|

市场调查报告书

商品编码

1797829

蛋白质水解物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

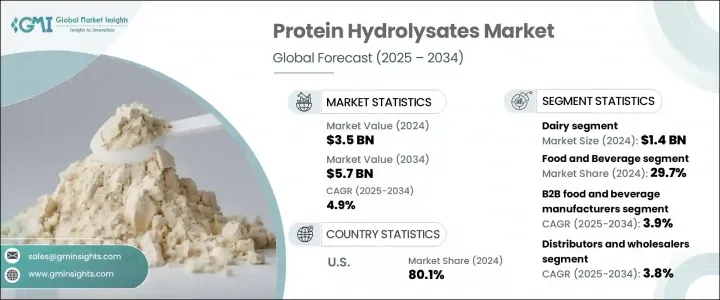

2024年,全球蛋白质水解物市场规模达35亿美元,预计2034年将以4.9%的复合年增长率成长至57亿美元。各行各业对功能性、易消化营养成分的需求日益增长,推动了该市场的扩张。蛋白质水解物来自植物、乳製品、动物和海洋蛋白等,因其高生物利用度和功能多样性而备受推崇。其快速吸收的特性使其在运动营养领域尤为重要,而婴儿营养领域则由于对低致敏性和易消化配方的需求不断增长而持续稳步增长。这些蛋白质也广泛应用于医疗营养、个人护理产品、医药级配方、动物饲料和宠物营养等领域。在众多生产技术中,酵素水解仍是主流方法,因其高效、能够生产高品质水解物且副产物较少而备受青睐。

儘管化学和微生物水解方法在生产具有特定功能或营养特性的客製化蛋白质水解物方面仍然发挥着重要作用,但它们往往受到副产物生成和反应环境控制较差的限制。热处理等物理方法虽然应用较少,但正在被重新审视,并采用新技术来减少蛋白质降解并提高反应效率。生物技术、精准发酵和膜分离领域的最新突破,使製造商能够在分子层面上微调水解物的成分。这些进步正在推动下一代水解物的开发,这些水解物将针对医疗营养、植物性运动恢復、个人化补充剂甚至化妆品配方等特定领域进行最佳化。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 35亿美元 |

| 预测值 | 57亿美元 |

| 复合年增长率 | 4.9% |

2024年,乳基蛋白水解物细分市场销售额达14亿美元,占40%。这些产品因其优异的吸收性和功能特性,主要用于婴儿配方奶粉、医疗营养和运动恢復产品。乳清和酪蛋白衍生物凭藉其卓越的营养特性,成为此细分市场表现的核心。此细分市场的优势源自于其高营养品质以及人们对蛋白质在各个生命阶段功效的日益重视。

2024年,婴儿营养品市场占据19.9%的市场份额,这得益于对传统乳蛋白敏感或过敏的婴儿对安全易消化的蛋白质来源的需求日益增长。由于消费者越来越关注无过敏原且肠道友善的替代品,婴儿配方奶粉中水解蛋白的使用持续成长。这个市场不仅受到监管政策的影响,也受到知情父母对注重健康的婴儿解决方案的强烈需求的影响。

2024年,美国蛋白质水解物市场占据80.1%的市场份额,贡献了10亿美元的市场规模。由于消费者对健康、科学食品的偏好,美国已成为蛋白质水解物领域成熟且创新驱动的市场。消化健康、肌肉恢復和免疫功能的日益增长趋势,进一步推动了不同蛋白质形式的发展。此外,人们对清洁标籤的期望值不断上升,以及人们对植物性替代品的兴趣日益浓厚,促使生产商在乳製品以外的领域进行创新。製造商正在推出更永续、生物可利用的蛋白质成分,以符合不断变化的消费者价值观。

全球蛋白质水解物市场的主要领导者包括嘉吉公司、戴维斯科食品国际公司、阿彻丹尼尔斯米德兰公司、恆天然合作社和爱氏晨曦食品配料公司。各大製造商正在利用研发投入,设计针对免疫支持、肠道健康和运动恢復等特定健康功能的水解物配方。与临床研究人员和配方专家的策略合作,使品牌能够增强生物活性,并针对目标应用客製化胜肽谱。领先的企业正在扩展其产品组合,推出不含乳製品和低过敏原的产品,以满足日益增长的清洁标籤和植物性趋势。此外,各公司正在透过增加本地采购、提高可追溯性和投资製程创新来增强供应链的韧性,以确保在已开发市场和新兴市场中产品品质始终如一,并实现具有成本效益的可扩展性。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 运动和临床营养产品需求不断成长

- 人们越来越喜欢植物性和无过敏原蛋白质

- 酶水解技术的进展

- 提高对蛋白质健康益处的认识

- 产业陷阱与挑战

- 生产成本高、加工方法复杂

- 食品成分的严格监管要求

- 市场机会

- 拓展功能性食品和饮料领域

- 营养保健品和个人化营养的成长

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按来源

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:按来源,2021 - 2034 年

- 主要趋势

- 乳製品

- 乳清

- 酪蛋白

- 牛奶

- 植物

- 大豆

- 豌豆

- 米

- 小麦

- 其他植物来源

- 动物

- 肉

- 胶原

- 蛋

- 海洋

- 鱼

- 海鲜

- 海洋

第六章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 食品和饮料

- 功能性食品

- 饮料

- 烘焙和糖果

- 乳製品及其替代品

- 肉类和肉类替代品

- 运动营养

- 粉末和补充剂

- 运动前后产品

- 恢復和耐力产品

- 体重管理产品

- 婴儿营养

- 临床和医学营养

- 动物饲料和宠物食品

- 化妆品和个人护理

- 药品和营养保健品

第七章:市场估计与预测:依生产方式,2021 - 2034 年

- 主要趋势

- 酵素

- 化学

- 微生物

- 新颖和新兴的方法

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- B2B食品和饮料製造商

- 营养保健品和补充品公司

- 製药公司

- 动物饲料和宠物食品製造商

- 化妆品和个人护理公司

- 研究和学术机构

- 直接面向消费者的品牌

第九章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 直销

- 分销商和批发商

- 线上B2B平台

- 其他的

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

- 埃及

第 11 章:公司简介

- Archer Daniels Midland Company (ADM)

- Arla Foods Ingredients

- Cargill, Incorporated

- Davisco Foods International

- Fonterra Co-operative Group Limited

- FrieslandCampina

- Glanbia plc

- Hilmar Ingredients

- Ingredia SA

- Kerry Group plc

The Global Protein Hydrolysates Market was valued at USD 3.5 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 5.7 billion by 2034. The growing demand for functional and easily digestible nutritional components across diverse sectors is fueling the expansion of this market. Protein hydrolysates are produced from sources such as plant, dairy, animal, and marine proteins, and are prized for their enhanced bioavailability and functional versatility. Their rapid absorption makes them especially valuable in sports nutrition, while the infant nutrition segment continues to grow steadily due to increasing demand for hypoallergenic and easily digestible formulas. These proteins are also widely used in areas like medical nutrition, personal care products, pharmaceutical-grade formulations, animal feeds, and pet nutrition. Among the various production techniques, enzymatic hydrolysis remains the dominant method, appreciated for its efficiency and ability to yield high-quality hydrolysates with fewer unwanted by-products.

Although chemical and microbial hydrolysis methods continue to play a role in producing customized protein hydrolysates with specific functional or nutritional attributes, they are often limited by by-product formation and less-controlled reaction environments. Physical methods such as thermal processing, while less widely adopted, are being revisited with new techniques that reduce protein degradation and improve reaction efficiency. Recent breakthroughs in biotechnology, precision fermentation, and membrane separation are now enabling manufacturers to fine-tune hydrolysate composition at a molecular level. These advances are driving the development of next-generation hydrolysates optimized for specialized sectors like medical nutrition, plant-based sports recovery, personalized supplements, and even cosmetic formulations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.5 Billion |

| Forecast Value | $5.7 Billion |

| CAGR | 4.9% |

The dairy-based protein hydrolysates segment generated USD 1.4 billion in 2024 and comprising 40% share. These products are primarily used in infant formulations, medical nutrition, and athletic recovery products due to their excellent absorption and functional characteristics. With their superior nutritional profile, whey and casein derivatives are central to the segment's performance. The segment's strength stems from high nutritional quality and increasing awareness around protein efficacy in various life stages.

The infant nutrition segment held 19.9% share in 2024, driven by the increasing need for protein sources that are both safe and digestible for infants with sensitivities or allergies to traditional milk proteins. The use of hydrolyzed proteins in baby formulas continues to grow due to heightened consumer focus on allergen-free and gut-friendly alternatives. This segment is shaped not only by regulatory policies but also by a stronger demand for health-conscious infant solutions from well-informed parents.

United States Protein Hydrolysates Market held 80.1% share in 2024, contributing USD 1 billion. The country has established itself as a mature and innovation-driven landscape for protein hydrolysates, supported by consumer preference for health-forward, science-backed food products. Growing trends in digestive health, muscle recovery, and immune function are further pushing development across different protein formats. Additionally, the rise in clean-label expectations and interest in plant-based alternatives is prompting producers to innovate beyond dairy-sourced proteins. Manufacturers are introducing more sustainable, bioavailable protein ingredients that align with evolving consumer values.

Key players leading the Global Protein Hydrolysates Market include Cargill, Incorporated, Davisco Foods International, Archer Daniels Midland Company, Fonterra Co-operative, and Arla Foods Ingredients. Major manufacturers are leveraging R&D investments to design hydrolysate formulations tailored to niche health functions such as immune support, gut health, and sports recovery. Strategic collaboration with clinical researchers and formulation specialists is allowing brands to enhance bioactivity and tailor peptide profiles for targeted applications. Leading players are expanding their product portfolios with dairy-free and allergen-reduced options to meet rising clean-label and plant-based trends. Additionally, companies are strengthening supply chain resilience by increasing local sourcing, improving traceability, and investing in processing innovation to ensure consistent product quality and cost-effective scalability in both developed and emerging markets.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Source

- 2.2.3 Application

- 2.2.4 Production method

- 2.2.5 End Use

- 2.2.6 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for sports and clinical nutrition products

- 3.2.1.2 Growing preference for plant-based and allergen-free proteins

- 3.2.1.3 Advancements in enzymatic hydrolysis technology

- 3.2.1.4 Increasing awareness of protein’s health benefits

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs and complex processing methods

- 3.2.2.2 Stringent regulatory requirements for food ingredients

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into functional foods and beverages segment

- 3.2.3.2 Growth in nutraceuticals and personalized nutrition

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By source

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Source, 2021 - 2034 (USD Bn, Units)

- 5.1 Key trends

- 5.2 Dairy

- 5.2.1 Whey

- 5.2.2 Casein

- 5.2.3 Milk

- 5.3 Plant

- 5.3.1 Soy

- 5.3.2 Pea

- 5.3.3 Rice

- 5.3.4 Wheat

- 5.3.5 Other plant sources

- 5.4 Animal

- 5.4.1 Meat

- 5.4.2 Collagen

- 5.4.3 Egg

- 5.5 Marine

- 5.5.1 Fish

- 5.5.2 Seafood

- 5.5.3 Marine

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Bn, Units)

- 6.1 Key trends

- 6.2 Food and beverages

- 6.2.1 Functional foods

- 6.2.2 Beverages

- 6.2.3 Bakery and confectionery

- 6.2.4 Dairy products and alternatives

- 6.2.5 Meat and meat alternatives

- 6.3 Sports nutrition

- 6.3.1 Powders and supplements

- 6.3.2 Pre- and post-workout products

- 6.3.3 Recovery and endurance products

- 6.3.4 Weight management products

- 6.4 Infant nutrition

- 6.5 Clinical and medical nutrition

- 6.6 Animal feed and pet food

- 6.7 Cosmetics and personal care

- 6.8 Pharmaceuticals and nutraceuticals

Chapter 7 Market Estimates & Forecast, By Production Method, 2021 - 2034 (USD Bn, Units)

- 7.1 Key trends

- 7.2 Enzymatic

- 7.3 Chemical

- 7.4 Microbial

- 7.5 Novel and emerging methods

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Bn, Units)

- 8.1 Key trends

- 8.2 B2B food and beverage manufacturers

- 8.3 Nutraceutical and supplement companies

- 8.4 Pharmaceutical companies

- 8.5 Animal feed and pet food manufacturers

- 8.6 Cosmetics and personal care companies

- 8.7 Research and academic institutions

- 8.8 Direct-to-consumer brands

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 (USD Bn, Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Distributors and wholesalers

- 9.4 Online B2B platforms

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Bn, units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 France

- 10.3.3 Italy

- 10.3.4 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Egypt

Chapter 11 Company Profiles

- 11.1 Archer Daniels Midland Company (ADM)

- 11.2 Arla Foods Ingredients

- 11.3 Cargill, Incorporated

- 11.4 Davisco Foods International

- 11.5 Fonterra Co-operative Group Limited

- 11.6 FrieslandCampina

- 11.7 Glanbia plc

- 11.8 Hilmar Ingredients

- 11.9 Ingredia SA

- 11.10 Kerry Group plc

蛋白质水解物市场规模、份额及成长分析(依产品类型、形态类型、应用类型及地区划分)-2026-2033年产业预测

蛋白质水解物市场规模、份额及成长分析(依产品类型、形态类型、应用类型及地区划分)-2026-2033年产业预测 全球蛋白质水解物市场规模、份额、趋势和成长分析报告(2026-2034)

全球蛋白质水解物市场规模、份额、趋势和成长分析报告(2026-2034) 有机蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)单细胞蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)精准发酵法製备蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)老年营养蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)下一代蛋白质水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034)

有机蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)单细胞蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)精准发酵法製备蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)老年营养蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)下一代蛋白质水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034) 蛋白质水解物市场-全球产业规模、份额、趋势、机会和预测,按类型、来源、形态、製程、应用、地区和竞争格局划分,2020-2030年预测非基因改造蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)食品废弃物衍生蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

蛋白质水解物市场-全球产业规模、份额、趋势、机会和预测,按类型、来源、形态、製程、应用、地区和竞争格局划分,2020-2030年预测非基因改造蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)食品废弃物衍生蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)