|

市场调查报告书

商品编码

1934833

越南电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Vietnam Telecom MNO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

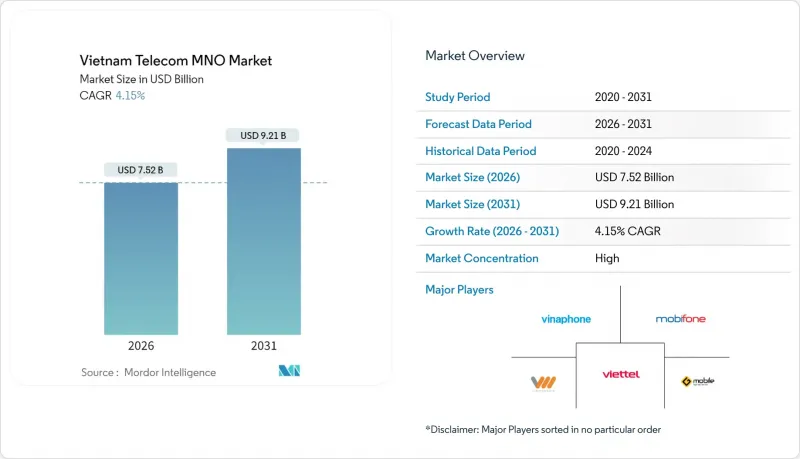

预计到 2026 年,越南电信行动网路营运商 (MNO) 市场的规模将达到 75.2 亿美元。

预计该产业规模将从 2025 年的 72.2 亿美元成长到 2031 年的 92.1 亿美元,2026 年至 2031 年的复合年增长率为 4.15%。

不断增长的数据消费、全国范围内的5G网路部署以及政府的支持性政策正在推动越南电信服务从语音转型为数位服务。同时,通讯业者正利用高端企业服务来应对语音收入的下滑。对边缘运算、私人5G网路和卫星农村接入的投资正在扩大目标用户群体,并支撑越南电信行动网路营运商(MNO)市场的稳定收入成长。儘管价格竞争仍然激烈,但严格的基础设施共用有效控制了营运成本和资本支出,从而维持了营运利润率。高度集中的市场格局——三家国有通讯业者占据了超过95%的用户份额——为快速的技术升级提供了必要的规模,并保护了越南电信行动网路营运商市场免受新进入者的衝击。

越南电信行动网路营运商市场趋势与洞察

4G和5G的快速部署将推动行动数据需求的激增。

2025年4月进行的早期5G试验实现了364.43 Mbps的平均速度,加速了对高频宽服务的需求。随着2G服务在2026年和3G服务在2028年强制终止,用户正在迁移到更高价值的4G和5G套餐,这自然提高了每位用户平均收入(ARPU)。 Viettel在短短几个月内就获得了400万5G用户,其中70%的用户体验到了超过1.5 Gbps的速度,这证明消费者愿意为高性能支付更高的价格。基础设施共用降低了部署成本,并实现了全国63个省份的覆盖。快速成长的流量推动了边缘运算节点和内容分发网路(CDN)的发展,通讯业者正在向越南电信行动网路营运商(MNO)市场中更广泛的数位基础设施公司转型。

国家数位转型计画加速宽频普及

政府的目标是到2024年10月达到82.4%的家庭光纤覆盖,这一目标已提前于2025年实现。 2024年发放的2,000万张电子ID卡增加了可靠宽频接取电子政府服务的需求。一个处理了13亿次查询的人口资料库表明,数位活动的规模之大需要强大的网路支援。 48个智慧城市计划和岘港市的半导体投资为通讯业者带来了可预测的流量。新的数位服务进一步推动了对网路连接的需求,形成良性循环,确保越南电信行动网路营运商(MNO)市场的收入持续成长。

日益激烈的价格竞争对每位用户平均收入(ARPU)带来压力。

诸如FPT Telecom计划于2025年4月将住宅宽频速度翻倍频宽升级方案,加速了每兆位元成本的下降。 VNPT和Viettel也采取了类似策略,随着OTT应用在通讯占据主导地位,语音和简讯收入有所下降。儘管通讯业者寻求透过网路共用提高成本效益,但持续的ARPU(每用户平均收入)压力正迫使越南电信行动网路营运商(MNO)市场转向企业级和垂直整合解决方案。

细分市场分析

到2025年,数据和互联网服务将占越南电信行动网路营运商(MNO)市场48.62%的份额,这印证了越南电信市场正经历从语音到数位连接的结构性转变。物联网/机器对机器(IoT/M2M)领域已呈现4.32%的年复合成长率(CAGR)的最快成长势头,随着工厂自动化和城市智慧基础设施平台的普及,其市场规模预计将迅速扩张。语音和简讯服务已被OTT通讯和通话服务所取代,延续了长期下滑的趋势。付费电视和捆绑式OTT影片服务则受益于不断扩展的光纤网路而蓬勃发展,推动了家庭平均每用户收入(ARPU)的成长。

5G 能够支援边缘运算、AR/VR 和网路切片,为通讯业者提供以高性价比价格提供高速网路和低延迟服务的途径。针对超大规模资料中心的批发回程回程传输能够带来高收益客户,而数位钱包等附加价值服务(VAS) 则能提升交叉销售收入。虽然这些相邻的收入来源能够缓解传统现金流下滑的风险,但升级越南电信行动网路营运商 (MNO) 市场的客户体验平台对于成功收购至关重要。

越南电信行动网路营运商 (MNO) 市场按服务类型(语音服务、数据及网际网路服务、通讯服务、物联网及机器对机器 (IoT & M2M) 服务、OTT 及付费电视服务、其他服务)及最终用户(企业、消费者)进行细分。市场预测以价值(美元)和用户数量(用户数)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 监理与政策框架

- 频谱环境与竞争格局

- 通讯业生态系统

- 宏观经济与外在因素

- 波特五力模型

- 竞争对手之间的竞争

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 领先行动网路营运商的关键绩效指标(2020-2025)

- 独立行动用户和渗透率

- 行动网路使用者数量和普及率

- 按接入技术分類的SIM卡连线数和渗透率

- 蜂巢式物联网/M2M连接

- 宽频连线(移动和固定)

- ARPU(每位用户平均收入)

- 用户平均每月数据使用量(GB/月)

- 市场驱动因素

- 4G和5G的快速部署将推动行动数据需求的激增。

- 国家数位转型计画加速宽频普及

- 智慧型手机价格亲民,推动了数据流量消耗。

- 资料中心扩张正在推动对批发光纤的需求。

- 在製造地部署私有 5G/IoT

- 光纤付费电视方案提升家庭平均每用户收入

- 市场限制

- 日益激烈的价格竞争对每位用户平均收入(ARPU)带来压力。

- 频谱高成本且重复使用延迟

- 山区通行权成本较高,导致遍远地区的光纤安装工程停滞不前。

- 缺乏对新成立的虚拟营运商(MVNO)的监管,阻碍了服务创新。

- 技术展望

- 电信业主要经营模式分析

- 定价模式和定价分析

第五章 市场规模与成长预测

- 通信总收入和每位用户平均收入

- 服务类型

- 语音服务

- 数据和网际网路服务

- 通讯服务

- 物联网和机器对机器服务

- OTT和付费电视服务

- 其他服务(附加价值服务、漫游和国际服务、企业和批发服务等)

- 最终用户

- 公司

- 一般消费者

第六章 竞争情势

- 市场集中度

- 主要供应商的策略与投资动向(2023-2025)

- 2024年行动网路营运商市场占有率分析

- Product Benchmarking Analysis for mobile network services

- MNO snapshot(subscribers, churn rate, ARPU, etc.)

- 行动网路营运商公司简介*

- Viettel Group

- Vinaphone

- Mobifone Corporation

- Vietnamobile

- Gmobile

第七章 市场机会与未来展望

Vietnam Telecom MNO Market size in 2026 is estimated at USD 7.52 billion, growing from 2025 value of USD 7.22 billion with 2031 projections showing USD 9.21 billion, growing at 4.15% CAGR over 2026-2031.

Heightened data consumption, the nationwide 5G roll-out, and supportive government policies are steering the transition from voice to digital services while operators exploit premium enterprise offerings to counter falling voice revenue. Investments in edge computing, private 5G, and satellite-enabled rural access are broadening the addressable user base and underpinning steady top-line expansion across the Vietnam telecom MNO market. Price competition remains intense, yet disciplined infrastructure sharing contains opex and capex, preserving operating margins. A high concentration ratio-three state-backed carriers hold more than 95% of subscriptions-creates the scale needed for rapid technology upgrades and shields the Vietnam telecom MNO market from disruptive entrants.

Vietnam Telecom MNO Market Trends and Insights

Rapid 4G and 5G rollout drives mobile-data surge

Early 5G tests delivered median speeds of 364.43 Mbps in April 2025, propelling user demand for high-bandwidth services. The mandated sunset of 2G in 2026 and 3G in 2028 channels subscribers onto higher-value 4G and 5G plans, naturally lifting ARPU. Viettel captured 4 million 5G users within months, with 70% experiencing speeds above 1.5 Gbps, proving consumers will pay premiums for performance. Infrastructure sharing reduced deployment costs and enabled coverage in all 63 provinces. Surging traffic is spurring edge-computing nodes and CDNs, so carriers evolve into broader digital-infrastructure firms inside the Vietnam telecom MNO market.

National Digital Transformation programme accelerates broadband uptake

Government targets pushed fiber penetration to 82.4% of households by October 2024, already above the 2025 goal. Issuance of 20 million electronic ID cards in 2024 amplified demand for reliable broadband to access e-government services. A population database that handled 1.3 billion queries proves the scale of digital activity requiring sturdy networks. Forty-eight smart-city projects and Da Nang's semiconductor investments are transferring predictable traffic to carriers. Positive network effects emerge as each new digital service spurs further connectivity demand, assuring durable revenue expansion across the Vietnam telecom MNO market.

Intensifying price wars compress ARPU

Bandwidth upgrades at unchanged prices-FPT Telecom doubled speeds for residential users in April 2025-accelerated the decline in price-per-megabit. VNPT and Viettel replicated the strategy, pushing voice and SMS income lower as OTT apps dominate messaging. Operators chase cost efficiencies through network sharing, but sustained ARPU pressure forces a pivot toward enterprise and vertical solutions within the Vietnam telecom MNO market.

Other drivers and restraints analyzed in the detailed report include:

- Data-centre build-outs elevate wholesale fibre demand

- Private 5G/IoT adoption in manufacturing parks

- High spectrum costs and slow refarming

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Data and internet offerings captured 48.62% of Vietnam telecom MNO market share in 2025, confirming the structural pivot from voice to digital connectivity. IoT and M2M already produce the fastest 4.32% CAGR, and the Vietnam telecom MNO market size for that niche is projected to scale rapidly as factories automate and cities deploy smart-infrastructure platforms. Voice and SMS continue their secular decline, displaced by OTT messaging and calling. Pay-TV and bundled OTT video ride on expanded fibre footprints, accelerating household ARPU growth.

5G unlocks edge computing, AR/VR, and network slicing, giving carriers tools to price premium speeds and latency guarantees. Wholesale backhaul to hyperscale data centers adds high-margin accounts, while VAS such as digital wallets broaden cross-sell revenue. These adjacent income streams de-risk falling legacy cash flows, yet successful capture hinges on upgrading customer-experience platforms across the Vietnam telecom MNO market.

The Vietnam Telecom MNO Market is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, Iot and M2M Services, OTT and PayTV Services, Other Services), End User (Enterprises, Consumers). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

List of Companies Covered in this Report:

- Viettel Group

- Vinaphone

- Mobifone Corporation

- Vietnamobile

- Gmobile

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Regulatory and Policy Framework

- 4.3 Spectrum Landscape and Competitive Holdings

- 4.4 Telecom Industry Ecosystem

- 4.5 Macroeconomic and External Drivers

- 4.6 Porter's Five Forces

- 4.6.1 Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Bargaining Power of Buyers

- 4.6.5 Threat of Substitutes

- 4.7 Key MNO KPIs (2020-2025)

- 4.7.1 Unique Mobile Subscribers and Penetration Rate

- 4.7.2 Mobile Internet Users and Penetration Rate

- 4.7.3 SIM Connections by Access Technology and Penetration

- 4.7.4 Cellular IoT / M2M Connections

- 4.7.5 Broadband Connections (Mobile and Fixed)

- 4.7.6 ARPU (Average Revenue Per User)

- 4.7.7 Average Data Usage per Subscription (GB/month)

- 4.8 Market Drivers

- 4.8.1 Rapid 4G and 5G rollout drives mobile-data surge

- 4.8.2 National Digital Transformation programme accelerates broadband uptake

- 4.8.3 Smartphone affordability boosts data consumption

- 4.8.4 Data-centre build-outs elevate wholesale fibre demand

- 4.8.5 Private 5G/IoT adoption in manufacturing parks

- 4.8.6 Pay-TV fibre bundles lift household ARPU

- 4.9 Market Restraints

- 4.9.1 Intensifying price wars compress ARPU

- 4.9.2 High spectrum costs and slow refarming

- 4.9.3 Mountainous right-of-way costs stall rural fibre

- 4.9.4 Nascent MVNO rules delay service innovation

- 4.10 Technological Outlook

- 4.11 Analysis of key business models in Telecom

- 4.12 Analysis of Pricing Models and Pricing

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Overall Telecom Revenue and ARPU

- 5.2 Service Type

- 5.2.1 Voice Services

- 5.2.2 Data and Internet Services

- 5.2.3 Messaging Services

- 5.2.4 IoT and M2M Services

- 5.2.5 OTT and PayTV Services

- 5.2.6 Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.)

- 5.3 End-User

- 5.3.1 Enterprises

- 5.3.2 Consumer

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Investments by key vendors, 2023-2025

- 6.3 Market share analysis for MNOs, 2024

- 6.4 Product Benchmarking Analysis for mobile network services

- 6.5 MNO snapshot (subscribers, churn rate, ARPU, etc.)

- 6.6 Company Profiles* of MNOs (Includes Business Overview | Service Portfolio | Financials | Business Strategy and Recent Developments | SWOT Analysis)

- 6.6.1 Viettel Group

- 6.6.2 Vinaphone

- 6.6.3 Mobifone Corporation

- 6.6.4 Vietnamobile

- 6.6.5 Gmobile

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测

5G MVNO市场:按套餐类型、最终用户、设备类型、销售管道、产业和网路类型划分-2026-2032年全球市场预测 2026年全球行动虚拟网路营运商(MVNO)市场报告

2026年全球行动虚拟网路营运商(MVNO)市场报告 行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年

行动虚拟网路营运商 (MVNO) 市场规模、份额、趋势和预测:按类型、商业模式、服务类型、用户数量和地区划分,2026-2034 年 行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分

行动虚拟网路营运商 (MVNO) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分 东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)美国行动虚拟网路营运商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)

东协行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)亚太地区行动虚拟网路营运商(MVNO):市场占有率分析、产业趋势与统计、成长预测(2026-2031)新加坡电信行动网路业者:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031)美国电信行动网路营运商:市场占有率分析、产业趋势与统计数据、成长预测(2026-2031 年)美国行动虚拟网路营运商:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)