|

市场调查报告书

商品编码

1764336

全球汽车LED市场(2025年)- 照明与显示产品趋势2025 Global Automotive LED Market- Lighting and Display Product Trend |

||||||

全球汽车LED市场(2025年)- 照明和显示产品趋势预测,由于持续的经济不确定性,2025年价格下行压力将加剧。不过,TrendForce对车用LED厂商订单积压情况的分析显示,汽车产量预计将在2025年下半年再次復苏。此外,随着先进技术将继续搭载于2026年车型,预计到2025年,车用LED和车用照明的市场规模将分别成长至34.51亿美元和357.29亿美元。

未来汽车照明将致力于个人化、通讯显示、驾驶辅助和安全性提升

车用照明与显示器市场趋势

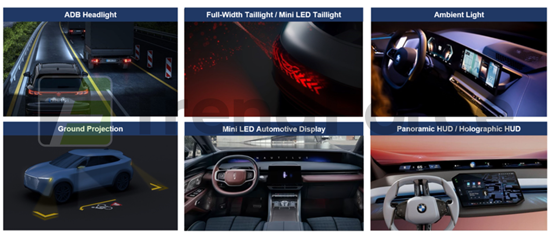

1.车头灯

ADB车头灯透过独立控制高性能LED,提供更佳的道路照明,扩大驾驶者的夜间视野,并透过独立控制延长侦测障碍物时的反应时间。无眩光远光灯可减轻前车和对侧车辆驾驶的不适感,并防止行人被车头灯晃眼。根据TrendForce分析,由于全球经济不确定性增加,ADB车头灯市场渗透率的成长放缓,但到2029年仍有望达到21.6%。

Micro/Mini LED像素模组在ADB车头灯的应用日益广泛,可透过像素的独立数位控制来调整照射区域,提高驾驶安全性。采Samsung的PixCell LED(COB技术)的Mini LED像素模组已成功搭载于Tesla Model 3/Y和NIO ES6。此外,Volkswagen、Porsche、SAICVolkswagen、NIO、Opel、Audi等汽车製造商将在2025年率先采用Micro LED头灯解决方案。

ADB头灯是大势所趋,强调小发光面(LES)、高亮度和高对比。据TrendForce表示,汽车製造商对Micro LED ADB头灯的平均像素要求为2万像素。未来Micro LED像素阵列的产品趋势可望朝两个方向发展:3000-4000像素的低像素产品,以及70000-100000像素的高阶产品。 OEM厂商的目标是每个头灯达到10万像素。因此,ams OSRAM和Nichia计划持续提升Micro LED像素阵列的像素数量,以满足汽车製造商的需求和目标。

2.尾灯

随着汽车照明个人化、通讯显示、驾驶辅助和安全性提升等趋势的发展,Mini LED 尾灯(后部)和 RGB Mini LED 通讯显示器(前部)应运而生。这些产品已应用于 IM Motors、GWM(SAR Mecha Dragon)、Changan(NEVO CD07)等品牌的车辆。根据 TrendForce 分析,目前主流设计主要采用 P3-P4 显示屏,出于成本和功耗方面的考虑,功率为 100W。

ams OSRAM 创新开发了 ALIYOS 技术,将 Mini LED 与排列在纤薄柔性透明箔片上的不显眼金属线连接起来。 ALIYOS 技术为 Mini LED 阵列的放置提供了极大的灵活性。它们还可以作为可单独寻址的单元形成任何形状,实现基于区块的灯光控制,允许动态显示符号、文字、图像和抽象画,用于造型、资讯传递和警告。 ams OSRAM 正与全球主要汽车零件製造商和 OEM 合作,探索汽车内外照明领域的全新可能性。

3.装饰照明

根据 TrendForce 分析,装饰照明包括气氛灯、格栅灯、全宽前饰条、ADS 标誌灯等。预计到2029年,装饰照明市场规模将跃升至 3.11亿美元,2024年至2029年的年复合成长率将达到 28%。其中,智慧氛围 LED 市场在2024年至2029年的年复合成长率将高达 69%。

智慧氛围灯采用内建驱动 IC 驱动的RGB LED。除了获得 ISELED 联盟认证的智慧氛围灯外,ams OSRAM 和 Dominant 还相继推出了搭载开放系统协定(OSP)的智慧氛围灯。 ams OSRAM 的智慧氛围灯已搭载于 ZEEKR MIX(2024年)车型,预计将被欧美汽车製造商采用。

除了 RGB LED 解决方案外,汽车製造商还计划采用高显色性(CRI 95 及以上)和可调色温(2,700-6,500K)的白光 LED 解决方案,用于阅读灯、车顶灯、化妆镜和脚部空间照明。首尔半导体采用 SunLike 技术的环境白光 LED 产品处于业界领先地位。该产品已成功整合于Volvo Polestar 3/EX90 车型。其 1W 环境白光 LED 亮度高达 100 lm(CRI 95 以上)。

4.小型LED车载显示器

随着HDR、局部调光、广色域和曲面萤幕设计的趋势发展,包括NIO、General Motors、Li Auto、BYD、Ford、Geely、Stellantis在内的汽车製造商将在2024年开始采用车载Mini LED显示器。Xiaomi、BMW、Mercedes-Benz、HKMC、BAIC、GWM、Sony预计将在2025年至2029年间推出搭载Mini LED显示器的汽车。此外,全景和全像HUD预计将开始采用Mini LED技术来提升对比度,进一步推动车载显示器市场的成长动能。

汽车照明市场规模及车灯厂商营收实绩

根据TrendForce预测,在新能源汽车的带动下,2024年全球汽车销售将达到8,855万辆,新能源汽车渗透率将达到25%。然而,随着车灯厂商受到价格压力、库存去化、汇率波动等因素的影响,汽车照明市场规模将小幅下滑至346.58亿美元。2024年,全球十大汽车照明厂商分别为Koito、Valeo、Forvia Hella、Marelli、Stanley、SL Corporation、Xingyu、HASCO Vision、ZKW、OPmobility。

车用LED厂商营收实绩

2024年全球五大车用LED厂商分别为ams OSRAM、Nichia、Lumileds、Seoul Semiconductor、Dominant。ams OSRAM凭藉其稳定的品质、卓越的光效和高性价比,已成为全球高端汽车和新能源汽车製造商的首选供应商。Seoul Semiconductor的销售业绩主要得益于韩国和中国订单的成长。此外,由于中国、欧洲和韩国市场需求的成长,亿光预计2024年其车用LED销售额将成长40%以上。弘凯光电致力于汽车市场应用,致力于光学感测技术,协助沟通和沈浸式体验,并致力于为客户提供一体化的加值服务。

TrendForce从七个角度分析车用LED市场的发展:

- (1)汽车照明与显示器的产品趋势

- (2)汽车照明市场规模与应用

- (3)汽车照明厂商营收与产品策略

- (4)车灯价格

- (5)车用LED市场需求(各产品应用与地区市场价值)

- (6)车用LED厂商营收实绩与产品策略

- (7)车用驱动IC市场规模与产品趋势

由此,为读者呈现车用LED市场的完整市场动态。

目录

第1章 汽车照明产品趋势

- 汽车照明产品趋势

- 头灯产品趋势

- 头灯产品趋势 - ADB 头灯 vs. 小直径头灯

- LED 头灯/ADB 头灯渗透率分析,2025-2029

- ADB头灯 - 优势及监管分析

- ADB头灯 - 矩阵式 LED/DLP/Micro LED 技术概述

- ADB头灯 - 矩阵式 LED/DLP/Micro LED 技术分析

- ADB头灯 - 矩阵式 LED/DLP/Micro LED 技术趋势,2025-2029

- ADB头灯 - Samsung PixCell LED 技术分析

- ADB头灯 - 100像素Mini LED模组价格及成本预测

- ADB头灯 - Tesla/Hella SSL 100头灯价格及成本预测

- ADB头灯 - Micro LED像素阵列规格分析

- ADB头灯 - Micro LED像素阵列技术分析

- ADB头灯 - 巨量转移设备分析

- ADB头灯 - Micro LED像素阵列价格及成本预测

- ADB头灯 - Micro LED头灯价格及成本预测

- ADB头灯 - Micro LED头灯市场应用分析

- Micro LED ADB头灯 - 福斯/Porsche,2023-2024

- Micro LED ADB头灯案例研究概况及供应链

- Micro LED ADB头灯特性分析

- LED头灯价格分析,2025年

- 雷射头灯 - 产品设计及供应链

- LED尾灯产品趋势

- 全宽尾灯价格价格与成本预测 - 0.2W SMD LED

- 全宽尾灯价格与成本预测 - 1515 LED

- Mini LED 尾灯 - ALIYOS

- Mini LED 尾灯合理价格与成本预测

- 类 OLED LED 尾灯产品趋势

- 气氛灯产品趋势 - 动态视觉照明

- (智慧)气氛灯 - 优缺点分析

- (智慧)气氛灯 - 设计架构概述

- (智慧)气氛灯 - 设计架构解决方案

- 智慧型气氛灯 - 开放式系统协定(OSP)vs. ISELED

- 智慧氛围灯 - 案例研究分析

- 气氛灯白光产品趋势

- 气氛灯 - 市场情势分析

- 格栅灯/前全宽条形灯产品趋势

- 格栅灯/前全宽条形产品设计

- 自动驾驶系统标誌灯产品趋势

- 地面投影产品趋势

- (智慧)气氛灯/装饰灯LED市场,2025-2029

第2章 车上显示产品趋势

- 智慧座舱趋势

- 智慧座舱-从现在到未来

- 车载显示技术概述

- 2025-2029年车上显示面板出货量及渗透率

- 2025-2029年车用背光LED市场规模分析

- LCD(侧光式/直下式)与OLED车用显示器规格比较

- Mini LED车用显示器-规格及供应链,2022

- Mini LED车载显示器 - 规格与供应链,2023

- Mini LED车用显示器 - 规格与供应链,2024

- COB/COG/POG 技术分析

- Mini LED 汽车显示器发展时间表和规格,2022-2029

- NIO ET7/ET5/ES7 汽车显示器 - 规格与成本分析

- Cadillac LYRIQ 汽车显示器 - 规格和成本分析

- Buick Electra E5 汽车显示器 - 规格与成本分析

- Cadillac Celestic 汽车显示器 - 规格与成本分析

- Zeekr 7X 汽车显示器 - 规格与成本分析

- Zeekr 009 汽车显示器 - 规格与成本分析

- HKMC 汽车显示器 - 规格与成本分析,2026

- 汽车显示器成本分析 - 边缘/直下式,2025

- Mini LED 汽车显示器 - 直驱/扫描驱动IC的优缺点

- OLED车上显示器发展规划及规格,2022-2025

- 车上背光显示器市场现况分析

- HUD市场出货量 -2025-2029年产品及地区市场分析

- HUD厂商出货量/市场占有率分析,2024年

- HUD产品规格分析

- AR-HUD技术分析

- AR-HUD OEM供应链及产品规格分析

- 2025年HUD产品价格分析

- 全景HUD与全像HUD

- HUD市场现况分析

- Micro LED透明显示器

- Micro LED车用显示器应用概述

- 2025年Micro LED车用透明显示器成本分析

- Micro LED车用显示器市场现况分析

第3章 汽车照明市场规模及各厂商营收实绩

- 汽车照明市场现况分析

- 2025-2029年汽车照明市场规模及应用分析

- 2022-2024年汽车照明厂商市场占有率分析

- 2022-2024年全球前15大汽车照明厂商营收分析

- 汽车照明产业併购分析

- 15家车灯厂商营收及产品策略分析

- 中国车灯/模组厂商

第4章 汽车LED厂商营收及策略分析

- 全球汽车LED厂商名单

- 2023-2024年汽车LED厂商市场占有率分析

- 2022-2024年全球前10大汽车LED厂商营收分析

- 全球前10大汽车LED厂商营收分析照明与背光,2023-2024

- 18家汽车LED製造商营收 - 照明与背光,2024年

- 6大汽车LED照明製造商营收预测 - 照明产品分析,2024年

- 2023年全球五大车灯LED公司营收分析

- 2024年全球五大车灯LED公司营收分析

- 2023年汽车LED厂商排名 - 中国/亚洲/欧洲、中东和非洲/美洲

- 2024年汽车LED厂商排名 - 中国/亚洲/欧洲、中东和非洲/美洲

- 18家汽车LED厂商营收及产品策略

第5章 汽车LED驱动IC市场及产品分析

- 汽车LED驱动IC市场规模2025-2029年分析

- Texas Instruments

- Macroblock

- Chipone

- Xm-Plus

- 车用 LED 驱动 IC 规格及价格分析

[Excel]

- 1.汽车市场出货量 - 区域市场分析

- 2.2025-2029年车用 LED 市场价值、量及普及率 - 产品分析

- 3.2024-2025年车用 LED 市场价值、量及普及率 - 产品/区域市场分析

- 4.汽车照明/车用 LED 市场各参与者营收实绩

- 5.车灯/车用 LED 市价分析

According to TrendForce "2025 Global Automotive LED Market- Lighting and Display Product Trend, towards 2025", due to the ongoing uncertainty in the overall economy, greater downward pricing pressure is anticipated in 2025. However, according to TrendForce's analysis on automotive LED manufacturers' orders on hand, car production is expected to recover again in 2H25. Additionally, with advanced technologies continuing to be incorporated into car models of 2026, the automotive LED and automotive lighting market value is forecasted to grow to USD 3.451 billion and USD 35.729 billion in 2025.

Automotive Lighting Will Concentrate on Personalization, Communication Display,

Driver Assistance, and Safety Upgrading in the Future

Automotive Lighting and Display Market Trend

1. Headlights

Through independent control of high-performance LEDs, the ADB headlights help expand drivers' nighttime field of view, giving them more time to react when seeing an obstacle and achieving better road lighting. Glare-free high beams help reduce discomfort for drivers of vehicles ahead, those of opposing vehicles, and prevent pedestrians from being dazzled by headlights. As TrendForce analyzes, increasing global economic uncertainty has slowed the growth of the ADB headlight market penetration rate, but still has the potential to reach 21.6% by 2029.

As Micro/Mini LED pixelated module is increasingly used for ADB headlights, the area of illumination can be adjusted for better driving safety through independent digital control of pixels. Mini LED pixelated modules utilized by Samsung's PixCell LED (COB technology) have been successfully implemented in the Tesla Model 3 / Y and the NIO ES6. In addition, Volkswagen, Porsche, SAIC Volkswagen, NIO, Opel, and Audi have been leading car makers in adopting Micro LED headlight solutions in 2025.

ADB headlights are the trend of the times, with an emphasis on a small light emitting surface (LES), high brightness, and high contrast. According to TrendForce, automakers require an average pixel count of 20,000 for Micro LED ADB headlights. The future product trend of Micro LED pixel arrays will have the opportunity to develop towards two polarizations: one is low-pixel products, using 3,000-4,000-pixels; the other is premium products, using 70,000-100,000-pixels. OEMs have set a target of 100,000 pixels per headlight. Therefore, ams OSRAM and Nichia plan to continually increase the pixel count of its Micro LED pixel array to meet automaker demands and goals.

2. Taillights

The increasing trend towards personalization, communication display, driver assistance, and safety upgrading for automotive lighting has given rise to Mini LED taillights (rear) and RGB Mini LED communication displays (front). These products have been installed in the vehicles of IM Motors, GWM (SAR Mecha Dragon), and Changan (NEVO CD07). According to TrendForce's analysis, current mainstream designs mainly incorporate P3-P4 displays and a 100W specification for cost and power consumption concerns.

ams OSRAM has innovatively developed its ALIYOS technology, connecting Mini LEDs with unnoticeable metal wires that are arranged on a slim, flexible, and transparent foil. ALIYOS offers great flexibility for the arrangement of Mini LED arrays. It can also form any shape as individually addressable units, achieving block-based light control, hence the ability to display symbols, words, images, and abstract pictures dynamically for styling, messaging, and warning. ams OSRAM is working with leading Tier 1 automotive suppliers and OEMs worldwide to explore new possibilities in both interior and exterior automotive lighting.

3. Decorative Lighting

As TrendForce analyzes, decorative lights include ambient lights, grill lamps, full-width front strips, and ADS marker lamps. The decorative light market scale is likely to jump to USD 311 million by 2029, with a 28% CAGR from 2024 to 2029. Specifically, the 2024-2029 CAGR for the intelligent ambient LED market will be a whopping 69%.

Intelligent ambient lights are equipped with RGB LEDs powered by built-in driver ICs. Beyond the intelligent ambient lights certified by the ISELED Alliance, ams OSRAM and Dominant have successively launched intelligent ambient lights with the Open System Protocol (OSP). The microcontroller can send commands to lighting units individually and obtain their status, enabling high-precision color calibration and temperature compensation. ams OSRAM's intelligent ambient lights are installed on the ZEEKR MIX (2024) model and is expected to be adopted by European and American automakers.

In addition to RGB LED solutions, automakers intend to adopt white LED solutions featuring high color rendering (CRI greater than or equal to 95), and adjustable color temperature (2,700-6,500K) for reading lights, roof lights, make-up mirrors, and foot room illumination. Seoul Semiconductor's ambient white LED product featuring SunLike technology leads the industry. The product has been successfully integrated into Volvo Polestar 3 / EX90. Its 1W ambient white LED achieves a brightness of up to 100 lm (CRI greater than or equal to 95).

4. Mini LED Automotive Displays

Following the trend towards HDR, local dimming, wide color gamut, and curved screen design, car manufacturers began adopting automotive Mini LED displays in 2024, including NIO, General Motors, Li Auto, BYD, Ford, Geely, and Stellantis. Xiaomi, BMW, Mercedes-Benz, HKMC, BAIC, GWM, and Sony are expected to release vehicles equipped with Mini LED displays between 2025 and 2029. Additionally, panoramic HUDs and holographic HUDs will start adopting Mini LED technology to enhance contrast ratio, which is expected to drive growth momentum for the automotive display market.

Automotive Lighting Market Scale and Automotive Lamp Player Revenue Performance

According to TrendForce, driven by NEVs, global car sales in 2024 hit 88.55 million units, with the NEV penetration rate reaching 25%. However, as automotive lighting manufacturers were affected by pricing pressure, inventory depletion, and exchange rate fluctuations, the automotive lighting market value slightly dropped to USD 34.658 billion. In 2024, the top ten automotive lighting players were Koito, Valeo, Forvia Hella, Marelli, Stanley, SL Corporation, Xingyu, HASCO Vision, ZKW, and OPmobility.

Automotive LED Player Revenue Performance

The top five automotive LED manufacturers in 2024 include ams OSRAM, Nichia, Lumileds, Seoul Semiconductor, and Dominant. Thanks to the stable quality, exceptional luminous efficacy, and good value of its products, ams OSRAM has become the preferred supplier for premium vehicle and NEV manufacturers worldwide. Seoul Semiconductor's sales performance was mainly benefited from order increases in Korea and China. In addition, thanks to the rising demand in China, Europe, and South Korea, Everlight saw its automotive LED revenue surge more than 40% in 2024. Brightek specializes in automotive market applications and has regarded light sensing for communication and immersive experiences as its target, aiming to offer integrated value-added services for its customers.

TrendForce has analyzed developments in the automotive LED market from seven perspectives:

- 1) automotive lighting and display product trends,

- 2) automotive lighting market scale and applications,

- 3) automotive lighting player revenue and product strategies,

- 4) automotive lamp prices,

- 5) automotive LED market demand (product applications and regional market value), and

- 6) automotive LED player revenue performance and product strategies.

- 7) automotive driver IC market scale and product trend.

In this way, we provide readers with a comprehensive picture of marketing dynamics in the automotive LED market.

Table of Contents

Chapter 1. Automotive Lighting Product Trend

- Automotive Lighting Product Trend

- Headlight Product Trend

- Headlight Product Trend- ADB Headlight vs. Small Aperture

- 2025-2029 LED Headlight / ADB Headlight- Penetration Rate Analysis

- ADB Headlight- Advantage and Regulation Analysis

- ADB Headlight- Matrix LED / DLP / Micro LED Technology Overview

- ADB Headlight- Matrix LED / DLP / Micro LED Technology Analysis

- 2025-2029 ADB Headlight- Matrix LED / DLP / Micro LED Technology Trend

- 2025-2029 ADB Headlight LED Market- LED vs. Micro/Mini LED Module

- ADB Headlight- Samsung PixCell LED Technology Analysis

- ADB Headlight- 100-Pixel Mini LED Module Price and Cost Estimates

- ADB Headlight- Tesla / Hella SSL 100 Headlight Price and Cost Estimates

- ADB Headlight- Micro LED Pixel Array Specification Analysis

- ADB Headlight- Micro LED Pixel Array Technology Analysis

- ADB Headlight- Mass Transfer Equipment Analysis

- ADB Headlight- Micro LED Pixel Array Price and Cost Estimates

- ADB Headlight- Micro LED Headlight Price and Cost Estimates

- ADB Headlight- Micro LED Headlight Market Application Analysis

- 2023-2024 Micro LED ADB Headlight- Volkswagen / Porsche

- Micro LED ADB Headlight Case Study Overview and Supply Chain

- Micro LED ADB Headlight Function Analysis

- 2025 LED Headlight Price Analysis

- Laser Headlight- Product Design and Supply Chain

- LED Taillight Product Trend

- Full-Width Taillight Price and Cost Estimates- 0.2W SMD LED

- Full-Width Taillight Price and Cost Estimates- 1515 LED

- Mini LED Taillight- ALIYOS

- Mini LED Taillight Price Sweet Spot and Cost Estimates

- OLED-Like LED Taillight Product Trend

- Ambient Light Product Trend- Dynamic Visual Lighting

- (Intelligent) Ambient Light- Pros-Cons Analysis

- (Intelligent) Ambient Light- Design Architecture Overview

- (Intelligent) Ambient Light- Design Architecture Solutions

- Intelligent Ambient Light- Open System Protocol (OSP) vs. ISELED

- Intelligent Ambient Light- Case Study Analysis

- Ambient Light White Product Trend

- Ambient Light- Market Landscape Analysis

- Grille Lamp / Full-Width Front Stripe Product Trend

- Grille Lamp / Full-Width Front Stripe Product Design

- Autonomous Driving System Marker Lamp Product Trend

- Ground Projection Product Trend

- 2025-2029 (Intelligent) Ambient Light LED / Decorative Light LED Markets

Chapter 2. Automotive Display Product Trend

- Smart Cockpit Trend

- Smart Cockpit- From Today to the Future

- Automotive Display Technology Overview

- 2025-2029 Automotive Display Panel Shipment and Penetration Rate

- 2025-2029 Automotive Backlight LED Market Value Analysis

- LCD (Edge / Direct-Type) vs. OLED Automotive Display Specification

- 2022 Mini LED Automotive Display- Specification vs. Supply Chain

- 2023 Mini LED Automotive Display- Specification vs. Supply Chain

- 2024 Mini LED Automotive Display- Specification vs. Supply Chain

- COB / COG / POG Technology Analysis

- 2022-2029 Mini LED Automotive Display Schedule and Specification

- NIO ET7 / ET5 / ES7 Automotive Display- Specification and Cost Analysis

- Cadillac LYRIQ Automotive Display- Specification and Cost Analysis

- Buick Electra E5 Automotive Display- Specification and Cost Analysis

- Cadillac Celestiq Automotive Display- Specification and Cost Analysis

- Zeekr 7X Automotive Display- Specification and Cost Analysis

- Zeekr 009 Automotive Display- Specification and Cost Analysis

- 2026 HKMC Automotive Display- Specification and Cost Analysis

- 2025 Automotive Display Cost Analysis- Edge / Direct-Type

- Mini LED Automotive Display- Direct / Scan Driver IC Pros-Cons Analysis

- 2022-2025 OLED Automotive Display Schedule and Specification

- Automotive Backlight Display Market Landscape Analysis

- 2025-2029 HUD Market Shipment- Product vs. Regional Market Analysis

- 2024 HUD Player Shipment / Market Share Analysis

- HUD Product Specification Analysis

- AR-HUD Technology Analysis

- AR-HUD OEM Supply Chain and Product Specification Analysis

- 2025 HUD Product Price Analysis

- Panoramic HUD vs. Holographic HUD

- HUD Market Landscape Analysis

- Micro LED Transparent Display

- Micro LED Automotive Display Application Overview

- 2025 Micro LED Automotive Transparent Display Cost Analysis

- Micro LED Automotive Display Market Landscape Analysis

Chapter 3. Automotive Lighting Market Scale and Player Revenue Performance

- Automotive Lighting Market Landscape Analysis

- 2025-2029 Automotive Lighting Market Scale- Application Analysis

- 2022-2024 Automotive Lighting Player Market Share Analysis

- 2022-2024 Top 15 Automotive Lighting Player Revenue Ranking

- Automotive Lighting Industry M&A Analysis

- 15 Automotive Lamp Manufacturers Revenue and Product Strategies

- Automotive Lamp / Module Factories in China

Chapter 4. Automotive LED Player Revenue and Strategies

- Global Automotive LED Player List

- 2023-2024 Automotive LED Player Market Share Analysis

- 2022-2024 Top 10 Automotive LED Player Revenue Ranking

- 2023-2024 Top 10 Automotive LED Player Revenue- Lighting vs. Backlight

- 2024 18 Automotive LED Players' Revenue- Lighting vs. Backlight

- 2024 Top 6 Automotive LED Player Revenue- Lighting Product Analysis

- 2023 Global Top 5 Headlight LED Player Revenue Analysis

- 2024 Global Top 5 Headlight LED Player Revenue Analysis

- 2023 Auto Lighting LED Player Ranking- China / Asia / EMEA / Americas

- 2024 Auto Lighting LED Player Ranking- China / Asia / EMEA / Americas

- 18 Automotive LED Manufacturers Revenue and Product Strategies

Chapter 5. Automotive LED Driver IC Market and Product Analysis

- 2025-2029 Automotive LED Driver IC Market Value Analysis

- Texas Instruments

- Macroblock

- Chipone

- Xm-Plus

- Automotive LED Driver IC Specification and Price Analysis

[EXCEL]

- 1. Car Market Shipment- Regional Market Analysis

- 2. 2025-2029 Automotive LED Market Value, Volume and Penetration- Product Analysis

- 3. 2024-2025 Automotive LED Market Value, Volume and Penetration- Product / Regional Market Analysis

- 4. Automotive Lighting / Automotive LED Player Revenue Performance

- 5. Automotive Lamp / Automotive LED Market Price Analysis

2026年全球汽车LED照明市场报告

2026年全球汽车LED照明市场报告 汽车LED照明市场-全球产业规模、份额、趋势、机会、预测:按位置、车辆类型、自适应照明、地区和竞争格局划分,2021-2031年

汽车LED照明市场-全球产业规模、份额、趋势、机会、预测:按位置、车辆类型、自适应照明、地区和竞争格局划分,2021-2031年 汽车LED照明市场规模、份额和成长分析(按技术类型、车辆类型、类型和地区划分)-产业预测(2026-2033年)

汽车LED照明市场规模、份额和成长分析(按技术类型、车辆类型、类型和地区划分)-产业预测(2026-2033年) 汽车用LED的世界市场趋势:照明和显示器预测

汽车用LED的世界市场趋势:照明和显示器预测 汽车LED照明市场:2025年至2030年预测全球汽车LED尾灯市场:未来预测(2025-2030)

汽车LED照明市场:2025年至2030年预测全球汽车LED尾灯市场:未来预测(2025-2030) 汽车用LED照明的全球市场:车辆类别,各销售管道,各应用类型,各地区,机会,预测,2018年~2032年

汽车用LED照明的全球市场:车辆类别,各销售管道,各应用类型,各地区,机会,预测,2018年~2032年 中东和非洲汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)中国汽车 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)亚太地区汽车 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

中东和非洲汽车 LED 照明:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)中国汽车 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)亚太地区汽车 LED 照明:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)