|

市场调查报告书

商品编码

1885855

精准发酵法製备蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Precision Fermentation-Based Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

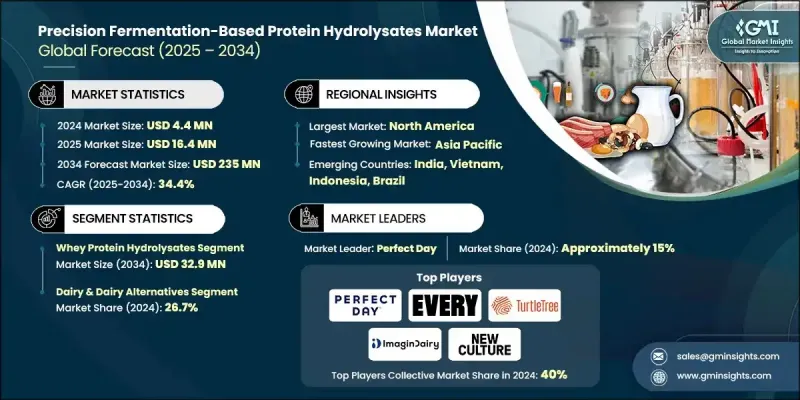

2024 年全球精准发酵蛋白水解物市场价值为 440 万美元,预计到 2034 年将以 34.4% 的复合年增长率增长至 2.35 亿美元。

市场发展势头正因多种因素的共同作用而加速,其中包括监管方面的进展,这些进展为新型精准发酵蛋白作为水解物生产的基础原料进入商业渠道铺平了道路。年产能超过10万公升的大型发酵厂正在陆续投产,显着提升了供应潜力。随着製程优化和规模化效率的提高,生产成本预计将越来越有竞争力,与传统蛋白质来源相比更具优势。同时,随着营养、食品技术和製药业的公司将精准发酵水解物整合到新产品线中,其应用范围也不断扩大。这些水解物在婴幼儿营养、医疗配方、健康生活方式补充剂、功能性食品配料、化妆品应用和特种动物营养等领域都具有巨大的应用潜力,蕴藏着巨大的收入机会。此外,这些水解物也被设计用于提供具有抗氧化、抗菌、降血压、矿物质结合或免疫支持等功效的生物活性化合物,这些功效已透过临床研究证实,进一步提升了这些优质原料的差异化优势。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 440万美元 |

| 预测值 | 2.35亿美元 |

| 复合年增长率 | 34.4% |

预计2034年,乳清蛋白水解物市场规模将达3,290万美元,年复合成长率(CAGR)预估为30.3%。由于其在运动营养、婴幼儿配方奶粉和功能性食品等领域的长期应用,该细分市场是蛋白质来源中最成熟的。其主要蛋白质组分具有显着的功能特性,包括有效的起泡性、乳化性和凝胶形成性,这些特性通常可透过标靶水解而增强。

2024年,乳製品及乳製品替代品市占率为26.7%,预计2025年至2034年间将以29.2%的复合年增长率成长。该领域仍是最大的应用领域,因为消费者熟悉乳蛋白,而生产商则依赖这些蛋白在饮料、发酵乳製品、冷冻甜点和其他富含蛋白质的食品中的功能性表现。日益增多的产业合作将继续推动精准发酵水解物在主流消费品中的应用。

2024年,北美精准发酵蛋白水解物市场预计将占据41.9%的市场份额,这主要得益于先进的生物技术环境、有利的监管路径以及众多专注于精准发酵的企业的强大实力。在美国,简化的监管流程使得许多申请者能够在大约10-12个月内完成审批流程,而其他一些地区的审批时间则要长得多。

精准发酵蛋白水解物市场的主要活跃企业包括Change Foods、Clara Foods、Cubiq Foods、Formo、Fybraworks Foods、Geltor、Helaina、Imagindairy、Jellatech、Modern Meadow、Motif FoodWorks、New Culture、Onego Bio、Perfect Day、Provectus AltoYuectus AlMmil、Spikid、Spifect Day、Provectus Albid、Ekot、SpiberTree、SpiFal、Treek、TheYat、Treek、Ek。这些企业正致力于巩固其在精准发酵蛋白水解物市场的地位,并实施以扩大生产规模、提高成本效益和加速产品创新为重点的策略。许多企业正在投资高产能发酵系统以提高产量,同时改善下游加工流程以提高纯度和产率。与食品、营养和生物技术公司的策略合作有助于拓展应用开发并确保长期市场需求。此外,企业还优先考虑监管合规,以缩短审批週期并扩大市场准入。此外,各公司正在对具有特殊功能和生物活性特征的蛋白质和水解物进行工程改造,以创造差异化、高利润的产品线,从而支持竞争地位。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按类型

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计

- 主要进口国

- 主要出口国(註:仅提供重点国家的贸易统计)

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依类型划分,2021-2034年

- 主要趋势

- 酪蛋白水解物

- 乳清蛋白水解物

- 乳铁蛋白水解物

- 卵清蛋白水解物

- 卵子黏液水解物

- 肌红蛋白水解物

- 豆血红素水解物

- 胶原蛋白水解物

- 弹性蛋白水解物

- 酵素水解物

- 生长因子水解物

- 功能性胜肽浓缩物

- 微生物蛋白水解物

- 其他的

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 乳製品及乳製品替代品

- 液态奶及乳製品替代品

- 全脂牛奶替代品

- 脱脂和低脂牛奶替代品

- 风味牛奶替代品

- 咖啡师级牛奶替代品

- 起司替代品

- 马苏里拉起司(披萨、餐饮服务)

- 切达干酪和硬质奶酪

- 奶油乳酪和软乳酪

- 加工乳酪製品

- 优格及发酵替代品

- 希腊式优格

- 可饮用优格

- 益生菌配方

- 冰淇淋和冷冻甜点

- 高级冰淇淋

- 冷冻优格

- 新奇商品和酒吧

- 奶油、奶油和抹酱的替代品

- 乳製品成分替代品

- 乳清蛋白替代品

- 酪蛋白酸盐替代品

- 牛奶蛋白分离物替代品

- 液态奶及乳製品替代品

- 烘焙和糖果

- 麵包和捲饼

- 三明治麵包

- 手工麵包

- 麵包捲和麵包卷

- 蛋糕和糕点

- 千层蛋糕

- 鬆饼和纸杯蛋糕

- 丹麦酥和羊角麵包

- 饼干和曲奇

- 蛋液替代品

- 糖果及甜点应用

- 棉花糖和牛轧糖(充气器、质地)

- 软糖和果冻(胶原蛋白,营养强化)

- 巧克力及涂层(牛奶蛋白替代品)

- 麵包和捲饼

- 饮料

- 蛋白质水

- 清澈的蛋白质水

- 电解质和功能性水

- 运动及能量饮料

- 等渗透压饮料

- 富含蛋白质的能量饮料

- 训练前/训练中饮料

- 即饮蛋白奶昔

- 植物性蛋白质奶昔

- 清澈的即饮蛋白奶昔

- 代餐

- 果汁和低pH值饮料

- 混合果汁

- 碳酸饮料

- 酸性官能基

- 酒精应用

- 啤酒(稳定剂)

- 葡萄酒(澄清剂)

- 加入蛋白质的酒精饮料

- 蛋白质水

- 肉类、海鲜及烹饪应用

- 植物肉应用

- 汉堡和肉饼

- 整块肉(牛排、鸡肉製品)

- 结构化肉品替代品

- 肌红蛋白/血红素用于调味和香气

- 人造肉培养基及投入物

- 生长因子(IGF、FGF、TGF-α)

- 血清和胺基酸替代品

- 支架蛋白(胶原蛋白、细胞外基质类似物)

- 海鲜替代品

- 鳍鱼(鲔鱼、鲑鱼类似物)

- 甲壳类(虾、蟹)

- 烹饪应用(一般咸味)

- 汤类和肉汤(乳製品/肉类替代品)

- 酱汁、肉汁和乳化剂

- 调味品和佐料

- 速食、即食食品、方便食品

- 植物肉应用

- 运动与积极生活方式营养

- 蛋白质粉

- 发酵乳清类似物

- 发酵酪蛋白和鸡蛋类似物

- 多源混合

- 功能性蛋白棒和零食

- 恢復和耐力产品

- 以支链胺基酸(BCAA)为重点的产品

- 肌肉/关节/免疫益处

- 运动后饮料冲剂

- 清洁标籤和高性能水溶性物质

- 蛋白质粉

- 医学与临床营养

- 基于胜肽的肠内营养配方

- 半元素

- 元素

- 口服医学营养

- 癌症、慢性阻塞性肺病、老年病

- 治疗应用

- 肝肾饮食

- 免疫支持

- 术后恢復

- 药理胜肽

- 费雪比率寡肽

- 免疫调节水解物

- 基于胜肽的肠内营养配方

- 婴幼儿营养

- 婴儿配方奶粉(0-6个月)

- 部分水解

- 深度水解

- 胺基酸基

- 后续配方奶粉和幼儿配方奶粉(6-24个月)

- 水解后续

- 成长奶粉

- CMP过敏及低过敏产品

- 乳铁蛋白和生物活性胜肽

- 免疫和肠道功能支持

- 婴儿配方奶粉(0-6个月)

- 膳食补充剂与功能性健康

- 膳食蛋白质补充剂

- 粉剂、胶囊

- 蛋白质注射液

- 功能性软糖和饮料

- 按功能分类的生物活性胜肽

- 心血管支持(ACE抑制剂)

- 抗氧化剂

- 抗菌剂

- 免疫调节剂

- 认知/压力支持胜肽

- 膳食蛋白质补充剂

- 药妆品及个人护理

- 保养品

- 促进胶原蛋白生成的乳霜

- 抗老精华液

- 保湿霜和眼霜

- 头髮和头皮产品

- 水溶性角蛋白型蛋白质

- 头髮修復胜肽

- 口腔及牙齿护理

- 胜肽漱口水

- 口腔卫生补充剂

- 保养品

- 动物营养

- 宠物食品(犬猫)

- 高蛋白干粮、湿粮、点心

- 水产饲料

- 鲑鱼、虾、鳟鱼-促进消化的胜肽

- 牲畜饲料添加剂

- 猪、家禽、反刍动物性能

- 免疫和肠道健康胜肽

- 宠物食品(犬猫)

- 製药与生物治疗

- 治疗性胜肽(例如,GLP-1类似物)

- 生物类似胜肽

- 基于胜肽的活性药物成分

- 药物递送胜肽支架

- 伤口癒合与再生疗法

- 抗菌及局部用药

第七章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第八章:公司简介

- Change Foods

- Clara Foods

- Cubiq Foods

- Formo

- Fybraworks Foods

- Geltor

- Helaina

- Imagindairy

- Jellatech

- Modern Meadow

- Motif FoodWorks

- New Culture

- Onego Bio

- Perfect Day

- Provectus Algae

- Remilk

- Spiber

- The EVERY Company

- TurtleTree

- Vivici

- Others

The Global Precision Fermentation-Based Protein Hydrolysates Market was valued at USD 4.4 million in 2024 and is estimated to grow at a CAGR of 34.4% to reach USD 235 million by 2034.

Market momentum is accelerating due to multiple reinforcing factors, including regulatory progress that is opening the door for novel precision-fermented proteins to enter commercial channels as foundational materials for hydrolysate production. Large-capacity fermentation plants exceeding 100,000 liters are being brought online, significantly boosting supply potential. As optimization improves and scaling efficiencies advance, production costs are expected to become increasingly competitive with conventional protein sources. At the same time, application development is broadening as companies in nutrition, food technologies, and pharmaceuticals integrate precision-fermented hydrolysates into new product pipelines. Revenue opportunities span high-value uses across infant nutrition, medical formulations, active lifestyle supplements, functional food ingredients, cosmetic applications, and specialty animal nutrition. These hydrolysates are also being designed to deliver bioactive compounds that have demonstrated benefits such as antioxidant, antimicrobial, antihypertensive, mineral-binding, or immune-supportive effects through clinical findings, adding further differentiation to these premium ingredients.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.4 Million |

| Forecast Value | $235 Million |

| CAGR | 34.4% |

The whey protein hydrolysates segment is expected to reach USD 32.9 million by 2034 at a projected CAGR of 30.3%. This segment is the most established among protein sources due to long-standing use across sports nutrition, infant formulations, and functional food applications. Its primary protein fraction offers notable functional properties, including effective foaming, emulsification, and gel formation, which are often enhanced through targeted hydrolysis.

The dairy and dairy alternatives segment held a 26.7% share in 2024 and is anticipated to grow at a 29.2% CAGR between 2025 and 2034. This category remains the largest application area because consumers are familiar with dairy proteins and manufacturers rely on the functional performance of these proteins in beverages, cultured dairy items, frozen desserts, and other protein-enriched foods. Growing industry collaborations continue to support higher adoption of precision-fermented hydrolysates across mainstream consumer products.

North America Precision Fermentation-Based Protein Hydrolysates Market captured 41.9% share in 2024, supported by an advanced biotechnology landscape, favorable regulatory pathways, and a strong presence of companies specializing in precision fermentation. In the United States, a streamlined regulatory route allows many applicants to move through approval stages in roughly 10-12 months, compared with longer timelines in certain other regions.

Key companies active in the Precision Fermentation-Based Protein Hydrolysates Market include Change Foods, Clara Foods, Cubiq Foods, Formo, Fybraworks Foods, Geltor, Helaina, Imagindairy, Jellatech, Modern Meadow, Motif FoodWorks, New Culture, Onego Bio, Perfect Day, Provectus Algae, Remilk, Spiber, The EVERY Company, TurtleTree, and Vivici. Companies strengthening their foothold in the Precision Fermentation-Based Protein Hydrolysates Market are implementing strategies focused on scaling production, improving cost efficiency, and accelerating product innovation. Many organizations are investing in high-capacity fermentation systems to increase output while refining downstream processing to raise purity and yield. Strategic collaborations with food, nutrition, and biotech firms are helping expand application development and secure long-term demand. Businesses are also prioritizing regulatory readiness to shorten approval cycles and enhance market access. In addition, firms are engineering proteins and hydrolysates with specialized functional and bioactive profiles to create differentiated, high-margin product lines that support competitive positioning.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries ( Note: the trade statistics will be provided for key countries only)

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Casein Hydrolysates

- 5.3 Whey Protein Hydrolysates

- 5.4 Lactoferrin Hydrolysates

- 5.5 Ovalbumin Hydrolysates

- 5.6 Ovomucoid Hydrolysates

- 5.7 Myoglobin Hydrolysates

- 5.8 Leghemoglobin Hydrolysates

- 5.9 Collagen Hydrolysates

- 5.10 Elastin Hydrolysates

- 5.11 Enzyme Hydrolysates

- 5.12 Growth Factor Hydrolysates

- 5.13 Functional Peptide Concentrates

- 5.14 Microbial Protein Hydrolysates

- 5.15 Others

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Dairy & Dairy Alternatives

- 6.2.1 Fluid Milk & Milk Alternatives

- 6.2.1.1 Whole Milk Analogues

- 6.2.1.2 Skim & Low-Fat Milk Analogues

- 6.2.1.3 Flavored Milk Alternatives

- 6.2.1.4 Barista-Grade Milk Alternatives

- 6.2.2 Cheese Analogues

- 6.2.2.1 Mozzarella (Pizza, Food Service)

- 6.2.2.2 Cheddar & Hard Cheeses

- 6.2.2.3 Cream Cheese & Soft Cheeses

- 6.2.2.4 Processed Cheese Products

- 6.2.3 Yogurt & Fermented Alternatives

- 6.2.3.1 Greek-Style Yogurt

- 6.2.3.2 Drinkable Yogurt

- 6.2.3.3 Probiotic Formulations

- 6.2.4 Ice Cream & Frozen Desserts

- 6.2.4.1 Premium Ice Cream

- 6.2.4.2 Frozen Yogurt

- 6.2.4.3 Novelties & Bars

- 6.2.5 Cream, Butter & Spread Alternatives

- 6.2.6 Dairy Ingredient Replacers

- 6.2.6.1 Whey Protein Replacers

- 6.2.6.2 Caseinate Replacers

- 6.2.6.3 Milk Protein Isolate Replacers

- 6.2.1 Fluid Milk & Milk Alternatives

- 6.3 Bakery & Confectionery

- 6.3.1 Bread & Rolls

- 6.3.1.1 Sandwich Bread

- 6.3.1.2 Artisan Breads

- 6.3.1.3 Buns & Rolls

- 6.3.2 Cakes & Pastries

- 6.3.2.1 Layer Cakes

- 6.3.2.2 Muffins & Cupcakes

- 6.3.2.3 Danish & Croissants

- 6.3.3 Cookies & Biscuits

- 6.3.4 Egg Wash Replacers

- 6.3.5 Confectionery & Sweet Applications

- 6.3.5.1 Marshmallows & Nougat (Aerators, Texture)

- 6.3.5.2 Gummies & Jellies (Collagen, Fortification)

- 6.3.5.3 Chocolate & Coatings (Milk Protein Replacers)

- 6.3.1 Bread & Rolls

- 6.4 Beverages

- 6.4.1 Protein Waters

- 6.4.1.1 Clear Protein Waters

- 6.4.1.2 Electrolyte & Functional Waters

- 6.4.2 Sports & Energy Drinks

- 6.4.2.1 Isotonic Drinks

- 6.4.2.2 Protein-Enriched Energy Drinks

- 6.4.2.3 Pre-Workout/Intra-Workout Drinks

- 6.4.3 RTD Protein Shakes

- 6.4.3.1 Plant-Based Protein Shakes

- 6.4.3.2 Clear RTD Protein Shakes

- 6.4.3.3 Meal Replacements

- 6.4.4 Juice & Low pH Beverages

- 6.4.4.1 Juice Blends

- 6.4.4.2 Carbonated Beverages

- 6.4.4.3 Acidic Functionals

- 6.4.5 Alcoholic Applications

- 6.4.5.1 Beer (Stabilizers)

- 6.4.5.2 Wine (Fining Agents)

- 6.4.5.3 Protein-Fortified Alcoholic Beverages

- 6.4.1 Protein Waters

- 6.5 Meat, Seafood & Culinary Applications

- 6.5.1 Plant-Based Meat Applications

- 6.5.1.1 Burgers & Patties

- 6.5.1.2 Whole Cuts (Steaks, Chicken Analogues)

- 6.5.1.3 Structured Meat Alternatives

- 6.5.1.4 Myoglobin/Heme for Flavor & Aroma

- 6.5.2 Cultivated Meat Media & Inputs

- 6.5.2.1 Growth Factors (IGF, FGF, TGF-a)

- 6.5.2.2 Serum & Amino Acid Replacers

- 6.5.2.3 Scaffold Proteins (Collagen, ECM analogues)

- 6.5.3 Seafood Analogues

- 6.5.3.1 Finfish (Tuna, Salmon analogues)

- 6.5.3.2 Crustaceans (Shrimp, Crab)

- 6.5.4 Culinary Applications (General Savory)

- 6.5.4.1 Soups & Broths (Dairy/Meat analogues)

- 6.5.4.2 Sauces, Gravies & Emulsions

- 6.5.4.3 Dressings and Condiments

- 6.5.4.4 Instant Meals, RTE, Convenience Foods

- 6.5.1 Plant-Based Meat Applications

- 6.6 Sports & Active Lifestyle Nutrition

- 6.6.1 Protein Powders

- 6.6.1.1 Fermented Whey Analogues

- 6.6.1.2 Fermented Casein & Egg Analogues

- 6.6.1.3 Multi-Source Blends

- 6.6.2 Functional Protein Bars & Snacks

- 6.6.3 Recovery & Endurance Products

- 6.6.3.1 BCAA-Focused Products

- 6.6.3.2 Muscle/Joint/Immune Benefits

- 6.6.3.3 Post-Workout Drink Mixes

- 6.6.4 Clean Label & Performance Hydrosolubles

- 6.6.1 Protein Powders

- 6.7 Medical & Clinical Nutrition

- 6.7.1 Peptide-Based Enteral Formulas

- 6.7.1.1 Semi-Elemental

- 6.7.1.2 Elemental

- 6.7.2 Oral Medical Nutrition

- 6.7.2.1 Cancer, COPD, Geriatric

- 6.7.3 Therapeutic Applications

- 6.7.3.1 Hepatic/renal diets

- 6.7.3.2 Immune support

- 6.7.3.3 Post-surgical recovery

- 6.7.4 Pharmacological Peptides

- 6.7.4.1 Fischer Ratio Oligopeptides

- 6.7.4.2 Immune-modulating Hydrolysates

- 6.7.1 Peptide-Based Enteral Formulas

- 6.8 Infant & Pediatric Nutrition

- 6.8.1 Infant Formula (0-6 months)

- 6.8.1.1 Partially Hydrolyzed

- 6.8.1.2 Extensively Hydrolyzed

- 6.8.1.3 Amino Acid-Based

- 6.8.2 Follow-On & Toddler Formula (6-24 months)

- 6.8.2.1 Hydrolyzed Follow-On

- 6.8.2.2 Growing-Up Milk

- 6.8.3 CMP-Allergy and Hypoallergenic Products

- 6.8.4 Lactoferrin & Bioactive Peptides

- 6.8.4.1 Immune and Gut Function Support

- 6.8.1 Infant Formula (0-6 months)

- 6.9 Dietary Supplements & Functional Wellness

- 6.9.1 Dietary Protein Supplements

- 6.9.1.1 Powders, Capsules

- 6.9.1.2 Protein Shots

- 6.9.2 Functional Gummies & Beverages

- 6.9.3 Bioactive Peptides by Function

- 6.9.3.1 Cardiovascular Support (ACE inhibitors)

- 6.9.3.2 Antioxidants

- 6.9.3.3 Antimicrobials

- 6.9.3.4 Immune-Modulators

- 6.9.3.5 Cognitive / Stress Support Peptides

- 6.9.1 Dietary Protein Supplements

- 6.10 Cosmeceuticals & Personal Care

- 6.10.1 Skincare Products

- 6.10.1.1 Collagen-Boosting Creams

- 6.10.1.2 Anti-Aging Serums

- 6.10.1.3 Moisturizers & Eye Creams

- 6.10.2 Hair & Scalp Products

- 6.10.2.1 Hydrosoluble Keratin-style Proteins

- 6.10.2.2 Hair Repair Peptides

- 6.10.3 Oral & Dental Care

- 6.10.3.1 Peptide Mouthwashes

- 6.10.3.2 Oral Hygiene Supplements

- 6.10.1 Skincare Products

- 6.11 Animal Nutrition

- 6.11.1 Pet Food (Dogs & Cats)

- 6.11.1.1 Protein-Enhanced Kibble, Wet Food, Treats

- 6.11.2 Aquaculture Feed

- 6.11.2.1 Salmon, Shrimp, Trout - Digestibility-enhancing Peptides

- 6.11.3 Livestock Feed Additives

- 6.11.3.1 Swine, Poultry, Ruminant Performance

- 6.11.3.2 Immune & Gut Health Peptides

- 6.11.1 Pet Food (Dogs & Cats)

- 6.12 Pharmaceuticals & Biotherapeutics

- 6.12.1 Therapeutic Peptides (e.g., GLP-1 analogues)

- 6.12.2 Biosimilar Peptides

- 6.12.3 Peptide-based APIs

- 6.12.4 Drug Delivery Peptide Scaffolds

- 6.12.5 Wound Healing & Regenerative Therapies

- 6.12.6 Antimicrobial & Topical Therapeutics

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Change Foods

- 8.2 Clara Foods

- 8.3 Cubiq Foods

- 8.4 Formo

- 8.5 Fybraworks Foods

- 8.6 Geltor

- 8.7 Helaina

- 8.8 Imagindairy

- 8.9 Jellatech

- 8.10 Modern Meadow

- 8.11 Motif FoodWorks

- 8.12 New Culture

- 8.13 Onego Bio

- 8.14 Perfect Day

- 8.15 Provectus Algae

- 8.16 Remilk

- 8.17 Spiber

- 8.18 The EVERY Company

- 8.19 TurtleTree

- 8.20 Vivici

- 8.21 Others

蛋白质水解物市场规模、份额及成长分析(依产品类型、形态类型、应用类型及地区划分)-2026-2033年产业预测

蛋白质水解物市场规模、份额及成长分析(依产品类型、形态类型、应用类型及地区划分)-2026-2033年产业预测 全球蛋白质水解物市场规模、份额、趋势和成长分析报告(2026-2034)

全球蛋白质水解物市场规模、份额、趋势和成长分析报告(2026-2034) 有机蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)单细胞蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)老年营养蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)下一代蛋白质水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034)

有机蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)单细胞蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)老年营养蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)下一代蛋白质水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034) 蛋白质水解物市场-全球产业规模、份额、趋势、机会和预测,按类型、来源、形态、製程、应用、地区和竞争格局划分,2020-2030年预测非基因改造蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)食品废弃物衍生蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)发酵蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

蛋白质水解物市场-全球产业规模、份额、趋势、机会和预测,按类型、来源、形态、製程、应用、地区和竞争格局划分,2020-2030年预测非基因改造蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)食品废弃物衍生蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)发酵蛋白水解物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)