|

市场调查报告书

商品编码

1910859

法国网路安全市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)France Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

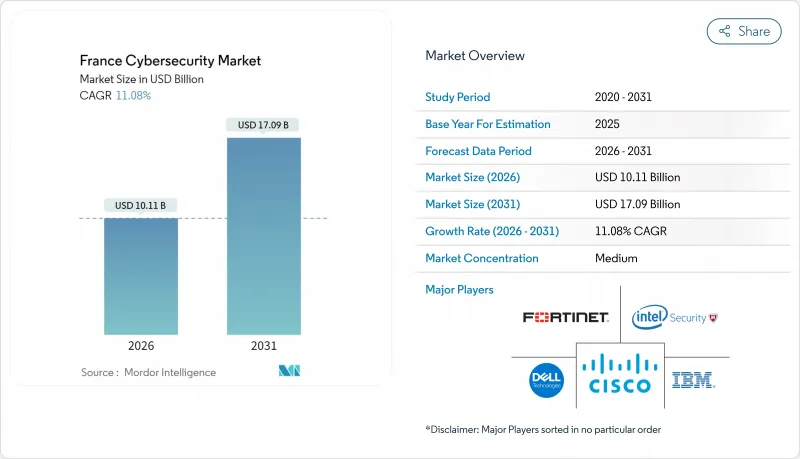

法国网路安全市场预计到 2025 年将达到 91 亿美元,到 2026 年将成长到 101.1 亿美元,到 2031 年将成长到 170.9 亿美元,预测期(2026-2031 年)的复合年增长率为 11.08%。

NIS2法规的快速扩展、公共部门资金的增加以及云端迁移的激增,共同为供应商带来了更多潜在机会。企业持续整合其安全架构,增加对整合平台的投入,以减轻合规负担并缓解人才短缺问题。为解决熟练人员长期短缺的问题,对资安管理服务的需求激增,而人工智慧驱动的分析正成为法国安全营运中心(SOC)的标配。奥运期间网路安全活动的活性化,正在永久改变法国对威胁的认知,并促使企业对医疗保健、能源和交通等关键领域的威胁监控基础设施进行长期投资。

法国网路安全市场趋势与洞察

加速NIS2实施及法国政府网路安全资金投入

NIS2 将监管范围从 500 家法国公司扩大到约 15,000 家,受监管行业数量增加了两倍。对管治、风险和合规 (GRC) 工具的需求正在蓬勃发展。法国政府的「法国 2030」计画累计3,900 万欧元(约 4,200 万美元)用于 17 个资讯安全相关计划,以提升国家网路安全能力。法国国家资讯安全局 (ANSSI) 的分阶段实施政策强调能力建构而非製裁,这刺激了企业应对漏洞的需求,也促使企业争相解决安全漏洞。政府计划以 7 亿欧元(约 7.48 亿美元)收购 Atos 的网路安全资产,进一步凸显了国内智慧财产权的战略价值。这些措施共同註入了资金,扩大了基本客群,并巩固了法国网路安全市场作为欧洲合规中心的地位。

法国关键基础设施和医疗保健领域勒索软体激增

法国国家安全资讯系统管理局 (ANSSI) 记录显示,2024 年共发生 4,386 起安全事件(较前一年增加 15%),其中医疗保健产业占勒索软体攻击报告总数的 10%。阿尔芒蒂耶尔和科尔贝-埃鬆的医院被迫关闭,导致对固定价格的端点检测和事件回应服务的需求激增。卢浮宫和大皇宫等文化机构也受到影响,这显示没有一个产业能够倖免。支出已转向扩展灾难復原 (XDR) 平台和危机管理咨询,这表明法国网路安全市场作为快速服务交付中心的地位正在增强。

网路安全人才严重短缺推高了安全营运中心(SOC)的成本。

儘管自2020年以来网路安全人才成长了89%,但全国仍存在约15,000个职缺。高级分析师的薪资已高达90,000欧元(约96,300美元),这挤压了服务提供者的利润空间,并推动了自动化进程。泰雷兹公司实施了GenAI4SOC系统,并将个案分诊效率提高了40%。虽然这些努力缓解了人才短缺问题,但并未彻底消除人才短缺,这仍然是法国网路安全市场全面扩张的一大障碍。

细分市场分析

到2025年,解决方案业务将占总收入的52.10%,其中统一威胁管理套件和XDR的普及加速了企业减少工具冗余的需求。随着越来越多的客户将全天候监控外包以应对人员短缺问题,託管服务正以12.85%的复合年增长率快速成长。身分识别和存取管理工具,尤其是特权存取管理,对于零信任架构的实作至关重要。例如,Wallix正利用其获得法国国家资讯安全局(ANSSI)认证的优势来吸引受监管的客户。专业服务是软体支出的补充,提供旨在实现NIS2(网路资讯安全指令)目标的评估和补救计划。虽然硬体设备仍然至关重要,但它们与人工智慧驱动的分析功能的整合凸显了法国网路安全市场的融合特征。

这种整合趋势正在推动混合消费模式的出现,即买家获得核心平台的许可,并额外购买用于事件回应的持续服务。这种方式既延长了供应商的生命週期价值,又能在预算紧张时期提供柔软性。随着勒索软体攻击的日益增多,用于事件回应的持续服务已成为银行、金融和保险 (BFSI) 以及医疗保健行业的基本需求,从而稳步扩大了法国保全服务市场的规模。

到2025年,云端采用将占支出的59.78%,这反映出SaaS的广泛应用以及中小企业快速进入云端领域的趋势。法国网路安全市场中与云端解决方案相关的规模预计将以14.25%的复合年增长率成长,超过本地部署平台,因为关键工作负载正在迁移到混合环境中。 SecNumCloud认证正在增强人们对国内託管的信心,使OVHcloud和Outscale等业者受益。

在国防和监管严格的公共产业领域,本地部署模式仍然占据主导地位,因为在这些领域,资料居住和延迟要求比扩充性更为重要。然而,即使是这些领域也在采用基于云端的分析来增强传统的控制功能。能够跨多个云端供应商标准化策略的多重云端编配平台正变得越来越受欢迎,这降低了企业在寻求超越单一超大规模资料中心业者服务商时被供应商锁定的风险。因此,法国网路安全市场正在进一步模糊传统部署的界限,并朝着以控制平面为中心的架构发展。

法国网路安全市场报告按公共产业类型(解决方案、服务)、部署模式(本地部署、云端部署)、最终用户垂直产业(银行、金融服务和保险、医疗保健、IT 和电信、工业和国防、製造业、零售和电子商务、能源和公用事业、其他)以及最终用户公司规模(中小企业、大型企业)对产业进行细分。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 加快实施NIS2标准并增加对法国政府网路安全计画的资金投入

- 法国关键基础设施和医疗保健产业遭受勒索软体攻击激增

- 2024年巴黎奥运推动了威胁监测投资

- 法国NUM数位代金券推动中小企业云端迁移

- 校园网路生态系统驱动区域解决方案创新

- 向远端办公的转变需要零信任和身分与存取管理 (IAM) 升级。

- 市场限制

- 网路安全人才严重短缺正在推高安全营运中心(SOC)服务成本。

- 法国中小企业将网路安全视为营运支出 (OPEX),并倾向于避免预算限制。

- 由于法规重迭(GDPR、NIS2、ANSSI产业法规)导致的采购延误

- 工具分散且整合复杂,导致技术栈碎片化。

- 重要法规结构评估

- 价值链分析

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 主要用例和案例研究

- 宏观经济因素对市场的影响

- 投资分析

第五章 市场区隔

- 报价

- 解决方案

- 应用程式安全

- 云端安全

- 资料安全

- 身分和存取管理

- 基础设施保护

- 综合风险管理

- 网路安全设备

- 端点安全

- 其他服务

- 服务

- 专业服务

- 託管服务

- 解决方案

- 透过部署模式

- 本地部署

- 云

- 按最终用户行业划分

- BFSI

- 卫生保健

- 资讯科技/通讯

- 工业与国防

- 製造业

- 零售与电子商务

- 能源与公共产业

- 製造业

- 其他的

- 按最终用户公司规模划分

- 中小企业

- 大公司

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- IBM Corporation

- Cisco Systems Inc.

- Dell Technologies Inc.(SecureWorks)

- Fortinet Inc.

- Intel Security(McAfee LLC)

- F5 Networks Inc.

- AVG Technologies(Gen Digital)

- IDECSI Enterprise Security

- Trellix(Formerly FireEye)

- Thales Group

- Orange Cyberdefense

- Atos SE(Eviden)

- Capgemini SE

- Sopra Steria Group SA

- Airbus Defence & Space CyberSecurity

- Stormshield

- Wallix Group

- Exclusive Networks SA

- Check Point Software Technologies Ltd.

- Palo Alto Networks Inc.

- CrowdStrike Holdings Inc.

- Trend Micro Inc.

- Okta Inc.

- Darktrace plc

第七章 市场机会与未来展望

The France cybersecurity market was valued at USD 9.10 billion in 2025 and estimated to grow from USD 10.11 billion in 2026 to reach USD 17.09 billion by 2031, at a CAGR of 11.08% during the forecast period (2026-2031).

Rapid regulatory expansion under NIS2, heavier public-sector funding, and a sharp rise in cloud migration are synchronizing to widen the addressable opportunity for vendors. Enterprises continue to consolidate security stacks, channeling spending toward integrated platforms that ease compliance and talent pressures. Managed security services are surging as buyers offset a persistent shortage of skilled practitioners, while AI-driven analytics are becoming standard in French security operations centers. Heightened Olympic-period cyber activity has permanently recalibrated domestic threat awareness, prompting long-term investment in threat-monitoring infrastructure across critical sectors such as healthcare, energy, and transportation.

France Cybersecurity Market Trends and Insights

Accelerated NIS2 adoption and French Government cyber funding

NIS2 widens the compliance net from 500 to roughly 15,000 French entities, tripling the number of regulated sectors and intensifying demand for governance, risk, and compliance tooling. France 2030 earmarked EUR 39 million (USD 42 million) for 17 cybersecurity projects, anchoring sovereign capability development. ANSSI's phased roll-out stresses enablement over sanction, spurring advisory services as firms race to close gaps. Government interest in acquiring Atos' cybersecurity assets for EUR 700 million (USD 748 million) further underlines the strategic value of domestic IP. Together these moves inject capital, enlarge the client base, and reinforce the France cybersecurity market as a continental compliance hub.

Ransomware surge on French critical infrastructure and healthcare

ANSSI logged 4,386 security incidents in 2024, up 15% year on year, with healthcare representing 10% of ransomware filings. Hospitals at Armentieres and Corbeil-Essonnes endured emergency shutdowns, driving urgency around endpoint detection and incident-response retainer services. Cultural landmarks such as the Louvre and Grand Palais also faced disruptions, proving no sector is immune. Spending is pivoting toward XDR platforms and crisis-management consulting, reinforcing the France cybersecurity market as a responsive services arena.

Acute cyber-talent shortage inflating SOC costs

Roughly 15,000 cybersecurity vacancies persist nationwide, despite an 89% workforce expansion since 2020. Salary inflation reaches EUR 90,000 (USD 96,300) for senior analysts, squeezing provider margins and stimulating automation. Thales responded with GenAI4SOC to improve case triage efficiency by 40%. Such initiatives temper, but do not erase, the talent gap that restrains the France cybersecurity market's ability to scale fully.

Other drivers and restraints analyzed in the detailed report include:

- Paris 2024 Olympics-driven threat-monitoring investments

- SME cloud-migration boom under "France Num" digital vouchers

- Budget aversion among SMEs viewing cyber as OPEX

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions generated 52.10% of 2025 revenue, with unified threat-management suites and XDR gaining traction as enterprises rationalize tool sprawl. The managed-services slice is growing at 12.85% CAGR as clients contract out 24/7 monitoring to compensate for staffing gaps. Identity-and-access tools, especially privileged-access management, underpin Zero-Trust rollouts. Wallix, for example, leverages its ANSSI qualification to court regulated clients. Professional services complement software spend, delivering assessment and remediation projects tied to NIS2 milestones. Hardware appliances remain foundational but are increasingly bundled with AI-driven analytics, illustrating the convergence that defines the France cybersecurity market.

The integration trend is fostering hybrid consumption models in which buyers license core platforms and overlay retained services for incident response. This approach expands lifetime value for vendors while providing flexibility in tight budget cycles. As ransomware campaigns intensify, incident-response retainers are now a baseline requirement across BFSI and healthcare, pushing the France cybersecurity market size for services steadily upward.

Cloud deployments accounted for 59.78% of 2025 spending, reflecting widespread SaaS preference and rapid SME onboarding. The France cybersecurity market size attached to cloud solutions is forecast to rise at a 14.25% CAGR, outpacing the on-premise base as more critical workloads move to hybrid environments. SecNumCloud certification accelerates trust in domestic hosting, benefiting players such as OVHcloud and Outscale.

On-premise models persist in defense and heavily regulated utilities where data residency and latency demands outweigh elasticity. Yet even these sectors adopt cloud-based analytics to augment legacy controls. Multi-cloud orchestration platforms that normalize policy across providers are gaining lift, mitigating vendor lock-in risks for enterprises expanding beyond a single hyperscaler. As a result, the France cybersecurity market continues to blur traditional deployment lines, pivoting toward control-plane-centric architectures.

The France Cybersecurity Market Report Segments the Industry Into by Offering (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-User Vertical (BFSI, Healthcare, IT and Telecom, Industrial and Defense, Manufacturing, Retail and E-Commerce, Energy and Utilities, Manufacturing, and Others), and End-User Enterprise Size (Small and Medium Enterprises (SMEs), and Large Enterprises)

List of Companies Covered in this Report:

- IBM Corporation

- Cisco Systems Inc.

- Dell Technologies Inc. (SecureWorks)

- Fortinet Inc.

- Intel Security (McAfee LLC)

- F5 Networks Inc.

- AVG Technologies (Gen Digital)

- IDECSI Enterprise Security

- Trellix (Formerly FireEye)

- Thales Group

- Orange Cyberdefense

- Atos SE (Eviden)

- Capgemini SE

- Sopra Steria Group SA

- Airbus Defence & Space CyberSecurity

- Stormshield

- Wallix Group

- Exclusive Networks SA

- Check Point Software Technologies Ltd.

- Palo Alto Networks Inc.

- CrowdStrike Holdings Inc.

- Trend Micro Inc.

- Okta Inc.

- Darktrace plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated NIS2 adoption and Increasing French Government Cyber Plan funding

- 4.2.2 Ransomware surge on French critical infrastructure and healthcare

- 4.2.3 Paris 2024 Olympics-driven threat-monitoring investments

- 4.2.4 SME cloud-migration boom under "France Num" digital vouchers

- 4.2.5 Campus Cyber ecosystem catalysing local solution innovation

- 4.2.6 Remote-work shift demanding Zero-Trust and IAM upgrades

- 4.3 Market Restraints

- 4.3.1 Acute cyber-talent shortage inflating SOC service costs

- 4.3.2 Budget aversion among French SMEs viewing cyber as OPEX

- 4.3.3 Regulatory overlap (GDPR, NIS2, ANSSI sector rules) delaying buys

- 4.3.4 Tool-sprawl and integration complexity across fragmented stack

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Application Security

- 5.1.1.2 Cloud Security

- 5.1.1.3 Data Security

- 5.1.1.4 Identity and Access Management

- 5.1.1.5 Infrastructure Protection

- 5.1.1.6 Integrated Risk Management

- 5.1.1.7 Network Security Equipment

- 5.1.1.8 Endpoint Security

- 5.1.1.9 Other Services

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Manufacturing

- 5.3.6 Retail and E-commerce

- 5.3.7 Energy and Utilities

- 5.3.8 Manufacturing

- 5.3.9 Others

- 5.4 By End-User Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 IBM Corporation

- 6.4.2 Cisco Systems Inc.

- 6.4.3 Dell Technologies Inc. (SecureWorks)

- 6.4.4 Fortinet Inc.

- 6.4.5 Intel Security (McAfee LLC)

- 6.4.6 F5 Networks Inc.

- 6.4.7 AVG Technologies (Gen Digital)

- 6.4.8 IDECSI Enterprise Security

- 6.4.9 Trellix (Formerly FireEye)

- 6.4.10 Thales Group

- 6.4.11 Orange Cyberdefense

- 6.4.12 Atos SE (Eviden)

- 6.4.13 Capgemini SE

- 6.4.14 Sopra Steria Group SA

- 6.4.15 Airbus Defence & Space CyberSecurity

- 6.4.16 Stormshield

- 6.4.17 Wallix Group

- 6.4.18 Exclusive Networks SA

- 6.4.19 Check Point Software Technologies Ltd.

- 6.4.20 Palo Alto Networks Inc.

- 6.4.21 CrowdStrike Holdings Inc.

- 6.4.22 Trend Micro Inc.

- 6.4.23 Okta Inc.

- 6.4.24 Darktrace plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

网路安全市场:按组件、安全类型、组织规模、部署模式和产业划分-2026-2032年全球市场预测

网路安全市场:按组件、安全类型、组织规模、部署模式和产业划分-2026-2032年全球市场预测 人工智慧网路安全市场预测至2034年—按交付方式、安全类型、部署方式、技术、应用、最终用户和地区分類的全球分析金融科技网路安全解决方案市场预测至2034年-按组件、安全类型、部署模式、组织规模、应用、最终用户和地区分類的全球分析

人工智慧网路安全市场预测至2034年—按交付方式、安全类型、部署方式、技术、应用、最终用户和地区分類的全球分析金融科技网路安全解决方案市场预测至2034年-按组件、安全类型、部署模式、组织规模、应用、最终用户和地区分類的全球分析 2026-2030年全球智慧体与自主人工智慧系统网路安全解决方案市场

2026-2030年全球智慧体与自主人工智慧系统网路安全解决方案市场 网路安全市场规模、份额、趋势和预测:按组件、部署类型、用户类型、行业和地区划分,2026-2034 年

网路安全市场规模、份额、趋势和预测:按组件、部署类型、用户类型、行业和地区划分,2026-2034 年 2026年全球建筑网路安全市场报告2026年全球电网网路安全市场报告2026年全球旅游安全市场报告

2026年全球建筑网路安全市场报告2026年全球电网网路安全市场报告2026年全球旅游安全市场报告 全球网路靶场市场报告:实际结果与预测(2021-2032)2026年全球Web3安全市场报告

全球网路靶场市场报告:实际结果与预测(2021-2032)2026年全球Web3安全市场报告