|

市场调查报告书

商品编码

1906978

设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

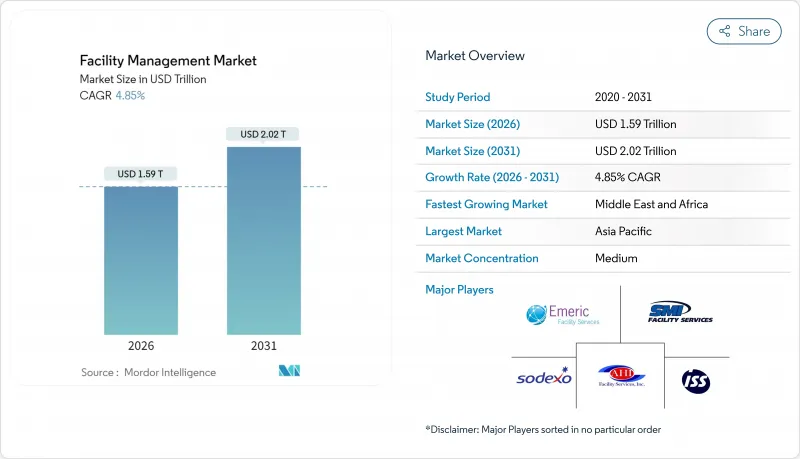

预计到 2026 年,设施管理市场规模将达到 1.59 兆美元,较 2025 年的 1.517 兆美元持续成长。预计到 2031 年,该市场规模将达到 2.02 兆美元,2026 年至 2031 年的复合年增长率为 4.85%。

这种成长动能反映了设施管理定位的转变,它不再只是支持成本,而是成为提升营运韧性、数位整合和员工生产力的策略槓桿。不断增长的外包需求、儘管网路安全事件频繁但仍在加速的云端迁移,以及对环境、社会和治理(ESG)要求的日益重视,共同推动了潜在需求的扩大。新兴市场(尤其是亚太地区)不断增长的基础设施投资,进一步强化了设施管理市场的多区域扩张週期。那些将技术平台与基于结果的模式相结合的供应商,正赢得那些寻求透明成本管理和可衡量效率的客户的高价值合约。

全球设施管理市场趋势与洞察

越来越重视将非核心职能外包

企业正将设施管理业务外包给专业合作伙伴,从而释放资金用于核心创新。到2024年,35%的企业将增加设施管理预算,以降低营运复杂性。设施管理市场受益于规模经济,能够有效应对供应链中断,并提供多元化的员工。科技和医疗保健产业的需求尤其显着,支撑了世邦魏理仕(CBRE) 2025年第一季收入净额成长16%的预期。这种模式也有助于降低供应商风险(29%的企业表示担忧供应中断),促使企业更倾向选择物流能力较强的设施管理伙伴。随着外包业务量的成长,供应商正将利润再投资于自动化、预测分析和员工技能提升,强化了设施管理市场良性成长的循环。

利用物联网进行预测性维护,实现设施数位化。

预测性维护平台预计到2025年将达到55亿美元,年增长率达17%,并将推动从被动维修转向基于状态的管理模式的结构性转变。医疗保健产业的部署报告显示,透过自动产生工单,设施成本降低了10-15%。软体层(占支出的44%)整合了预训练演算法,使中型设施也能在设施管理市场普及应用。一项在工业工厂进行的初步试点计画表明,废热回收率提高了25%,展现了切实的ESG(环境、社会和治理)效益。随着异常检测模型的日趋成熟,资料需求不断降低,使得小规模资产无需庞大的历史日誌即可参与其中,从而扩大了市场渗透率,涵盖更广泛的地区。

设施管理职的薪资上涨

预计到2024年,设施管理职缺的平均时薪将成长4.1%,中位数达到21.74美元。这将对劳动密集型合约的利润率造成压力。熟练工种(尤其是暖通空调和电气工种)的短缺加剧了竞标竞争,而康乃尔大学设施管理工人罢工等事件也凸显了工会活动的活性化。隐性合约费用和后端附加费进一步加重了预算压力,迫使采购负责人重新评估外包的经济效益。为此,供应商正在加速采用机器人技术和自主清洁系统,但初始投资和再培训要求阻碍了这些技术在设施管理市场的短期普及。

细分市场分析

受机械、电气和管道 (MEP) 设备强制维护以确保资产完整性的驱动,硬性服务将在 2025 年占据设施管理市场规模的 58.65%。日益严格的监管标准和资产复杂性正在推动对认证技术人员需求的稳定成长。在预测期内,客户对整合管理体验的日益青睐将推动其与软性服务的进一步整合,从而为整合供应商创造交叉销售机会。

儘管软性服务规模较小,但其复合年增长率高达6.05%,反映出企业日益关注卫生、安全和居住者福祉。清洁合约中已包含抗菌通讯协定和机器人吸尘器,而安保也正朝着人工智慧影像分析的方向发展。随着ESG(环境、社会和治理)标准扩展至室内空气品质和餐饮永续性,软性服务正逐渐获得经营团队的认可。能够整合硬性数据和软性数据的供应商可以主动调整预防性维护计划,从而带来实际的营运效益,并提升其在设施管理市场的份额。

截至2025年,以明确责任的综合设施管理(IFM)合约为支撑的内部管理模式将占据设施管理市场份额的53.20%。拥有多个办公地点的公司重视单一发票的透明度,并正在推动这种模式的普及。同时,随着网路安全敏感型产业保留关键的管理职能,外包设施管理将以5.71%的复合年增长率成长。混合型结构正变得越来越普遍,它透过将策略规划保留在公司内部,而将现场执行工作转移给合作伙伴,从而在柔软性和风险之间取得平衡。

随着综合设施管理(IFM)范围的扩大,供应商正在整合分析门户,以可视化方式呈现按地点分類的服务成本,从而实现数据驱动的合约续约。由于客户要求提供整体价值提案,单一服务选项正在减少,迫使规模较小的承包商进行合併或专业转型。世邦魏理仕(CBRE)以16亿美元收购Industrious,凸显了其向体验式订阅服务的战略转型,该服务整合了设施管理、酒店服务和空间分析,重新定义了设施管理市场的竞争格局。

区域分析

预计到2025年,亚太地区将占据全球设施管理市场41.10%的份额,年复合成长率达6.05%,主要得益于政府的奖励策略和都市区进程。中国高达51.4兆美元的固定资产投资,其中包括基础设施投资成长5.9%,将支持对设施管理服务的长期需求。印度商业房地产的快速扩张正在推动远端监控的需求,而东协的智慧城市规划也正在将设施管理合约纳入其总体规划。能够建立本地化供应链和多语言平台的营运商将获得先发优势。

北美市场环境依然成熟且充满创新活力,云端运算的普及和ESG合规性推动了高端定价。该地区的设施管理市场面临劳动力短缺,促使自动化技术得到应用。能源优化要求和控制通膨的立法奖励正在推动设施管理专业人员进行维修。欧洲也在数位化进程中不断前进,但其特点是严格的碳排放法规,例如欧盟环境影响评估指令(EPBD),并且合约正朝着基于绩效的补偿模式发展。泛欧供应商正在利用跨境管治框架来规范服务品质。

在中东和非洲,公私合营在交通、医疗和教育基础设施领域的应用正在加速普及。波湾合作理事会(GCC)的大型企划从设计阶段开始纳入设施管理(FM)条款,从而提升了专案的全生命週期价值。在南美洲,物流和製造业的扩张推动了稳定的需求,但汇率波动也带来了弹性价格设定的需求。在所有新兴地区,供应商分散化正在推动产业整合,这为擅长併购整合的全球巨头扩大了设施管理市场。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 越来越重视非核心职能的外包

- 利用物联网进行预测性维护,实现设施数位化。

- 永续性和ESG相关设施管理合约

- 疫情后混合职场重新设计的必要性

- 新兴市场的公私合营基础建设项目

- 人工智慧主导的能源优化要求

- 市场限制

- 行政工作工资上涨

- 在新兴市场实现供应商基础多元化

- 基于云端的设施管理平台中的网路安全风险

- 中小企业IFM平台的资本固定

- 价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 定价分析

- 对宏观经济趋势的市场评估

第五章 市场规模与成长预测

- 按服务类型

- 硬服务

- 资产管理

- 机电及暖通空调

- 防火和安全措施

- 其他硬体服务

- 软服务

- 打扫

- 安全和办公支持

- 餐饮

- 其他软体服务

- 硬服务

- 按规定表格

- 内部

- 外包

- 单服务调频广播

- Bundle FM

- 综合设施管理(IFM)

- 按部署模式

- 本地部署

- 基于云端的

- 按公司规模

- 大公司

- 中小企业

- 按最终用户行业划分

- 商业设施(IT/通讯、零售、仓储)

- 饭店餐饮业(饭店、餐厅)

- 公共机构和公共

- 卫生保健

- 工业与流程

- 住宅和休閒

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- 北欧国家(瑞典、挪威、丹麦、芬兰)

- 波兰

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 智利

- 其他南美洲

- 中东和非洲

- 中东

- 海湾合作委员会(沙乌地阿拉伯、阿联酋、卡达、阿曼、科威特、巴林)

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 肯亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- CBRE Group Inc.

- Cushman and Wakefield plc

- JLL(Jones Lang LaSalle Inc.)

- ISS A/S

- Sodexo SA

- Compass Group plc

- Emeric Facility Services

- SMI Facility Services

- AHI Facility Services Inc.

- Aramark Corporation

- ABM Industries Inc.

- G4S Limited

- Atalian Global Services

- Vinci Facilities(VINCI SA)

- EMCOR Group Inc.

- Comfort Systems USA

- Balfour Beatty-Workplace

- Serco Group plc

- Reliance Facilities(India)

- Sinopec Engineering FM(China)

- Unispace Global

第七章 市场机会与未来展望

facility management market size in 2026 is estimated at USD 1.59 trillion, growing from 2025 value of USD 1.517 trillion with 2031 projections showing USD 2.02 trillion, growing at 4.85% CAGR over 2026-2031.

Growth momentum reflects the repositioning of facility management from a support cost to a strategic lever for operational resilience, digital integration, and employee productivity. Heightened outsourcing appetite, rapid cloud migration despite cybersecurity incidents, and the steady pull of ESG mandates are collectively widening addressable demand. Rising infrastructure spending in emerging markets, particularly Asia-Pacific, is reinforcing a multi-regional expansion cycle for the facility management market. Providers that blend technology platforms with outcome-based models are capturing premium contracts as clients seek transparent cost control and measurable efficiency.

Global Facility Management Market Trends and Insights

Growing emphasis on outsourcing non-core operations

Corporations are channeling capital toward core innovation by transferring facilities responsibilities to specialist partners, with 35% of enterprises boosting FM budgets in 2024 to curb operational complexity. The facility management market is benefiting from scale effects that let providers absorb supply-chain shocks and provide diversified labor pools. Demand is pronounced in technology and healthcare, supporting CBRE's 16% net revenue rise from facilities contracts during Q1 2025. The practice also mitigates supplier-risk exposure-29% of firms flagged disruption fears-fueling preference for FM partners with fortified logistics. As outsourcing volume mounts, providers are reinvesting margin gains into automation, predictive analytics, and workforce upskilling, reinforcing a virtuous growth cycle across the facility management market.

Facility digitisation via IoT-enabled predictive maintenance

Predictive maintenance platforms worth USD 5.5 billion in 2025 and expanding 17% annually underpin a structural shift from reactive repairs to condition-based care. Healthcare adopters report 10-15% facility cost savings through automated work-order generation. The software layer-44% of spend-packages pre-trained algorithms that democratize access for midsize sites inside the facility management market. Early pilots in industrial plants reveal 25% faster waste-heat recovery, highlighting tangible ESG payoffs. As anomaly-detection models mature, data prerequisites shrink, enabling smaller assets to participate without dense historical logs, thereby broadening market penetration across geographies.

High wage inflation in custodial labour

Average hourly earnings in facilities support soared 4.1% in 2024, lifting median pay to USD 21.74 and compressing margins for labour-intensive contracts. Skilled-trade shortages, especially HVAC and electrical, intensify bidding wars, while events such as Cornell University's facilities-worker strike underscore rising union activism. Hidden contract fees and backend surcharges further strain budgets, pushing buyers to reconsider outsourcing economics. Providers respond by accelerating robotics and autonomous-cleaning pilots, but up-front capital and retraining requirements weigh on near-term adoption across the facility management market.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability and ESG-linked FM contracting

- Post-pandemic hybrid workplace re-design needs

- Fragmented vendor base in emerging markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard Services generated 58.65% of the facility management market size in 2025, buoyed by mandatory mechanical, electrical, and plumbing (MEP) maintenance that safeguards asset integrity. Regulatory codes and rising asset complexity necessitate certified technicians, reinforcing demand stability. Over the forecast horizon, convergence with Soft Services will intensify as clients seek unified experience management, creating cross-selling avenues for integrated vendors.

Soft Services, though smaller, accelerate at a 6.05% CAGR, reflecting heightened focus on hygiene, security, and occupant well-being. Cleaning contracts embed anti-microbial protocols and robotic vacuums, while security shifts toward AI video analytics. As ESG scorecards widen to include indoor air and catering sustainability, Soft Services gain board-level visibility. Providers that fuse Hard and Soft data streams can proactively adjust preventive schedules, creating tangible operational gains and broadening wallet share within the facility management market.

In-house models held 53.20% of the facility management market share in 2025, underpinned by integrated FM (IFM) contracts that streamline accountability. Multisite firms appreciate single-invoice transparency, propelling uptake. Simultaneously, Outsourcing FM expands 5.71% CAGR as cyber-sensitive industries retain critical controls. Hybrid structures are proliferating: strategic planning stays internal, while field execution shifts to partners, balancing flexibility and risk.

As IFM scope widens, vendors embed analytics portals that surface cost-to-serve by location, enabling data-driven renewals. Single-service options erode as clients insist on total-value propositions, nudging smaller contractors toward mergers or specialisation niches. CBRE's USD 1.6 billion Industrious acquisition underscores strategic re-positioning toward experiential subscriptions that bundle facilities, hospitality, and space analytics, thereby redefining competitive contours of the facility management market.

The Facility Management Market Report is Segmented by Service Type (Hard Services, and Soft Services), Offering Type (In-House, and Outsourced), Deployment Model (On-Premise, and Cloud-Based), Organisation Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Commercial, Hospitality, Institutional, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 41.10% of the facility management market in 2025 and is set to expand at a 6.05% CAGR, sustained by government stimulus and urban migration. China's USD 51.4 trillion fixed-asset push, including 5.9% growth in infrastructure placements, underpins long-run service pipelines. India's commercial real estate surge adds demand for remote monitoring, while ASEAN smart-city programs embed FM contracts into master planning stages. Providers scaling localized supply chains and multilingual platforms will gain early-mover advantage.

North America maintains a mature yet innovative landscape where cloud penetration and ESG compliance drive premium fees. The facility management market in the region contends with tight labor pools, spurring automation adoption. Energy-optimisation mandates and the Inflation Reduction Act's incentives incentivize retrofits managed by FM specialists. Europe exhibits similar digital sophistication but is distinguished by stringent carbon regulations such as EPBD, steering contracts toward performance-linked remuneration. Pan-European vendors leverage cross-border governance frameworks to standardise service quality.

The Middle East and Africa witness accelerating adoption through public-private partnerships in transport, healthcare, and education infrastructure. Gulf Cooperation Council megaprojects integrate FM provisions from the design stage, anchoring lifecycle value. South America experiences steady demand tied to logistics and manufacturing expansion, though currency volatility necessitates flexible pricing. Across all emerging regions, fragmented supplier landscapes encourage consolidation plays, broadening the facility management market for global majors adept at merger integration.

- CBRE Group Inc.

- Cushman and Wakefield plc

- JLL (Jones Lang LaSalle Inc.)

- ISS A/S

- Sodexo SA

- Compass Group plc

- Emeric Facility Services

- SMI Facility Services

- AHI Facility Services Inc.

- Aramark Corporation

- ABM Industries Inc.

- G4S Limited

- Atalian Global Services

- Vinci Facilities (VINCI SA)

- EMCOR Group Inc.

- Comfort Systems USA

- Balfour Beatty - Workplace

- Serco Group plc

- Reliance Facilities (India)

- Sinopec Engineering FM (China)

- Unispace Global

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing emphasis on outsourcing non-core operations

- 4.2.2 Facility digitisation via IoT-enabled predictive maintenance

- 4.2.3 Sustainability and ESG-linked FM contracting

- 4.2.4 Post-pandemic hybrid workplace re-design needs

- 4.2.5 Public-private infrastructure pipelines in EMs

- 4.2.6 AI-led energy optimisation mandates

- 4.3 Market Restraints

- 4.3.1 High wage inflation in custodial labour

- 4.3.2 Fragmented vendor base in emerging markets

- 4.3.3 Cyber-security risk in cloud-based FM platforms

- 4.3.4 Capital lock-in for IFM platforms among SMEs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Service Type

- 5.1.1 Hard Services

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC

- 5.1.1.3 Fire and Safety

- 5.1.1.4 Other Hard Services

- 5.1.2 Soft Services

- 5.1.2.1 Cleaning

- 5.1.2.2 Security and Office Support

- 5.1.2.3 Catering

- 5.1.2.4 Other Soft Services

- 5.1.1 Hard Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single-service FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM (IFM)

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud-Based

- 5.4 By Organisation Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By End-User Industry

- 5.5.1 Commercial (IT/Telecom, Retail, Warehouses)

- 5.5.2 Hospitality (Hotels, Restaurants)

- 5.5.3 Institutional and Public Infrastructure

- 5.5.4 Healthcare

- 5.5.5 Industrial and Process

- 5.5.6 Residential and Leisure

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Benelux (Belgium, Netherlands, Luxembourg)

- 5.6.2.7 Nordics (Sweden, Norway, Denmark, Finland)

- 5.6.2.8 Poland

- 5.6.2.9 Russia

- 5.6.2.10 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Chile

- 5.6.4.5 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 GCC (Saudi Arabia, UAE, Qatar, Oman, Kuwait, Bahrain)

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Kenya

- 5.6.5.2.5 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CBRE Group Inc.

- 6.4.2 Cushman and Wakefield plc

- 6.4.3 JLL (Jones Lang LaSalle Inc.)

- 6.4.4 ISS A/S

- 6.4.5 Sodexo SA

- 6.4.6 Compass Group plc

- 6.4.7 Emeric Facility Services

- 6.4.8 SMI Facility Services

- 6.4.9 AHI Facility Services Inc.

- 6.4.10 Aramark Corporation

- 6.4.11 ABM Industries Inc.

- 6.4.12 G4S Limited

- 6.4.13 Atalian Global Services

- 6.4.14 Vinci Facilities (VINCI SA)

- 6.4.15 EMCOR Group Inc.

- 6.4.16 Comfort Systems USA

- 6.4.17 Balfour Beatty - Workplace

- 6.4.18 Serco Group plc

- 6.4.19 Reliance Facilities (India)

- 6.4.20 Sinopec Engineering FM (China)

- 6.4.21 Unispace Global

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

烟草综合设施管理市场:按服务类型、设施类型、合约类型、组织规模和最终用户划分 - 2026-2032 年全球预测综合设施管理市场:按服务类型、部署模式和最终用户划分 - 2026-2032年全球预测

烟草综合设施管理市场:按服务类型、设施类型、合约类型、组织规模和最终用户划分 - 2026-2032 年全球预测综合设施管理市场:按服务类型、部署模式和最终用户划分 - 2026-2032年全球预测 2026年设施管理领域十大成长机会亚太地区设施管理市场,2026-2031年

2026年设施管理领域十大成长机会亚太地区设施管理市场,2026-2031年 机器人即服务 (RaaS) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分电脑辅助设施管理 (CAFM) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和模组划分设施管理市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及解决方案划分

机器人即服务 (RaaS) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分电脑辅助设施管理 (CAFM) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和模组划分设施管理市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及解决方案划分 亚太地区设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

亚太地区设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲设施管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)