其境型资讯墙来巩固其枢纽地位,数位电子看板市场向东扩张。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 人工智慧驱动的受众分析技术,协助北美及欧洲零售商店及交通走廊实现动态内容个人化。

- 5G和边缘运算技术使亚洲和大洋洲主要交通枢纽的户外即时串流播放成为可能。

- 欧盟企业永续性指令加速节能型微型LED和电子纸牌的普及

- 疫情后混合办公模式推动美国企业采用云端为基础的通讯仪錶板

- 在中东地区整合大型数位广告看板的大型智慧计划(NEOM,杜拜 2040)

- 零售媒体商业化战略推动拉丁美洲大型大众零售连锁店采用电视墙

- 市场限制

- 内容管理系统(CMS)标准分散化,使全球零售商的多供应商互通性变得复杂。

- 欧洲历史城区户外LED建筑幕墙建设面临高额的资本投资与审核障碍

- 美国公共运输显示器遭勒索软体攻击,凸显网路安全漏洞

- 用于大型面板的专用驱动积体电路的供应链价格正在上涨。

- 产业生态系分析

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 电视墙

- 视讯萤幕

- 亭

- 透明液晶萤幕

- 数位海报

- 广告看板

- 其他类型

- 按组件

- 硬体

- LCD/LED显示器

- 有机发光二极体显示器

- 微型LED显示器

- 媒体播放机

- 控制器

- 投影机/投影幕

- 其他硬体

- 软体

- 服务

- 安装与集成

- 託管服务

- 支援与维护

- 硬体

- 透过部署

- 本地部署

- 基于云端的

- 杂交种

- 按萤幕尺寸

- 小于 32 英寸

- 32英寸至52英寸

- 52吋或以上

- 超大尺寸,100吋或更大

- 按位置

- 店内/室内

- 户外的

- 按最终用途行业划分

- 零售

- 运输

- 饭店业

- 公司

- 教育

- 卫生保健

- 政府

- 体育娱乐

- 银行和金融服务

- 製造工厂

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 其他南美洲

- 亚太地区

- 中国

- 日本

- 印度

- 东南亚

- 亚太其他地区

- 中东和非洲

- 中东

- GCC

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- NEC Display Solutions Ltd.

- LG Display Co. Ltd.

- Samsung Electronics Co. Ltd.

- Panasonic Corporation

- Sony Group Corporation

- Stratacache

- Planar Systems Inc.

- Hitachi Ltd.

- Barco NV

- Goodview

- Cisco Systems Inc.

- Scala Inc.

- Broadsign International LLC

- Appspace Inc.

- BrightSign LLC

- Mvix Inc.

- Christie Digital Systems USA Inc.

- Daktronics Inc.

- Leyard Optoelectronic Co. Ltd.

- Unilumin Group Co. Ltd.

- JCDecaux SA

- E Ink Holdings Inc.

- Clear Channel Outdoor Holdings Inc.

- Sharp Corporation

第七章 市场机会与未来展望

Digital signage market size in 2026 is estimated at USD 29.95 billion, growing from 2025 value of USD 27.66 billion with 2031 projections showing USD 44.6 billion, growing at 8.28% CAGR over 2026-2031.

Consistent uptake of AI-driven content engines, 5G-enabled edge networks and energy-frugal MicroLED screens underpins this expansion. Large enterprises are using connected displays to unify communications across hybrid workplaces, while city authorities weave interactive boards into smart-city infrastructure to streamline mobility and public safety initiatives. Retailers intensify investment as audience-analytics platforms transform in-store screens into revenue-generating retail-media assets. At the same time, transportation operators deploy real-time passenger information systems that raise service quality.

Global Digital Signage Market Trends and Insights

AI-powered audience analytics boosting dynamic content personalisation

Retailers now replace one-size-fits-all loops with AI engines that adjust messaging in real time when shoppers approach. Computer-vision modules gauge age bracket, gender and engagement length, then trigger creative variants that can lift conversion by as much as 30%. Chains in the United States, United Kingdom, Germany and France link these insights with loyalty-app data to enrich omnichannel campaigns. Agencies pay premium CPMs for such precise exposure, turning store networks into high-margin media channels. Compliance with GDPR shapes rollout pace in Europe, yet vendors embed privacy-by-design workflows that anonymise video frames locally before analysis. These factors keep the digital signage market on a solid medium-term growth path.

5G + edge computing enabling real-time outdoor streaming

Transit authorities in Tokyo, Seoul, Singapore and Sydney use millimetre-wave 5G backbones to push ultra-low-latency video and emergency alerts to outdoor LED boards. On-device edge servers pre-cache high-resolution clips, cutting data transit cost and letting campaigns switch instantly when foot-traffic sensors spike. Studies for Asian transport hubs show productivity gains from 52% to 245% and cost savings up to 90% when 5G replaces legacy fibre. As more metros activate standalone 5G cores, the digital signage market receives an immediate uplift.

Fragmented CMS standards complicating multi-vendor interoperability

Global retailers often juggle screens from several brands yet find no common protocol for scheduling or analytics. The International Telecommunication Union warns that the lack of interoperability slows deployments and raises total ownership cost. Many firms therefore lock into single-vendor ecosystems, limiting competitive bids. Industry alliances are drafting APIs, but diverging roadmaps among vendors keep progress slow. This reality curbs near-term scalability for the digital signage market.

Other drivers and restraints analyzed in the detailed report include:

- EU corporate sustainability mandates accelerating energy-efficient displays

- Post-pandemic hybrid work models driving cloud dashboards

- Cyber-security vulnerabilities spotlighted by ransomware on transit displays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Video walls dominated 2025 revenue with 27.65% share due to their immersive impact in control rooms and flagship retail settings. The digital signage market continues to favour their scale for brand theatre and corporate town-hall events. Demand also stays steady for digital posters in quick-serve restaurants because franchisees value simple content swaps.

Kiosks, however, offer the fastest 9.1% CAGR to 2031 as shoppers embrace self-checkout, wayfinding and loyalty enrollment on responsive touchscreens. Retailers in the digital signage market deploy AI modules that recommend add-ons at check-out, nudging ticket size. Transparent LCD enclosures carve a niche in luxury stores and automotive showrooms, merging product visibility with data overlays. Manufacturers now experiment with hybrid rigs that fuse multi-panel video walls and kiosk interaction for transit concourses.

Hardware parts generated 60.12% of 2025 turnover and remain foundational to the digital signage market, covering LED tiles, media players and mounting kits. Falling pixel costs keep capex manageable for refresh cycles every four-to-five years.

Software revenue is growing at a double-digit 10.39% CAGR as companies discover that content orchestration and analytics drive ROI. Cloud dashboards secure fleet uptime through remote diagnostics, while AI schedulers improve campaign relevance. Vendors integrate proof-of-play ledgers so advertisers can audit exposures, raising confidence in the digital signage market.

The Digital Signage Market Report is Segmented by Type (Video Wall, Video Screen, Kiosk, and More), Component (Hardware, Software, and Services), Deployment (On-Premise, Cloud-Based, and Hybrid), Screen Size (Below 32", 32"-52", and More), Location (In-store/Indoor, and Outdoor), End-Use Industry (Retail, Transportation, Hospitality, Corporate, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 33.08% 2025 income, anchored by United States corporate refurbishments that turned lobbies into digital-first showcases. Canadian retailers accelerate checkout modernisation, keeping regional demand steady. The digital signage market here benefits from mature cloud infrastructure that reduces deployment friction.

Asia-Pacific is on an 8.42% CAGR trajectory, propelled by China's city cluster projects, Japan's technology export push, India's mall boom and Southeast Asia's tourism recovery. An integrated supply chain for panels and ICs lowers unit costs, giving regional buyers price latitude that boosts the digital signage market's penetration.

Europe records stable gains supported by ecodesign mandates and high purchasing power. Historic-district signage caps add compliance effort, yet German and Nordic corporates adopt energy-class A displays, offsetting tourist-zone pauses. Eastern European airports compete for hub status through immersive wayfinding walls, expanding the digital signage market eastward.

- NEC Display Solutions Ltd.

- LG Display Co. Ltd.

- Samsung Electronics Co. Ltd.

- Panasonic Corporation

- Sony Group Corporation

- Stratacache

- Planar Systems Inc.

- Hitachi Ltd.

- Barco NV

- Goodview

- Cisco Systems Inc.

- Scala Inc.

- Broadsign International LLC

- Appspace Inc.

- BrightSign LLC

- Mvix Inc.

- Christie Digital Systems USA Inc.

- Daktronics Inc.

- Leyard Optoelectronic Co. Ltd.

- Unilumin Group Co. Ltd.

- JCDecaux SA

- E Ink Holdings Inc.

- Clear Channel Outdoor Holdings Inc.

- Sharp Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-powered audience analytics boosting dynamic content personalisation in North American and European retail and transit corridors

- 4.2.2 5G + edge computing enabling real-time outdoor streaming across major Asian and Oceanian transport hubs

- 4.2.3 EU corporate sustainability mandates accelerating adoption of energy-efficient MicroLED and e-paper signage

- 4.2.4 Post-pandemic hybrid work models driving cloud-based corporate communication dashboards in the USA

- 4.2.5 Smart-city mega-projects (NEOM, Dubai 2040) integrating large-format digital billboards across the Middle East

- 4.2.6 Retail-media monetisation strategies fuelling video-wall roll-outs by Latin-American big-box chains

- 4.3 Market Restraints

- 4.3.1 Fragmented CMS standards complicating multi-vendor interoperability for global retailers

- 4.3.2 High CAPEX and permitting hurdles for outdoor LED facades in historical European city centres

- 4.3.3 Cyber-security vulnerabilities spotlighted by ransomware on United States transit displays

- 4.3.4 Supply-chain price spikes in specialty driver-ICs for large panels

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Type

- 5.1.1 Video Wall

- 5.1.2 Video Screen

- 5.1.3 Kiosk

- 5.1.4 Transparent LCD Screen

- 5.1.5 Digital Poster

- 5.1.6 Billboard

- 5.1.7 Other Types

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.1.1 LCD/LED Display

- 5.2.1.2 OLED Display

- 5.2.1.3 MicroLED Display

- 5.2.1.4 Media Players

- 5.2.1.5 Controllers

- 5.2.1.6 Projector/Projection Screens

- 5.2.1.7 Other Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.2.3.1 Installation and Integration

- 5.2.3.2 Managed Services

- 5.2.3.3 Support and Maintenance

- 5.2.1 Hardware

- 5.3 By Deployment

- 5.3.1 On-premise

- 5.3.2 Cloud-based

- 5.3.3 Hybrid

- 5.4 By Screen Size

- 5.4.1 Below 32"

- 5.4.2 32"-52"

- 5.4.3 Above 52"

- 5.4.4 Ultra-large Above 100"

- 5.5 By Location

- 5.5.1 In-store/Indoor

- 5.5.2 Outdoor

- 5.6 By End-use Industry

- 5.6.1 Retail

- 5.6.2 Transportation

- 5.6.3 Hospitality

- 5.6.4 Corporate

- 5.6.5 Education

- 5.6.6 Healthcare

- 5.6.7 Government

- 5.6.8 Sports and Entertainment

- 5.6.9 Banking and Financial Services

- 5.6.10 Manufacturing Facilities

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Nordics

- 5.7.2.5 Rest of Europe

- 5.7.3 South America

- 5.7.3.1 Brazil

- 5.7.3.2 Rest of South America

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South-East Asia

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Gulf Cooperation Council Countries

- 5.7.5.1.2 Turkey

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 NEC Display Solutions Ltd.

- 6.4.2 LG Display Co. Ltd.

- 6.4.3 Samsung Electronics Co. Ltd.

- 6.4.4 Panasonic Corporation

- 6.4.5 Sony Group Corporation

- 6.4.6 Stratacache

- 6.4.7 Planar Systems Inc.

- 6.4.8 Hitachi Ltd.

- 6.4.9 Barco NV

- 6.4.10 Goodview

- 6.4.11 Cisco Systems Inc.

- 6.4.12 Scala Inc.

- 6.4.13 Broadsign International LLC

- 6.4.14 Appspace Inc.

- 6.4.15 BrightSign LLC

- 6.4.16 Mvix Inc.

- 6.4.17 Christie Digital Systems USA Inc.

- 6.4.18 Daktronics Inc.

- 6.4.19 Leyard Optoelectronic Co. Ltd.

- 6.4.20 Unilumin Group Co. Ltd.

- 6.4.21 JCDecaux SA

- 6.4.22 E Ink Holdings Inc.

- 6.4.23 Clear Channel Outdoor Holdings Inc.

- 6.4.24 Sharp Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

数位电子看板市场规模、份额、趋势及预测(按类型、组件、技术、应用、位置、规模和地区划分),2026-2034年

数位电子看板市场规模、份额、趋势及预测(按类型、组件、技术、应用、位置、规模和地区划分),2026-2034年 2026年全球数位侧窗显示器市场报告

2026年全球数位侧窗显示器市场报告 2026-2030年全球数位电子看板市场

2026-2030年全球数位电子看板市场 商用大型指示牌市场按技术、安装方式、萤幕大小、触控功能和应用划分-全球预测(2026-2032 年)投影数位电子看板看板市场:按组件、连接方式、安装类型、显示类型、应用和最终用户划分,全球预测,2026-2032年织物标牌市场:按织物类型、印刷技术、应用、终端用户产业和分销管道划分-2026-2032年全球预测

商用大型指示牌市场按技术、安装方式、萤幕大小、触控功能和应用划分-全球预测(2026-2032 年)投影数位电子看板看板市场:按组件、连接方式、安装类型、显示类型、应用和最终用户划分,全球预测,2026-2032年织物标牌市场:按织物类型、印刷技术、应用、终端用户产业和分销管道划分-2026-2032年全球预测 欧洲数位电子看板市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

欧洲数位电子看板市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 工业显示系统市场规模、份额和成长分析(按显示类型、面板尺寸、技术/功能、最终用途产业和地区划分)-2026-2033年产业预测

工业显示系统市场规模、份额和成长分析(按显示类型、面板尺寸、技术/功能、最终用途产业和地区划分)-2026-2033年产业预测 数位看板市场按类型、应用、最终用户产业、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测日本数位电子看板市场报告:按类型、组件、技术、应用、安装位置、规模和地区划分(2026-2034 年)

数位看板市场按类型、应用、最终用户产业、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测日本数位电子看板市场报告:按类型、组件、技术、应用、安装位置、规模和地区划分(2026-2034 年)