|

市场调查报告书

商品编码

1822633

植物蛋白水解物市场机会、成长动力、产业趋势分析及2025-2034年预测Plant Protein Hydrolysate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

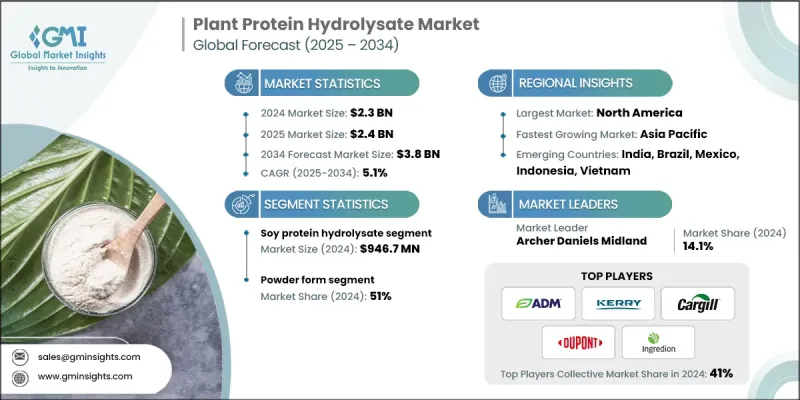

根据 Global Market Insights Inc. 发布的最新报告,全球植物蛋白水解物市场规模预计在 2024 年为 23 亿美元,预计将从 2025 年的 24 亿美元增长到 2034 年的 38 亿美元,复合年增长率为 5.1%。

消费者日益转向植物性饮食和清洁标籤产品,是植物蛋白水解物市场的主要驱动力。越来越多的人在选择饮食时优先考虑健康、可持续性和道德方面的考量,这导致对植物源性成分的需求激增。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 23亿美元 |

| 预测值 | 38亿美元 |

| 复合年增长率 | 5.1% |

大豆蛋白水解物的采用率不断上升

2024年,大豆蛋白水解物市场占据了显着份额,这得益于大豆丰富的氨基酸成分和广泛的可用性。作为一种用途广泛且经济高效的来源,大豆水解物广泛应用于运动营养、婴儿配方奶粉和功能性食品。其卓越的消化率和抗过敏特性使其在动物性替代品中占据绝对优势。市场参与者正在充分利用大豆蛋白的营养价值,同时投资于加工技术以减少苦味并提升风味,从而使大豆水解物对注重健康的消费者更具吸引力。

粉末获得牵引力

2024年,粉状产品占据了相当大的市场份额,这得益于其便利性、更长的保质期以及易于添加到各种食品和饮料产品中的优势。粉末为製造商提供了灵活性,使其能够配製从蛋白奶昔到烘焙食品的各种产品,而不会影响口感或营养成分。消费者也更青睐粉状水解物,因为它们便于携带,并且在日常饮食中可以直接使用。各公司正致力于改善粉状植物蛋白水解物的溶解度和口感,以拓宽其应用范围,并提高全球消费者的接受度。

北美将成为推动力地区

到2034年,北美植物蛋白水解物市场将迎来强劲成长,这得益于消费者对植物性营养和健康趋势的日益关注。製造商正利用与食品和饮料品牌的合作,创新并扩展符合北美口味和监管标准的产品组合。在研发方面的投资以及强调永续性和健康益处的行销策略,正在进一步增强其在该地区的市场影响力。

植物蛋白水解物市场的主要参与者有 Ingredion Incorporated、杜邦、阿彻丹尼尔斯米德兰公司 (ADM)、凯里集团和嘉吉。

为了巩固市场地位,植物蛋白水解物市场的企业正专注于产品创新,专注于改善风味和提高生物利用度。与食品製造商和营养品牌的策略合作,使其应用范围更广,市场渗透速度更快。扩大产能和采购可持续原料有助于满足日益增长的需求,同时契合消费者的价值观。此外,企业也投资于教育行销活动,以提高人们对植物蛋白水解物益处的认识,从而在竞争日益激烈的市场中推动其普及和客户忠诚度。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利格局

- 贸易统计资料(HS 编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考虑

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场规模与预测:依来源,2021-2034

- 主要趋势

- 大豆蛋白水解物

- 小麦蛋白水解物

- 豌豆蛋白水解物

- 米蛋白水解物

- 大麻蛋白水解物

- 葵花蛋白水解物

- 其他的

第六章:市场规模及预测:依形式,2021-2034

- 主要趋势

- 液体

- 粉末

第七章:市场规模与预测:按应用,2021-2034

- 主要趋势

- 食品和饮料

- 营养补充品

- 动物饲料

- 其他的

第 8 章:市场规模与预测:按地区,2021-2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- Archer Daniels Midland Company

- Kerry Group

- DuPont

- Ingredion Incorporated

- Cargill

- Evonik Industries

- Koninklijke DSM

- Glanbia

- Tate & Lyle

- Bunge Limited

- Roquette Freres

- Brenntag

- Associated British Foods

- Novozymes

- Givaudan

The global plant protein hydrolysate market was estimated at USD 2.3 billion in 2024 and is expected to grow from USD 2.4 billion in 2025 to USD 3.8 billion by 2034, at a CAGR of 5.1%, according to the latest report published by Global Market Insights Inc.

The increasing consumer shift toward plant-based diets and clean-label products is a major driver for the plant protein hydrolysate market. More people are prioritizing health, sustainability, and ethical considerations when choosing what to eat, leading to a surge in demand for plant-derived ingredients.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $3.8 Billion |

| CAGR | 5.1% |

Rising Adoption of Soy Protein Hydrolysate

The soy protein hydrolysate segment held a notable share in 2024, driven by soy's rich amino acid profile and widespread availability. As a versatile and cost-effective source, soy hydrolysates are extensively used in sports nutrition, infant formulas, and functional foods. Their superior digestibility and allergen-friendly nature position them well against animal-based alternatives. Market players are capitalizing on soy protein's nutritional benefits while investing in processing technologies to reduce bitterness and enhance flavor, making soy hydrolysates more appealing to health-conscious consumers.

Powder To Gain Traction

The powder form segment held a significant share in 2024, driven by its convenience, longer shelf life, and ease of incorporation into various food and beverage products. Powders provide manufacturers with the flexibility to formulate everything from protein shakes to bakery items without compromising texture or nutritional content. Consumers also prefer powdered hydrolysates for their portability and straightforward usage in daily diets. Companies are focusing on improving the solubility and taste profiles of powdered plant protein hydrolysates to broaden their application scope and increase consumer acceptance globally.

North America to Emerge as a Propelling Region

North America plant protein hydrolysate market will witness robust growth through 2034, fueled by increasing consumer awareness of plant-based nutrition and health trends. Manufacturers are leveraging partnerships with food and beverage brands to innovate and expand product portfolios tailored to North American tastes and regulatory standards. Investments in R&D and marketing strategies emphasizing sustainability and health benefits are further strengthening the market presence across the region.

Major players involved in the plant protein hydrolysate market are Ingredion Incorporated, DuPont, Archer Daniels Midland Company (ADM), Kerry Group, and Cargill.

To solidify their market foothold, companies in the plant protein hydrolysate market are emphasizing product innovation, focusing on flavor improvement and enhanced bioavailability. Strategic collaborations with food manufacturers and nutrition brands enable wider application and faster market penetration. Expanding production capacities and sourcing sustainable raw materials help meet rising demand while aligning with consumer values. Additionally, companies invest in educational marketing campaigns to raise awareness about the benefits of plant protein hydrolysates, thereby driving adoption and customer loyalty in an increasingly competitive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Source

- 2.2.2 Form

- 2.2.3 Application

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Soy protein hydrolysate

- 5.3 Wheat protein hydrolysate

- 5.4 Pea protein hydrolysate

- 5.5 Rice protein hydrolysate

- 5.6 Hemp protein hydrolysate

- 5.7 Sunflower protein hydrolysate

- 5.8 Others

Chapter 6 Market Size and Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Liquid

- 6.3 Powder

Chapter 7 Market Size and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Nutritional supplements

- 7.4 Animal feed

- 7.5 Others

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Archer Daniels Midland Company

- 9.2 Kerry Group

- 9.3 DuPont

- 9.4 Ingredion Incorporated

- 9.5 Cargill

- 9.6 Evonik Industries

- 9.7 Koninklijke DSM

- 9.8 Glanbia

- 9.9 Tate & Lyle

- 9.10 Bunge Limited

- 9.11 Roquette Freres

- 9.12 Brenntag

- 9.13 Associated British Foods

- 9.14 Novozymes

- 9.15 Givaudan

蛋白质水解物市场-全球产业规模、份额、趋势、机会和预测,按类型、来源、形态、製程、应用、地区和竞争格局划分,2020-2030年预测

蛋白质水解物市场-全球产业规模、份额、趋势、机会和预测,按类型、来源、形态、製程、应用、地区和竞争格局划分,2020-2030年预测 婴儿配方奶粉蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)清真认证蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)免疫调节蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)抗菌(酵素法)蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)海洋蛋白水解物市场机会、成长动力、产业趋势分析及2025-2034年预测蛋白质水解物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

婴儿配方奶粉蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)清真认证蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)免疫调节蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)抗菌(酵素法)蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)海洋蛋白水解物市场机会、成长动力、产业趋势分析及2025-2034年预测蛋白质水解物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球蛋白质水解物市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测抗菌(酵素)蛋白水解物市场机会、成长动力、产业趋势分析与预测 2025 - 2034蛋白质水解物的全球市场

全球蛋白质水解物市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测抗菌(酵素)蛋白水解物市场机会、成长动力、产业趋势分析与预测 2025 - 2034蛋白质水解物的全球市场