|

市场调查报告书

商品编码

1636270

北美电动车电池材料:市场占有率分析、行业趋势和成长预测(2025-2030)North America Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

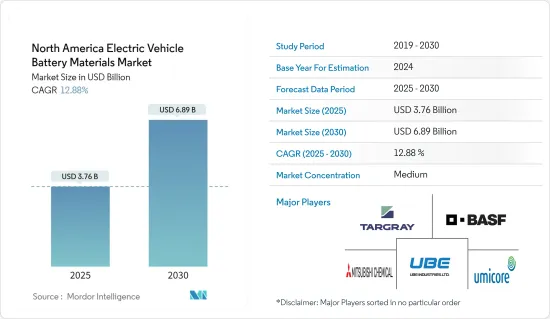

北美电动车电池材料市场规模预计到2025年为37.6亿美元,预计2030年将达到68.9亿美元,预测期内(2025-2030年)复合年增长率为12.88%。

主要亮点

- 未来几年,北美电动车电池材料市场预计将受到电动车销量激增和政府政策法规收紧的显着推动。

- 相反,北美电动车电池材料市场因国内原料生产不足而高度依赖进口,面临挑战。

- 儘管如此,我们仍在继续努力开发先进的电池技术。预计这一因素将在未来几年在市场上创造一些机会。

- 美国凭藉其强劲的汽车製造和销售业,将主导成长前景,并可能在预测期内实现最高的扩张。

北美电动车电池材料市场趋势

锂离子电池占市场主导地位

- 锂离子电池产业是北美电动车(EV)电池材料市场的基石,其特点是在电动车技术的成长和进步中发挥关键作用。作为电动车最广泛采用的电池类型,锂离子电池兼具能量密度、效率和寿命的优势,使其成为现代电动车应用的关键。

- 过去十年电池技术和製造流程的显着进步推动了电动车市场中锂离子电池的采用。这些进步不仅降低了成本,还提高了性能和可靠性,使锂离子电池对製造商和消费者越来越有吸引力。

- 近年来,锂离子电池和电池组的价格一直呈下降趋势,这使得它们对终端用户产业更具吸引力。经历2022年价格小幅上涨后,2023年电池价格将再次呈现下降趋势。锂离子电池组成本下降14%,达到139美元/kWh的历史低点。

- 该领域包括各种各样的材料,每种材料都有助于电池的整体性能和功能。选择这些材料是因为它们能够提高电池能量密度、循环寿命和热稳定性,满足汽车产业所需的关键性能参数。例如,富镍阴极材料由于其高能量容量而特别优选,这直接转化为电动车更长的行驶里程。

- 该地区对电动车的需求不断增长,导致对锂离子电池的需求大幅增加。因此,电池製造商和组装商现在正在投资电池材料的生产设施。这项策略性倡议旨在满足国内外对锂电池日益增长的需求。此外,电池技术的进步也进一步推动了需求。随着电动车变得越来越流行,预计该市场将继续成长。

- 例如,2023 年 10 月,电动车电池材料领域的主要参与者 Umicore 透过建立 CAM 和 pCAM 工厂,巩固了在加拿大安大略省的业务。该公司正在安大略省Loyalist积极建造35GWh电池材料生产设施,以服务快速成长的北美电动车(EV)市场。

- 优美科获得了加拿大政府和安大略省政府的支持,认识到该工厂将在加强该地区的电动车供应链和加强整体电动车电池格局方面发挥关键作用,我们已获得了重要的财政支持。

- 因此,如上所述,锂离子电池领域预计将在预测期内主导市场。

美国正在经历显着成长

- 在美国,由于消费者偏好、环保意识以及减少温室气体排放的监管压力,电动车的需求正在稳步增长。联邦和州级的奖励,例如电动车购买的税额扣抵和退税,在加速电动车的普及方面发挥重要作用。

- 2024 年,您可以获得高达 7,500 美元的税额扣抵,二手电动车的购买者可以获得高达 4,000 美元的税额扣抵。今年的一个显着变化是,消费者现在可以将此税额扣抵转移给合格的经销商,并在购买车辆时立即获得折扣。

- 这些激励措施不仅使电动车更容易为消费者所接受,而且刺激了对先进电池技术和材料的需求。此外,美国政府承诺在2050年实现净零排放,以及一项包括对电动车充电网路和清洁能源倡议进行大量投资的基础设施法案,将进一步推动电动车市场的发展,因此预计对电池材料的需求也将增加。

- 这些激励措施正在刺激电动车在该国的快速普及。特别是,国际能源总署(IEA)报告称,电动车普及率在过去十年中稳步增长。具体来说,2022年至2023年,电池式电动车销量激增37.5%以上。考虑到过去五年 71.6% 的复合年增长率,这一增长更加令人印象深刻。这些数字证实了人们对电动车日益增长的兴趣,从而提振了国内电池需求。

- 对国内电池製造能力的大量投资也是美国市场的特征。有鑑于减少对外国供应链依赖的战略重要性,私人公司和政府机构都在大力投资发展国内电池製造设施。特斯拉、通用汽车、现代汽车和福特等公司正带头建立超级工厂,大规模生产锂离子电池。

- 例如,2023年4月,两家知名汽车製造商宣布计划在美国建造电动车(EV)电池工厂,展示了美国电动车製造业的持续快速成长。通用汽车宣布将与三星SDI合作投资30亿美元在美国建造电动车电池工厂。同时,现代汽车透露与韩国电池製造商SK On建立合作关係,承诺出资50亿美元在乔治亚设立电池工厂。

- 这些设施旨在利用先进的製造技术和自动化来提高生产效率、降低成本并确保为国内市场稳定供应高品质的电池。

- 因此,如前所述,美国预计在预测期内将出现强劲成长。

北美电动汽车电池材料产业概况

北美电动车电池材料市场适度分散。该市场的主要企业(排名不分先后)包括Targray Technology International Inc.、 BASF SE、Mitsubishi Chemical Group Corporation、UBE Corporation 和Umicore。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2029年之前的市场规模与需求预测(单位:美元)

- 最新趋势和发展

- 政府法规政策

- 市场动态

- 促进因素

- 电动车销量成长

- 政府扶持政策及政策

- 抑制因素

- 原物料供应依赖进口

- 促进因素

- 供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品/服务的威胁

- 竞争公司之间的敌对关係

- 投资分析

第五章市场区隔

- 依电池类型

- 锂离子电池

- 铅酸电池

- 其他的

- 按材质

- 阴极

- 阳极

- 电解

- 分隔符

- 其他的

- 按地区

- 美国

- 加拿大

- 其他北美地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Targray Technology International Inc.

- BASF SE

- Mitsubishi Chemical Group Corporation

- UBE Corporation

- Umicore

- Sumitomo Chemical Co., Ltd.

- Nichia Corporation

- ENTEK International LLC

- Arkema SA

- Kureha Corporation

- List of Other Prominent Companies

- Market Ranking/Share(%)Analysis

第七章市场机会与未来趋势

- 电池技术的进步

简介目录

Product Code: 50003557

The North America Electric Vehicle Battery Materials Market size is estimated at USD 3.76 billion in 2025, and is expected to reach USD 6.89 billion by 2030, at a CAGR of 12.88% during the forecast period (2025-2030).

Key Highlights

- In the coming years, the North America Electric Vehicle Battery Materials Market is poised to be significantly driven by surging electric vehicle sales and bolstering government policies and regulations.

- Conversely, the North America Electric Vehicle Battery Materials Market faces challenges due to a heavy dependence on imports, stemming from insufficient domestic raw material production.

- Nevertheless, continued efforts are being made to develop advanced battery technology. This factor is expected to create several opportunities for the market in the future.

- With a robust vehicle manufacturing and sales industry, the United States is set to dominate the growth landscape, likely registering the highest expansion during the forecast period.

North America Electric Vehicle Battery Materials Market Trends

Lithium-ion Batteries to Dominate the Market

- The lithium-ion battery segment is a cornerstone of the North American electric vehicle (EV) battery materials market, characterized by its pivotal role in the growth and advancement of electric vehicle technology. As the most widely adopted battery type for electric vehicles, lithium-ion batteries offer a favorable combination of energy density, efficiency, and longevity, making them indispensable for modern EV applications.

- Significant advancements in battery technology and manufacturing processes over the last decade have propelled the adoption of lithium-ion batteries in the electric vehicle market. These strides have not only slashed costs but also bolstered performance and reliability, rendering lithium-ion batteries increasingly attractive to manufacturers and consumers alike.

- In recent years, the price of lithium-ion batteries and cell packs has been on the decline, making them more attractive to end-user industries. After experiencing slight price hikes in 2022, battery prices were once again declining in 2023. The cost of lithium-ion battery packs has decreased by 14% to reach a historic low of USD 139/kWh.

- This segment encompasses a diverse array of materials, each contributing to the overall performance and functionality of the batteries. These materials are chosen for their ability to enhance the battery's energy density, cycle life, and thermal stability, thereby addressing critical performance parameters required by the automotive industry. Nickel-rich cathode materials, for instance, are particularly favored for their high energy capacity, which directly translates to extended driving ranges for electric vehicles-an essential factor for consumer adoption and market competitiveness.

- The region's increasing appetite for electric vehicles has propelled a notable surge in demand for lithium-ion batteries. Consequently, battery manufacturers and assemblers are now channeling investments into battery material production facilities. This strategic move aims to cater to the escalating need for lithium batteries, both on a domestic and international scale. Additionally, advancements in battery technology are further driving this demand. The market is expected to witness continued growth as electric vehicle adoption rises.

- For instance, in October 2023, Umicore, a significant player in electric vehicle battery materials, is solidifying its presence in Ontario, Canada, with the establishment of the CAM and pCAM plants. The company is actively building a 35 GWh battery materials production facility in Loyalist, ON, specifically tailored to cater to the burgeoning North American electric vehicle (EV) market.

- Recognizing the pivotal role this plant will play in bolstering the regional electric vehicle supply chain and enhancing the overall electric vehicle battery landscape, Umicore has secured significant financial backing from both the Canadian and Ontario governments.

- Therefore, as per the points mentioned above, the lithium-ion battery segment is expected to dominate the market during the forecasted period.

United States to Witness Significant Growth

- The United States segment has a robust and growing demand for electric vehicles, driven by a combination of consumer preferences, environmental awareness, and regulatory pressures to reduce greenhouse gas emissions. Federal and state-level incentives, such as tax credits and rebates for Electric Vehicle purchases, play a crucial role in accelerating the adoption of electric vehicles.

- In 2024, the available financial incentives include a tax credit of up to USD 7,500, while buyers of used electric cars might be eligible for up to USD 4,000. A notable change this year is that consumers can now choose to transfer this credit to a qualifying dealer, securing an instant discount on their vehicle purchase.

- These incentives not only make Electric Vehicles more affordable for consumers but also stimulate demand for advanced battery technologies and materials. Furthermore, the United States administration's commitment to achieving net-zero emissions by 2050 and the proposed infrastructure bill, which includes substantial investments in Electric Vehicle charging networks and clean energy initiatives, are expected to bolster the Electric Vehicle market further and, consequently, the demand for battery materials.

- These incentives have spurred a swift adoption of electric vehicles in the country. Notably, the International Energy Agency reports a steady rise in electric vehicle adoption over the past decade. Specifically, from 2022 to 2023, battery electric vehicle sales surged by over 37.5%. This growth is even more pronounced when considering the annual average rate over the past five years, which stood at an impressive 71.6%. Such figures underscore the escalating interest in electric vehicles, consequently boosting the demand for batteries in the nation.

- Significant investments in domestic battery manufacturing capabilities also characterize the United States segment. Recognizing the strategic importance of reducing dependence on foreign supply chains, both private sector players and government entities are investing heavily in the development of local battery manufacturing facilities. Companies like Tesla, General Motors, Hyundai, and Ford are spearheading efforts to establish gigafactories that produce lithium-ion batteries at scale.

- For instance, in April 2023, Two prominent automakers unveiled plans to construct electric vehicle (EV) battery plants in the United States, underscoring the continued rapid growth of electric vehicle manufacturing in the nation. General Motors, in collaboration with Samsung SDI, disclosed a joint investment of USD 3 billion for an electric vehicle battery plant in the United States. Concurrently, Hyundai revealed its partnership with South Korean battery manufacturer SK On, committing a substantial USD 5 billion to establish a battery factory in Georgia.

- These facilities aim to leverage advanced manufacturing technologies and automation to enhance production efficiency, reduce costs, and ensure a stable supply of high-quality batteries for the domestic market.

- Therefore, as mentioned above, the United States is expected to witness significant growth during the forecast period.

North America Electric Vehicle Battery Materials Industry Overview

The North America Electric Vehicle Battery Materials Market is moderately fragmented. Some of the key players in this market (in no particular order) are Targray Technology International Inc., BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, and Umicore

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Dependence on Imported Raw Material Supply

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

- 5.3 Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Targray Technology International Inc.

- 6.3.2 BASF SE

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 UBE Corporation

- 6.3.5 Umicore

- 6.3.6 Sumitomo Chemical Co., Ltd.

- 6.3.7 Nichia Corporation

- 6.3.8 ENTEK International LLC

- 6.3.9 Arkema SA

- 6.3.10 Kureha Corporation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology

02-2729-4219

+886-2-2729-4219

中东及非洲电动车电池材料市场占有率分析、产业趋势、统计及成长预测(2025-2030)中国电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)义大利电动汽车电池材料:市场占有率分析、产业趋势与统计、成长预测(2025-2030)亚太地区电动汽车电池材料:市场占有率分析、产业趋势、成长预测(2025-2030)南美洲电动汽车电池材料:市场占有率分析、产业趋势、成长预测(2025-2030)印度电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)德国电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)欧洲电动车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)法国电动车电池材料:市场占有率分析、产业趋势与统计、成长预测(2025-2030)电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)

中东及非洲电动车电池材料市场占有率分析、产业趋势、统计及成长预测(2025-2030)中国电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)义大利电动汽车电池材料:市场占有率分析、产业趋势与统计、成长预测(2025-2030)亚太地区电动汽车电池材料:市场占有率分析、产业趋势、成长预测(2025-2030)南美洲电动汽车电池材料:市场占有率分析、产业趋势、成长预测(2025-2030)印度电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)德国电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)欧洲电动车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)法国电动车电池材料:市场占有率分析、产业趋势与统计、成长预测(2025-2030)电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)

▼