|

市场调查报告书

商品编码

1636275

亚太地区电动汽车电池材料:市场占有率分析、产业趋势、成长预测(2025-2030)Asia Pacific Electric Vehicle Battery Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

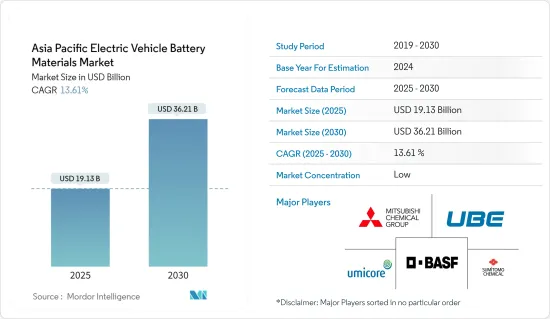

预计2025年亚太地区电动车电池材料市场规模为191.3亿美元,2030年将达362.1亿美元,预测期内(2025-2030年)复合年增长率为13.61%。

主要亮点

- 从中期来看,电动车(EV)销量的成长以及政府法规和倡议预计将在预测期内推动对电动车电池材料的需求。

- 相反,由于可靠性和成本效益,人们越来越偏好传统汽车,这给电动车及其电池的销售带来了挑战。

- 然而,电池技术的突破,具有更高的能量密度、更快的充电速度、更高的安全性和更长的使用寿命等特点,为参与企业带来了巨大的商机。

- 在电动车快速普及的推动下,印度预计将成为预测期内亚太地区电动车电池材料市场成长最快的地区。

亚太地区电动汽车电池材料市场趋势

锂离子电池类型主导市场

- 电动车(EV)锂离子电池产量的不断增加对电池材料市场产生了重大影响。电池产量的激增正在推动锂需求的大幅成长。该地区锂的发现对原材料成本产生了重大影响。

- 主要市场相关人员正在投资锂蕴藏量和研发,以提高锂离子电池产量并满足对电池原料日益增长的需求。这些蕴藏量的不断发现有助于长期压低锂离子电池的价格。

- 例如,2023年电池价格定为139美元/kWh时,降幅超过13%。预计,由于技术进步和製造改进,电池组的价格将在 2025 年降至 113 美元/kWh,到 2030 年降至 80 美元/kWh。

- 此外,为了因应日益增长的环境问题,亚太地区各国政府正积极支持电动车锂离子电池的生产。出于对实现净零碳排放的强烈兴趣,这些政府推出了多项倡议来提高锂离子电池的产量,以满足电动车需求的激增。

- 例如,2023年12月,韩国宣布未来五年投资290亿美元的计划,以加强其电池产业,重点是电动车电池。该策略包括实现电池供应链多元化以及为韩国大公司提供税收优惠。我们正在帮助这些公司向海外扩张,以获得重要电池材料的采矿权。这些措施不仅旨在扩大作为清洁能源替代品的锂离子电池的生产,而且会在短期内增加对电池材料的需求。

- 此外,锂离子电池价格下跌,加上需求激增和新生产工厂的建立,正在增强该地区对电池原料的需求。近年来,世界各地的主要企业启动了旨在扩大该地区电动车锂离子电池生产的计划。

- 例如,2024年2月,BMW宣布计画在泰国罗勇兴建新电池工厂。此举预计将加强该国的电池和供应链。 BMW希望泰国成为重要的电动车电池出口基地,并更广泛地服务亚太市场。这些倡议预计将在未来几年提高泰国的电池产量并增加对锂离子电池材料的需求。

- 鑑于这些发展,很明显,锂离子电池的生产将会进步,对电动车电池材料的需求将迅速增加。

印度正在经历显着的成长

- 印度在电动车(EV)电池材料领域占有重要地位。该国正在策略性地提高电池製造能力,同时确保基本材料的稳定供应。

- 近年来,印度已成为该地区电动车生产格局的主导力量。例如,根据国际能源总署(IEA)的报告,2023年印度电动车销量将达到8.2万辆,比2022年跃升70.8%,比2019年增长惊人的119倍。随着政府推出多项措施和计划,电动车销售的势头可能会持续下去。

- 印度致力于确保锂、钴和镍等关键材料的稳定和道德的供应。然而,这项倡议面临重大挑战。为了应对原材料挑战,印度正在利用国内蕴藏量并建立国际伙伴关係。印度的重点是利用其矿产资源来满足电动车电池材料需求的激增。

- 一项值得注意的进展是,印度地质调查局 (GSI) 于 2023 年 2 月在查谟和克什米尔的 Salal-Haimana 地区发现了锂蕴藏量估计为 590 万吨。锂是非铁金属,在电池能源储存系统和电动车应用中发挥至关重要的作用。这项发现满足了电动车对锂快速成长的需求,并使我们能够在可预见的未来提高电动车电池材料的产量。

- 印度领先的电动车製造商正在提高电池产能,以满足快速增长的电动车需求,这需要在基础设施和技术方面进行大量投资。

- Ola Electric 于 2024 年 7 月宣布,将在泰米尔纳德邦超级工厂的早期阶段投资 1 亿美元,这是一项重大倡议。该工厂将生产国产锂离子电池。 Ola Electric 的战略目标是在明年初之前转向生产自己的电池,摆脱目前在韩国和中国的供应商。此类大胆的投资不仅将加速电动车锂离子电池的生产,还将增加该地区对电动车电池材料的需求。

- 这些发展预计将显着增加电动车电池的产量,并且对电动车电池材料的需求预计在未来几年将激增。

亚太地区电动汽车电池材料产业概况

亚太地区电动汽车电池材料市场较为分散。主要参与企业(排名不分先后)包括BASF公司、三菱化学集团公司、宇部株式会社、优美科公司和住友化学公司。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 至2029年市场规模及需求预测(单位:十亿美元)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 电动车销量成长

- 政府扶持措施及措施

- 抑制因素

- 对传统汽车的依赖

- 促进因素

- 供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品/服务的威胁

- 竞争公司之间的敌对关係

- 投资分析

第五章市场区隔

- 电池类型

- 锂离子电池

- 铅酸电池

- 其他的

- 材料

- 正极

- 负极

- 电解

- 分隔符

- 其他的

- 地区

- 中国

- 印度

- 澳洲

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Sumitomo Chemical Co., Ltd.

- BASF SE

- Mitsubishi Chemical Group Corporation

- UBE Corporation

- Umicore SA

- Contemporary Amperex Technology Co. Limited

- Nichia Corporation

- ENTEK International LLC

- LG Chem

- Kureha Corporation

- 其他知名公司名单

- 市场排名/份额分析

第七章 市场机会及未来趋势

- 电池技术的进步

简介目录

Product Code: 50003562

The Asia Pacific Electric Vehicle Battery Materials Market size is estimated at USD 19.13 billion in 2025, and is expected to reach USD 36.21 billion by 2030, at a CAGR of 13.61% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, growing electric vehicle (EV) sales and supportive government policies and regulations are expected to drive the demand for electric vehicle battery materials during the forecast period.

- Conversely, the widespread preference for conventional vehicles, attributed to their reliability and cost-effectiveness, poses a challenge to the sales of electric vehicles and their batteries.

- However, breakthroughs in battery technology-boasting features like enhanced energy density, quicker charging, heightened safety, and extended lifespans-are set to unlock substantial opportunities for players in the electric vehicle battery materials market.

- Driven by surging electric vehicle adoption, India is poised to lead as the fastest-growing region in Asia Pacific's electric vehicle battery materials market during the forecast period.

Asia Pacific Electric Vehicle Battery Materials Market Trends

Lithium-Ion Battery Type Dominate the Market

- The growing production of lithium-ion batteries for electric vehicles (EVs) has notably influenced the battery materials market. This surge in battery production has driven a marked increase in lithium demand. Discoveries of lithium in the region have a pronounced effect on raw material costs.

- Key market players are channeling investments into lithium reserves and R&D, aiming to boost lithium-ion battery production and meet the escalating demand for battery raw materials. Ongoing discoveries of these reserves have been instrumental in driving down lithium-ion battery prices over time.

- For instance, battery prices saw a dip in 2023, settling at USD 139/kWh, marking a decline of over 13%. With the current trajectory of technological advancements and manufacturing improvements, projections suggest battery pack prices could further drop to USD 113/kWh by 2025 and USD 80/kWh by 2030.

- Moreover, in response to escalating environmental concerns, governments in the Asia Pacific are actively championing lithium-ion battery production for EVs. With a keen focus on achieving net-zero carbon emissions, these governments have launched multiple initiatives to boost lithium-ion battery production, catering to the surging EV demand.

- For instance, in December 2023, South Korea unveiled a USD 29 billion investment plan over the next five years to bolster its battery industry, with a spotlight on EV batteries. The strategy includes diversifying battery supply chains and providing tax incentives to major South Korean firms. These firms are being supported in their overseas ventures to secure mining rights for essential battery materials. Such initiatives are poised to not only amplify lithium-ion battery production as a clean energy alternative but also escalate the demand for battery materials in the foreseeable future.

- Additionally, the declining prices of lithium-ion batteries, coupled with a surging demand and the establishment of new production plants, are bolstering the demand for battery raw materials in the region. In recent years, top global firms have embarked on projects aimed at boosting lithium-ion battery production for EVs in the region.

- For instance, in February 2024, BMW unveiled plans for a new battery factory in Rayong, Thailand. This move is anticipated to bolster the nation's battery supply chains. BMW envisions Thailand as a pivotal export hub for its EV batteries, catering to the broader Asia Pacific market. Such undertakings are set to expedite battery production in Thailand and heighten the demand for lithium-ion battery materials in the years to come.

- Given these developments, it's clear that advancements in lithium-ion battery production and the surging demand for EV battery materials will continue to grow in the coming years.

India to Witness Significant Growth

- India is positioning itself as a key player in the electric vehicle (EV) battery materials arena. The nation is strategically bolstering its battery manufacturing capabilities while ensuring a steady supply of essential materials.

- In recent years, India has emerged as a dominant force in the regional EV production landscape. For instance, the International Energy Agency (IEA) reported that in 2023, India sold 82,000 electric vehicles, marking a 70.8% surge from 2022 and an astonishing 119-fold increase since 2019. With the government launching several initiatives and projects, the momentum in EV sales is set to continue its upward trajectory.

- India is placing a strong emphasis on ensuring a consistent and ethical supply of vital materials such as lithium, cobalt, and nickel. This endeavor, however, poses significant challenges. To tackle the raw material conundrum, India is delving into its domestic reserves and forging international partnerships. The nation's focus remains on harnessing its mineral wealth to cater to the surging demand for EV battery materials.

- In a notable development, the Geological Survey of India (GSI) unearthed lithium reserves estimated at 5.9 million tonnes in the Salal-Haimana region of Jammu and Kashmir in February 2023. Lithium, a non-ferrous metal, plays a pivotal role in battery energy storage systems and EV applications. This discovery is poised to satiate the burgeoning lithium demand for EVs and bolster EV battery material production in the foreseeable future.

- Leading Indian EV manufacturers are ramping up their battery production capabilities to align with the surging EV demand, necessitating substantial investments in both infrastructure and technology.

- In a significant move, Ola Electric, in July 2024, unveiled a USD 100 million investment for the initial phase of its gigafactory in Tamil Nadu. This facility is set to produce indigenous lithium-ion batteries. Ola Electric's strategic goal is to transition to its battery cells by early next year, moving away from its current suppliers in Korea and China. Such a bold investment is poised to not only expedite lithium-ion battery production for EVs but also amplify the demand for EV battery materials in the region.

- Given these developments, the trajectory of battery production for EVs is set for a significant boost, leading to a pronounced surge in demand for EV battery materials in the coming years.

Asia Pacific Electric Vehicle Battery Materials Industry Overview

Asia Pacific's electric vehicle battery materials market is fragmented. Some key players (not in particular order) are BASF SE, Mitsubishi Chemical Group Corporation, UBE Corporation, Umicore SA, Sumitomo Chemical Co., Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Supportive Government Policies and Regulations

- 4.5.2 Restraints

- 4.5.2.1 Dependence on Conventional Vehicle

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Others

- 5.2 Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.2.5 Others

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Australia

- 5.3.4 Japan

- 5.3.5 South Korea

- 5.3.6 Malaysia

- 5.3.7 Thailand

- 5.3.8 Indonesia

- 5.3.9 Vietnam

- 5.3.10 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Sumitomo Chemical Co., Ltd.

- 6.3.2 BASF SE

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 UBE Corporation

- 6.3.5 Umicore SA

- 6.3.6 Contemporary Amperex Technology Co. Limited

- 6.3.7 Nichia Corporation

- 6.3.8 ENTEK International LLC

- 6.3.9 LG Chem

- 6.3.10 Kureha Corporation

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/ Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology

02-2729-4219

+886-2-2729-4219

中东及非洲电动车电池材料市场占有率分析、产业趋势、统计及成长预测(2025-2030)中国电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)义大利电动汽车电池材料:市场占有率分析、产业趋势与统计、成长预测(2025-2030)北美电动车电池材料:市场占有率分析、行业趋势和成长预测(2025-2030)南美洲电动汽车电池材料:市场占有率分析、产业趋势、成长预测(2025-2030)印度电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)德国电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)欧洲电动车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)法国电动车电池材料:市场占有率分析、产业趋势与统计、成长预测(2025-2030)电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)

中东及非洲电动车电池材料市场占有率分析、产业趋势、统计及成长预测(2025-2030)中国电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)义大利电动汽车电池材料:市场占有率分析、产业趋势与统计、成长预测(2025-2030)北美电动车电池材料:市场占有率分析、行业趋势和成长预测(2025-2030)南美洲电动汽车电池材料:市场占有率分析、产业趋势、成长预测(2025-2030)印度电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)德国电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)欧洲电动车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)法国电动车电池材料:市场占有率分析、产业趋势与统计、成长预测(2025-2030)电动汽车电池材料:市场占有率分析、产业趋势/统计、成长预测(2025-2030)

▼