|

市场调查报告书

商品编码

1906221

中东和非洲IT服务:市场份额分析、行业趋势、统计数据和成长预测(2026-2031年)Middle East And Africa IT Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

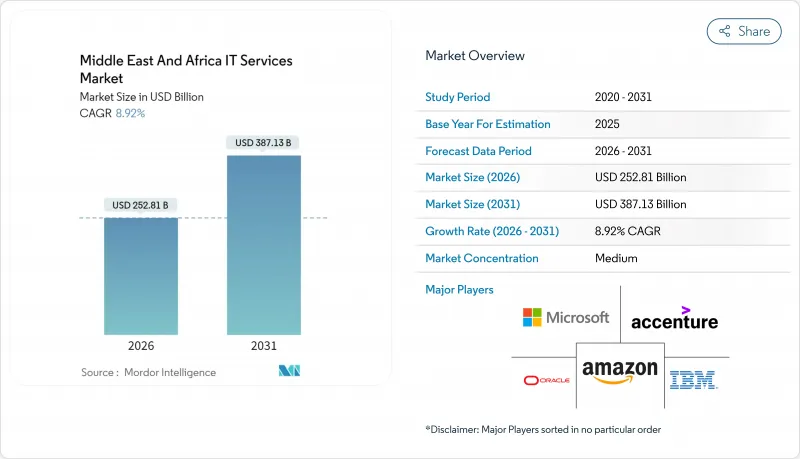

2025 年中东和非洲 IT 服务市场价值为 2321 亿美元,预计从 2026 年的 2528.1 亿美元增长到 2031 年的 3871.3 亿美元,预测期(2026-2031 年)复合年增长率为 8.92%。

政府主导的数位化计画加速推进、主权财富基金的技术指令以及5G的广泛应用,正在改变波湾合作理事会(GCC)和非洲主要经济体企业的IT支出模式。云端运算的普及、超大规模资料中心投资的激增以及全部区域的金融科技蓬勃发展,都推动了对咨询、实施和管理服务的需求。同时,精通云端原生技术的双语人才长期短缺以及跨境资料法律的分散化限制了成长前景,迫使服务提供者改进其交付模式和合规策略。全球整合商利用其规模和技术优势,而区域专家则利用其在地化需求和阿拉伯语能力,双方的竞争格局正在趋于平衡。

中东和非洲IT服务市场趋势与洞察

基于国家愿景的云端优先政策

沙乌地阿拉伯的数位政府政策以248亿美元的基础建设资金和覆盖全国的5G网路为支撑,旨在2030年将90%的公共服务迁移到云端。阿联酋和卡达也在推行类似的政策,推动需求从传统外包转向云端原生服务交付,这需要大规模整合、网路安全和託管服务的支援。为了保持竞争力,私人企业也正在效仿这些公共部门的标桿,推动混合云端咨询和平台服务的持续普及。

超大规模资料中心建设激增

沙乌地阿拉伯斥资210亿美元建设计画资料中心,以及由微软、贝莱德和淡马锡主导的300亿美元区域人工智慧基础建设联盟,正在改变当地的託管经济格局。新增的区域容量符合资料居住法规,支援对延迟敏感的工作负载,并能以高于传统託管服务的服务利润率实现边缘运算应用。

双语云原生人才短缺

南非在全球IT人才外流方面排名第三,2%的职缺为国际职位,导致本地人才流失严重。海湾合作委员会(计划对精通阿拉伯语和英语的专业人才的需求加剧了人才短缺,迫使供应商依赖外籍员工和分散的海外团队,从而增加了交付成本和周转时间。

细分市场分析

到2025年,云端和平台服务将占中东和北非地区IT服务市场份额的34.83%,预计复合年增长率将达到10.72%,这反映了企业向人工智慧架构的转型。传统外包对于传统工作负载仍然重要,但随着云端原生服务的成熟,其价格面临压力。随着网路风险在关键基础设施中日益增长,资安管理服务正在推动中东和北非地区IT服务市场的成长。 AWS、微软和Oracle在区域内的超大规模扩张,使服务供应商能够提供即时分析和物联网编配等附加价值服务,从而取代利润率低的基础设施支援服务。

随着企业对其关键业务应用程式进行平台重构,并针对边缘运算用例重新建构网路架构,对咨询和实施支援的需求仍然强劲。公共部门对文件管理和公民服务功能的业务流程外包 (BPO) 需求稳定。提供咨询、迁移支援和长期管理服务的供应商能够与客户建立持续的合作关係,并降低服务同质化的风险。

儘管大型企业预计到2025年将占总支出的67.55%,但中小企业预计将以10.18%的复合年增长率成长,这主要得益于海湾合作委员会(GCC)提供的云端服务补贴和技术援助计画。政府正拨款400亿美元帮助中小企业数位化,降低企业资源规划(ERP)、客户关係管理(CRM)和电子商务平台的进入门槛。这正在推动中东和北非(MENA)地区标准化SaaS IT服务市场的快速扩张。

大型企业持续授予人工智慧、预测性维护和多重云端管治计划多年期、数百万美元的合约。然而,价格敏感度日益提高,促使企业采用绩效付费的合约模式。将交付团队细分为高高触感企业计划和自动化中小企业工作的供应商,正在优化资源利用率和利润率。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- “2030愿景计画”中的“云端优先措施”

- 全部区域超大规模资料中心投资激增

- 数位公共服务与电子政府支出

- 区域金融科技繁荣推动了对託管服务的需求。

- 主权财富基金委託人工智慧和生成式人工智慧

- 5G和边缘运算的普及推动了整合计划的发展

- 市场限制

- 双语云原生人才长期短缺

- 跨境数据流动监管分散

- 非洲部分地区能源成本高且电网不稳定

- 地缘政治不稳定影响外包合约

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 影响市场的宏观经济因素

第五章 市场规模与成长预测

- 按服务类型

- IT咨询与实施支持

- IT外包(ITO)

- 业务流程外包(BPO)

- 资安管理服务

- 云端和平台服务

- 按最终用户公司规模划分

- 小型企业

- 大公司

- 按最终用户行业划分

- BFSI

- 製造业

- 政府/公共部门

- 医疗保健和生命科学

- 零售和消费品

- 通讯与媒体

- 物流/运输

- 能源与公共产业

- 其他终端用户产业

- 按部署模式

- 陆上交付

- 近岸交付

- 离岸交付

- 按国家/地区

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 科威特

- 阿曼

- 巴林

- 其他中东地区

- 非洲

- 南非

- 埃及

- 奈及利亚

- 肯亚

- 摩洛哥

- 其他非洲地区

- 中东

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Accenture plc

- International Business Machines Corporation(IBM)

- Oracle Corporation

- Microsoft Corporation

- Amazon Web Services, Inc.

- SAP SE

- Tata Consultancy Services Limited

- Infosys Limited

- Wipro Limited

- HCL Technologies Limited

- Google LLC(Google Cloud)

- Capgemini SE

- Cognizant Technology Solutions Corporation

- Tech Mahindra Limited

- NTT Data Corporation(Dimension Data)

- Gulf Business Machines(GBM)

- STC Solutions(Saudi Telecom Company)

- eand(Etisalat Group)

- Ooredoo QPSC

- Alareeb ICT Company

- Raqmiyat LLC

- Atos SE

- Deloitte Touche Tohmatsu Limited

第七章 市场机会与未来展望

The Middle East and Africa IT services market was valued at USD 232.1 billion in 2025 and estimated to grow from USD 252.81 billion in 2026 to reach USD 387.13 billion by 2031, at a CAGR of 8.92% during the forecast period (2026-2031).

Accelerated government-backed digitization programs, sovereign-wealth-fund technology mandates, and widespread 5G coverage are reshaping enterprise IT spending patterns across the Gulf Cooperation Council (GCC) and key African economies. Rising cloud adoption, surging hyperscale data-center investments, and a region-wide fintech boom are intensifying demand for consultative, implementation, and managed-service offerings. Meanwhile, chronic shortages of bilingual cloud-native professionals and fragmented cross-border data laws temper growth prospects, prompting providers to refine delivery models and compliance strategies. Competitive dynamics remain balanced as global integrators leverage scale and technology depth while regional specialists capitalize on localization requirements and Arabic language capabilities.

Middle East And Africa IT Services Market Trends and Insights

Cloud-First Mandates Under National Visions

Saudi Arabia's digital-government policy targets 90% cloud migration of public services by 2030, backed by USD 24.8 billion in infrastructure funding and nationwide 5G coverage. Comparable agendas in the UAE and Qatar require extensive integration, cybersecurity, and managed-service support, shifting demand from legacy outsourcing toward cloud-native delivery. Private enterprises mirror these public-sector benchmarks to sustain competitive parity, driving sustained uptake of hybrid-cloud consulting and platform services.

Surge in Hyperscale Data-Center Build-Outs

Saudi Arabia's USD 21 billion data-center pipeline and a USD 30 billion regional AI-infrastructure alliance anchored by Microsoft, BlackRock, and Temasek are transforming local hosting economics. Newly available in-region capacity satisfies data-residency statutes, supports latency-sensitive workloads, and enables edge-computing use cases that command higher service margins than traditional colocation offerings.

Bilingual Cloud-Native Talent Shortage

South Africa ranks third worldwide for outbound IT-talent recruitment, and 2% of all posted roles are international, draining local capacity. GCC projects intensify shortages by requiring Arabic-English fluent professionals, forcing providers to rely on expatriate hires or distributed offshore teams that increase delivery costs and timelines.

Other drivers and restraints analyzed in the detailed report include:

- Digital Public-Services Spending

- Fintech-Led Managed-Services Uptake

- Fragmented Cross-Border Data Laws

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The segment accounted for 34.83% of the Middle East and Africa IT services market share in 2025, yet cloud and platform services are set to grow at 10.72% CAGR, reflecting enterprises' pivot toward AI-ready architectures. Traditional outsourcing retains relevance for legacy workloads but faces pricing pressure as cloud-native offerings mature. The Middle East and Africa IT services market size attributed to managed security services is expanding as cyber-risk escalates across critical infrastructure. Regional hyperscale expansions by AWS, Microsoft, and Oracle allow providers to layer value-added services such as real-time analytics and IoT orchestration, displacing low-margin infrastructure support.

Demand for consulting and implementation remains robust as enterprises re-platform core applications and re-architect networks for edge-computing use cases. Business-process outsourcing maintains steady public-sector demand for document-management and citizen-service functions. Providers that bundle consulting, migration, and long-term managed services create sticky client relationships, mitigating commoditization risk.

Large enterprises represented 67.55% of 2025 spend, but SMEs are forecast to post a 10.18% CAGR, buoyed by subsidized cloud vouchers and technical-support schemes across GCC economies. Government funds worth USD 40 billion are earmarked for SME digital-enablement, lower entry barriers to ERP, CRM, and e-commerce platforms. The Middle East and Africa IT services market size for standardized SaaS onboarding is therefore rising sharply.

Large enterprises continue to award multi-year, multi-million-dollar contracts for AI, predictive maintenance, and multi-cloud governance projects. However, price sensitivity has increased, prompting outcome-based contracts. Providers that segment delivery teams for high-touch enterprise projects and automated SME engagements optimize utilization and margin.

The Middle East and Africa IT Services Market is Segmented by Service Type (IT Consulting and Implementation, IT Outsourcing, and More), End-User Enterprise Size (Small and Medium Enterprises and Large Enterprises), End-User Vertical (BFSI, Manufacturing, and More), Deployment Model (Onshore Delivery, Nearshore Delivery, and Offshore Delivery), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Accenture plc

- International Business Machines Corporation (IBM)

- Oracle Corporation

- Microsoft Corporation

- Amazon Web Services, Inc.

- SAP SE

- Tata Consultancy Services Limited

- Infosys Limited

- Wipro Limited

- HCL Technologies Limited

- Google LLC (Google Cloud)

- Capgemini SE

- Cognizant Technology Solutions Corporation

- Tech Mahindra Limited

- NTT Data Corporation (Dimension Data)

- Gulf Business Machines (GBM)

- STC Solutions (Saudi Telecom Company)

- eand (Etisalat Group)

- Ooredoo Q.P.S.C.

- Alareeb ICT Company

- Raqmiyat LLC

- Atos SE

- Deloitte Touche Tohmatsu Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first initiatives under Vision 2030 programs

- 4.2.2 Surge in hyperscale data-center investments across GCC

- 4.2.3 Digital public-services and e-government spending

- 4.2.4 Regional fintech boom driving managed-services demand

- 4.2.5 AI and generative-AI mandates by sovereign wealth funds

- 4.2.6 5G and edge-computing rollout fuelling integration projects

- 4.3 Market Restraints

- 4.3.1 Chronic shortage of bilingual cloud-native talent

- 4.3.2 Fragmented cross-border data-flow regulations

- 4.3.3 High energy cost and unreliable grids in parts of Africa

- 4.3.4 Geopolitical volatility affecting outsourcing contracts

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Service Type

- 5.1.1 IT Consulting and Implementation

- 5.1.2 IT Outsourcing (ITO)

- 5.1.3 Business Process Outsourcing (BPO)

- 5.1.4 Managed Security Services

- 5.1.5 Cloud and Platform Services

- 5.2 By End-User Enterprise Size

- 5.2.1 Small and Medium Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Manufacturing

- 5.3.3 Government and Public Sector

- 5.3.4 Healthcare and Life-Sciences

- 5.3.5 Retail and Consumer Goods

- 5.3.6 Telecom and Media

- 5.3.7 Logistics and Transport

- 5.3.8 Energy and Utilities

- 5.3.9 Other End-User Verticals

- 5.4 By Deployment Model

- 5.4.1 Onshore Delivery

- 5.4.2 Nearshore Delivery

- 5.4.3 Offshore Delivery

- 5.5 By Country

- 5.5.1 Middle East

- 5.5.1.1 Saudi Arabia

- 5.5.1.2 United Arab Emirates

- 5.5.1.3 Qatar

- 5.5.1.4 Kuwait

- 5.5.1.5 Oman

- 5.5.1.6 Bahrain

- 5.5.1.7 Rest of Middle East

- 5.5.2 Africa

- 5.5.2.1 South Africa

- 5.5.2.2 Egypt

- 5.5.2.3 Nigeria

- 5.5.2.4 Kenya

- 5.5.2.5 Morocco

- 5.5.2.6 Rest of Africa

- 5.5.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 International Business Machines Corporation (IBM)

- 6.4.3 Oracle Corporation

- 6.4.4 Microsoft Corporation

- 6.4.5 Amazon Web Services, Inc.

- 6.4.6 SAP SE

- 6.4.7 Tata Consultancy Services Limited

- 6.4.8 Infosys Limited

- 6.4.9 Wipro Limited

- 6.4.10 HCL Technologies Limited

- 6.4.11 Google LLC (Google Cloud)

- 6.4.12 Capgemini SE

- 6.4.13 Cognizant Technology Solutions Corporation

- 6.4.14 Tech Mahindra Limited

- 6.4.15 NTT Data Corporation (Dimension Data)

- 6.4.16 Gulf Business Machines (GBM)

- 6.4.17 STC Solutions (Saudi Telecom Company)

- 6.4.18 eand (Etisalat Group)

- 6.4.19 Ooredoo Q.P.S.C.

- 6.4.20 Alareeb ICT Company

- 6.4.21 Raqmiyat LLC

- 6.4.22 Atos SE

- 6.4.23 Deloitte Touche Tohmatsu Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

大型通讯业者业务与IT服务:全球市场预测(2025-2030)

大型通讯业者业务与IT服务:全球市场预测(2025-2030) 2026年全球网路部署服务市场报告

2026年全球网路部署服务市场报告 IT 服务市场:2026-2032 年全球市场预测(按服务类型、合约模式、最终用户、组织规模和部署方式划分)2026年全球5G网路部署服务市场报告2026年全球IT服务市场报告2026年全球硬体支援服务市场报告

IT 服务市场:2026-2032 年全球市场预测(按服务类型、合约模式、最终用户、组织规模和部署方式划分)2026年全球5G网路部署服务市场报告2026年全球IT服务市场报告2026年全球硬体支援服务市场报告 IT 服务市场规模、份额和趋势分析报告:按方法、类型、应用、技术、部署、企业规模、最终用途、地区和细分市场进行预测(2026-2033 年)

IT 服务市场规模、份额和趋势分析报告:按方法、类型、应用、技术、部署、企业规模、最终用途、地区和细分市场进行预测(2026-2033 年) IT 服务市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分Oracle服务市场分析及预测(至 2035 年):依类型、产品类型、服务、技术、元件、应用、部署类型、终端使用者、功能及解决方案划分

IT 服务市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分Oracle服务市场分析及预测(至 2035 年):依类型、产品类型、服务、技术、元件、应用、部署类型、终端使用者、功能及解决方案划分 美国IT服务:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

美国IT服务:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)