|

市场调查报告书

商品编码

1934821

法国最后一公里配送:市场占有率分析、产业趋势与统计、成长预测(2026-2031)France Last Mile Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

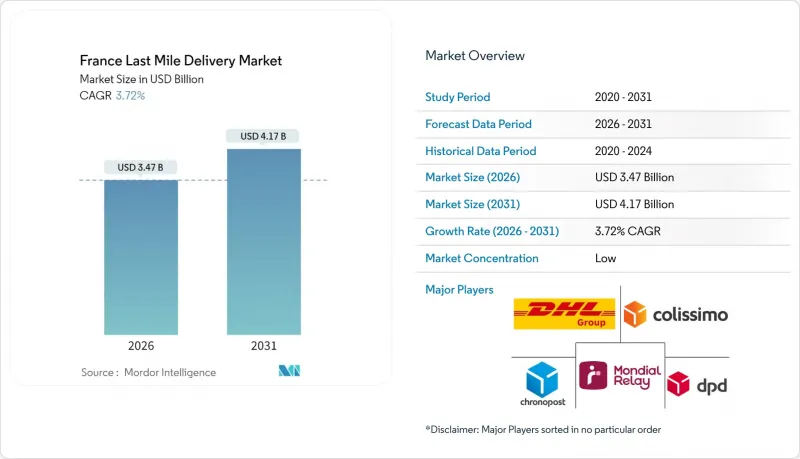

法国最后一公里配送市场预计将从 2025 年的 33.5 亿美元成长到 2026 年的 34.7 亿美元,到 2031 年达到 41.7 亿美元,2026 年至 2031 年的复合年增长率为 3.72%。

电子商务交易量的成长、宅配柜网路的密集化以及政府为加速车辆电气化而采取的奖励,推动了市场需求的成长。随着全球聚合商、区域宅配服务商和数位平台竞相争夺路线密度和包裹柜使用权,竞争日益激烈,迫使营运商调整收费系统以适应低价值跨境小包裹的需求。都市区拥挤、配送人员短缺以及微型配送中心用地不足制约了市场成长,而暗店合作和对温控物流的投资则持续开拓加值服务市场。如今,盈利依赖于自动化分类、多样化的取件和投递(PUDO)选择以及零排放车辆的引入,所有这些都能在监管严格的城市中心降低成本并带来竞争优势。

法国最后一公里配送市场趋势与分析

电子商务订单量快速成长

法国邮政的Colissimo服务在2024年处理了数百万个小包裹。订单密度的增加正在推动网路扩张,Geopost在2024年对分类机和配送中心的资本投资就证明了这一点。然而,盈利呈现两极化:来自Shein和Temu等平台的轻型包裹虽然增加了总运量,但利润却很低。业者透过提升销售追踪、指定地点递送和碳中和等高价增值服务来弥补利润率的下降。

扩大自宅配柜和PUDO基础设施

法国邮政营运12.8万个取货点和自助取件柜,建构了欧洲最密集的网络,有效降低了投递失败成本,并提升了客户满意度。其子公司Mondial 继电器计划到2025年将其自助取件柜网路扩展至7,000个,同时精简利用率不足的零售代理点。 Mondial Relay在2024年第三季处理的6,230万小包裹中,约有30%是透过自助取件柜寄送的,这显示消费者更倾向于灵活便捷的非接触式取件方式。对于快递公司而言,提高自助取件柜密度能够将多个包裹集中到一个地点,从而显着降低最后一公里配送成本,同时提高司机效率并减少碳排放。

都市区的交通和停车限制

巴黎是欧洲交通最拥挤的三大城市之一,都市区车速低于13公里/小时,外送司机停车时间过长。市政停车费和送货时间的缩短加剧了配送能力的紧张,而强制司机轮班工作则增加了人事费用。为了回应这个问题,开发商提案城市集散中心的方案,例如SEGRO的Les Gobelins项目,这是一个位于巴黎市中心15分钟车程、占地1600平方公尺的枢纽。这些微型枢纽平均可将最终配送距离缩短1.3公里,但由于缺乏指定的工业用地,其推广应用受到阻碍。

细分市场分析

2025年,利用现有邮局、长程干线和经济高效的批量分拣,标准配送将占据法国最后一公里配送市场42.55%的份额。该细分市场透过提供可预测的工作量并优化其枢纽辐射式基础设施,在郊区和区域路线上保持了有利的密度经济效益。随着消费者对必需品配送速度的需求不断成长,其规模优势依然存在。当日配送服务正以3.78%的复合年增长率成长,这主要得益于都市区消费者即时的需求以及零售商「下午1点前下单,当日送达」的承诺。营运商正将高价策略与碳中和认证相结合,以维持利润率。快递仍然是企业客户对时效性要求高的B2B货物运输的主要选择,填补了经济型配送和当日配送之间的空白。

成长率的差异预示着未来物流格局将呈现两极化:便利型商品将透过快速通路运输,而体积较大、价值较低的商品则继续走经济型路线。零售商正在推广混合购物车结帐模式,让消费者将新鲜商品与标准商品分开购买,分别享有当日送达和免费送货服务。这种柔软性有助于提高收入,同时避免网路过载。对于承运商而言,如何在同一路线上协调不同速度的配送是一项重大的最佳化挑战,需要动态调度和即时运力资讯。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电子商务订单量快速成长

- 扩大宅配柜和PUDO基础设施

- 政府对零排放送货车辆的激励措施

- 都市区暗店与奈米履约的发展

- 社群电商推动了微型配送频率的提升

- 城市集聚中心的市政指令

- 市场限制

- 城市交通和停车位限制

- 宅配员短缺和工资上涨

- 都市区微型枢纽房地产短缺

- 民众对无人机监管的抵抗与障碍

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方和消费者的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 透过服务

- 标准配送

- 当日送达

- 快递

- 按经营模式

- 企业对企业 (B2B)

- 企业对消费者 (B2C)

- 客户对客户 (C2C)

- 按最终用户行业划分

- 电子商务零售

- 时尚与生活风格

- 美容、健康和个人护理

- 居家及家具

- 家用电器/家用电器

- 医疗用品

- 其他的

- 按法国地区划分

- 法国法兰西岛

- 奥弗涅-罗纳-阿尔卑斯大区

- 普罗旺斯-阿尔卑斯-蓝色海岸

- 上法兰西区

- 新阿基坦

- 奥克西塔尼

- 格兰德埃斯特

- 布列塔尼

- 其他的

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Colissimo(La Poste Group)

- Chronopost

- DPD

- Mondial Relay(InPost)

- DHL Express

- FedEx

- UPS

- GLS

- Colis Prive

- Cubyn

- Geodis

- DSV

- Yusen Logistics

- GOFO

- Relais Colis

- Rhenus Logistics

- My Delivery France

- AIT Worldwide Logistics

- CEVA Logistics

第七章 市场机会与未来展望

The France Last Mile Delivery market is expected to grow from USD 3.35 billion in 2025 to USD 3.47 billion in 2026 and is forecast to reach USD 4.17 billion by 2031 at 3.72% CAGR over 2026-2031.

Demand scales with e-commerce volume growth, the densification of parcel-locker networks, and government incentives that accelerate fleet electrification. Competitive intensity has risen as global integrators, regional parcel specialists, and digital platforms jostle for route density and locker access, forcing operators to adjust tariffs in response to low-value cross-border parcels. Urban congestion, courier shortages, and scarce micro-hub real estate temper growth, yet investment in dark-store partnerships and temperature-controlled logistics continues to open premium service niches. Profitability now hinges on automated sortation, pickup-drop-off (PUDO) diversification, and zero-emission vehicle deployment, each delivering incremental cost and access advantages in heavily regulated urban cores.

France Last Mile Delivery Market Trends and Insights

Explosion in e-commerce order volume

La Poste's Colissimo processed millions of parcels in 2024. Higher order density fuels network expansion, evidenced by Geopost's capital spend on automated sorters and depots in 2024. Yet profitability diverges: lightweight shipments from platforms such as Shein and Temu carry wafer-thin yields even as they lift headline volumes. Operators counter margin pressure by upselling tracked, scheduled, or carbon-neutral options that command premium fees.

Expansion of parcel locker & PUDO infrastructure

La Poste hosts 128,000 pickup points and lockers-the densest network in Europe, cutting failed-delivery costs and lifting customer satisfaction scores. InPost-owned Mondial Relay raised its automated locker count to 7,000 by 2025 while pruning low-traffic retail agents. Nearly 30% of Mondial Relay's 62.3 million Q3-2024 parcels flowed through lockers, signaling shopper preference for flexible, contactless retrieval. For carriers, locker density collapses last-mile unit cost by consolidating multiple drop-offs into a single location, improving driver productivity and shrinking carbon intensity.

Urban traffic & parking constraints

Paris ranks among Europe's top three congestion hot spots, pushing average urban route speed below 13 km/h and inflating driver hours per stop. Municipal curb fees and reduced delivery windows squeeze capacity, forcing split-shift scheduling that raises labor requirements. Developers respond with urban consolidation centers like SEGRO's Les Gobelins, a 1,600-m2 hub fifteen minutes from central Paris. Such micro-hubs shave 1.3 km off average last-leg distance, yet the limited availability of industrial-zoned plots curtails widespread replication.

Other drivers and restraints analyzed in the detailed report include:

- Government incentives for zero-emission delivery fleets

- Growth of urban dark stores & nano-fulfillment

- Courier labor shortages & wage inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standard Delivery captured 42.55% of the France last mile delivery market share in 2025 by leveraging established postal depots, long-haul line-hauls, and cost-efficient batch sorting. The segment supplies predictable workloads that optimize hub-and-spoke infrastructure, sustaining favorable drop-density economics across suburban and rural routes. Volume leadership persists even as consumers upgrade to faster tiers for mission-critical items. Same-day services, advancing at a 3.78% CAGR, ride urban shopper expectations for immediacy and retailer promises of "order-by-1 pm-receive-today." Operators bundle premium fees with carbon-neutral badges to preserve margin. Express Delivery holds steady as a business account staple for time-definite B2B shipments, filling the gap between economy and same-day.

Growth differentials hint at a bifurcated future where convenience-led SKUs flow through rapid-cycle channels, while bulkier, lower-value items continue in economy lanes. Retailers increasingly offer hybrid cart checkout, letting shoppers split baskets between same-day perishables and slower, free-shipping lines. That elasticity underpins incremental revenue while preventing network overload. For carriers, orchestrating multi-speed promises within a single route remains the primary optimization frontier, demanding dynamic dispatching and real-time capacity visibility.

The France Last Mile Delivery Market Report is Segmented by Service (Standard Delivery, Same-Day, and Express Delivery), Business Model (Business-To-Business (B2B), Business-To-Consumer (B2C), and Customer-To-Consumer (C2C)), End-User Industry (E-Commerce Retail, Fashion & Lifestyle, Beauty, and More), Region (Hauts-De-France, Nouvelle-Aquitaine, Occitanie, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Colissimo (La Poste Group)

- Chronopost

- DPD

- Mondial Relay (InPost)

- DHL Express

- FedEx

- UPS

- GLS

- Colis Prive

- Cubyn

- Geodis

- DSV

- Yusen Logistics

- GOFO

- Relais Colis

- Rhenus Logistics

- My Delivery France

- AIT Worldwide Logistics

- CEVA Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosion in e-commerce order volume

- 4.2.2 Expansion of parcel locker & PUDO infrastructure

- 4.2.3 Government incentives for zero-emission delivery fleets

- 4.2.4 Growth of urban dark stores & nano-fulfilment

- 4.2.5 Social commerce boosts micro-shipment frequency

- 4.2.6 Municipal mandates for urban consolidation centres

- 4.3 Market Restraints

- 4.3.1 Urban traffic & parking constraints

- 4.3.2 Courier labour shortages & wage inflation

- 4.3.3 Scarcity of urban micro-hub real estate

- 4.3.4 Public resistance & drone-regulation hurdles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers/Consumers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service

- 5.1.1 Standard Delivery

- 5.1.2 Same-day

- 5.1.3 Express Delivery

- 5.2 By Business Model

- 5.2.1 Business-to-Business (B2B)

- 5.2.2 Business-to-Consumer (B2C)

- 5.2.3 Customer-to-Consumer (C2C)

- 5.3 By End-user Industry

- 5.3.1 E-commerce Retail

- 5.3.2 Fashion & Lifestyle

- 5.3.3 Beauty, Wellness & Personal Care

- 5.3.4 Home & Furniture

- 5.3.5 Consumer Electronics & Appliances

- 5.3.6 Healthcare & Medical Supplies

- 5.3.7 Others

- 5.4 By French Region

- 5.4.1 Ile-de-France

- 5.4.2 Auvergne-Rhone-Alpes

- 5.4.3 Provence-Alpes-Cote d'Azur

- 5.4.4 Hauts-de-France

- 5.4.5 Nouvelle-Aquitaine

- 5.4.6 Occitanie

- 5.4.7 Grand Est

- 5.4.8 Brittany

- 5.4.9 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Colissimo (La Poste Group)

- 6.4.2 Chronopost

- 6.4.3 DPD

- 6.4.4 Mondial Relay (InPost)

- 6.4.5 DHL Express

- 6.4.6 FedEx

- 6.4.7 UPS

- 6.4.8 GLS

- 6.4.9 Colis Prive

- 6.4.10 Cubyn

- 6.4.11 Geodis

- 6.4.12 DSV

- 6.4.13 Yusen Logistics

- 6.4.14 GOFO

- 6.4.15 Relais Colis

- 6.4.16 Rhenus Logistics

- 6.4.17 My Delivery France

- 6.4.18 AIT Worldwide Logistics

- 6.4.19 CEVA Logistics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2026年人工智慧驱动的最后一公里配送全球市场报告

2026年人工智慧驱动的最后一公里配送全球市场报告 自动驾驶最后一公里配送市场:依服务类型、推进方式、配送距离、组件和最终用户产业划分-2026-2032年全球市场预测食品低温运输最后一公里配送市场:依运输方式、服务类型、温度区域、配送方式及最终用户划分-2026-2032年全球市场预测2026年全球最后一公里配送市场报告2026年全球首末一公里配送市场报告2026年全球太空货物运输市场报告

自动驾驶最后一公里配送市场:依服务类型、推进方式、配送距离、组件和最终用户产业划分-2026-2032年全球市场预测食品低温运输最后一公里配送市场:依运输方式、服务类型、温度区域、配送方式及最终用户划分-2026-2032年全球市场预测2026年全球最后一公里配送市场报告2026年全球首末一公里配送市场报告2026年全球太空货物运输市场报告 最后一公里配送车辆技术市场-策略性洞察与预测(2026-2031年)

最后一公里配送车辆技术市场-策略性洞察与预测(2026-2031年) 首末公里旅游市场预测至2034年-按运输方式、技术、服务类型、最终用户和地区分類的全球分析全球最后一公里配送市场规模、份额、趋势和成长分析报告(2026-2034)2026年全球最后一公里配送软体市场报告

首末公里旅游市场预测至2034年-按运输方式、技术、服务类型、最终用户和地区分類的全球分析全球最后一公里配送市场规模、份额、趋势和成长分析报告(2026-2034)2026年全球最后一公里配送软体市场报告