|

市场调查报告书

商品编码

1911455

印尼二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Indonesia Used Car - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

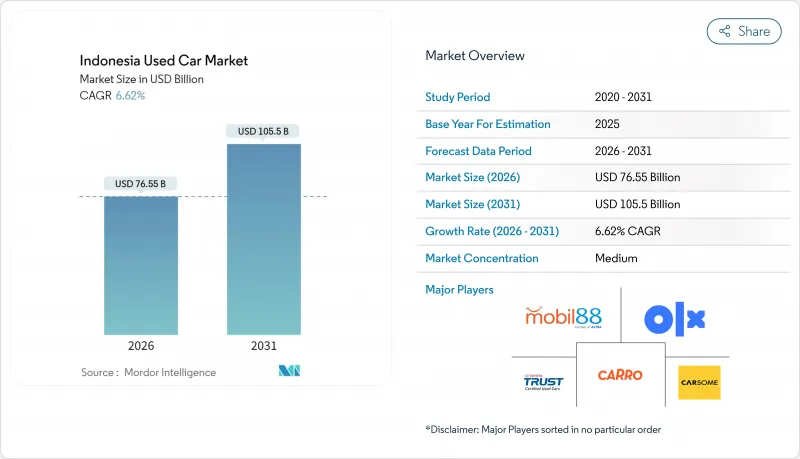

预计印尼二手车市场规模将从 2025 年的 718 亿美元成长到 2026 年的 765.5 亿美元,到 2031 年将达到 1,055 亿美元,2026 年至 2031 年的复合年增长率为 6.62%。

需求韧性反映出市场结构向二手车转变,信贷环境收紧和购买力下降迫使家庭在不推迟出行目标的前提下精打细算。二手车融资额将在2024年首次超过新车融资额,这标誌着消费行为正在持续调整。线上广告已成为资讯搜寻的主要方式,而新兴的人工智慧评估工具透过提供客观的车辆状况评分,正在缩小价格差距。主要银行贷款策略的转变提高了贷款的可及性和盈利能力,同时,叫车业者的车队更新也为经销商库存创造了源源不绝的优质二手车。

印尼二手车市场趋势及洞察

拓展线上广告与电子商务活动

数位平台让消费者在联繫卖家之前比较价格、里程和照片,从而简化交易流程。平台营运商整合了验车、融资和文书工作,减轻了经销商密度低的农村地区消费者的搜寻负担。 SEVA在2024年实现了17,500辆汽车的销量和8.2兆印尼币的总交易额,证明了这种模式的有效性,并刺激了资本流入和独角兽企业的诞生。传统企业集团也积极回应:Astra收购OLX后,将其内部融资、验车中心和物流整合到单一平台上。 OJK对平台内数位贷款的监管支援进一步完善了无缝体验,推动印尼二手车市场向更深层的线上渗透。

银行转向二手的二手车贷款产品

印尼中亚银行(BCA)等领先银行预计,到2024年,其汽车贷款余额将达到65.3兆印尼币(约41亿美元)。随着贷款机构寻求更高收益,二手车的市场份额正在不断增长。我们独特的评分系统经过改进,纳入了包括里程数、详细检测等级和预计转售价值在内的多种关键因素,不再只关注借款人的收入。这种创新方法使得线上市场能够实现即时预核准,显着缩短了核准时间,仅需几个小时。因此,这项精简的流程不仅提高了转换率,也刺激了印尼二手车市场的流动性,为买卖双方创造了更多机会。

虚报里程数和事故记录的现象仍然十分普遍。

地方政府的车辆登记(STNK)和所有权证书(BPKB)系统各自独立运行,使得不法分子能够篡改里程或掩盖车辆跨州运输过程中的水损情况。首次购车者和线上购车者受影响最大,他们往往要为问题车辆支付过高的价格。这种信任缺失推高了贷款风险溢价,并将阻碍印尼二手车市场的流动性,直到人工智慧检测和集中式数据普及。

细分市场分析

截至2025年,SUV将占印尼二手车市场37.62%的份额,这主要得益于其较高的离地间隙和在拥挤道路上的安全性能。 MPV的复合年增长率(CAGR)为7.05%,受到重视侧滑门和灵活座椅布局的多代家庭的青睐。轿车的目标客户是注重燃油效率的通勤者,而掀背车是针对能够应对狭窄停车位的首次购车者。预计在车队更新换代带来的强劲供应推动下,SUV在印尼二手车市场的份额将持续成长。然而,由于学生通勤需求的增加,MPV在爪哇岛郊区的销售量正在下降。中国汽车製造商正凭藉具有竞争力的混合模式进军这两个细分市场,而老牌日本汽车製造商也更频繁地更新其产品阵容。

在雅加达和泗水,新能源SUV深受追求品质生活的消费者青睐。而在路况较为复杂的外岛地区,紧凑型MPV则占主导地位。数位平台利用演算法向叫车用户推荐SUV,向成长型家庭推荐MPV,进而提高配对效率。认证二手车专案也更倾向于SUV和MPV,因为与轿车相比,这些车型的保固提升销售盈利更高。

截至2025年,汽油动力汽车仍将占印尼二手车市场63.10%的份额,但混合动力汽车汽车和电动车正以12.34%的复合年增长率快速成长,这主要得益于消费税减免和奢侈品税豁免政策。由于政府正在讨论削减补贴和实施更严格的排放气体法规,柴油汽车的市占率正在萎缩。虽然二手电动车市场规模仍然小规模,但快速充电桩的普及性和政府的蓝图预计将促进未来二手车的流通。从2024年起,雅加达竞标会上混合动力汽车的残值预计将比汽油动力汽车高出6-8%,这表明购车者的购车标准正在改变。

电池劣化的不不确定性限制了电动车的普及。经销商对未经製造商检验的老款电动车持谨慎态度。银行正在缩短仍在保固期内的电动车的贷款期限并降低抵押品估值。同时,在充电基础设施不发达的农村市场,汽油动力汽车仍具有流动性优势。

到2025年,价格区间在11,000美元至21,999美元之间的二手车将占印尼二手车市场收入的39.05%,年复合成长率达7.33%,这与家庭中等收入水准和银行信贷额度的成长趋势相符。售价低于5,500美元的入门级车型吸引了省会城市的现金买家,而售价高于22,000美元的高端车型则迎合了追求豪华品牌的富裕都市人群的需求。印尼二手价位二手车市场份额的成长得益于旺盛的置换需求以及提供一年保固的认证二手车项目。

线上分期付款模拟工具正在帮助提升消费者对中价位车型的认知度,在各大门户网站上搜寻最高的方案是首付20%、分48个月支付的1.5万美元Avanza车型。高阶车型市场的成长主要得益于外籍人士的车辆更新换代和企业车队的处置,但与以性价比为导向的核心市场相比,它仍然是一个小众市场。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 拓展线上广告与电子商务活动

- 银行转向推出专门针对二手车的贷款产品

- 在爪哇岛以外地区拓展有组织的经销商网络

- 叫车车辆更新週期(Grab 和 Gojek)

- 原厂回购计画提升残值

- 人工智慧驱动的状况评估平台缩小了价格差距

- 市场限制

- 里程表和事故记录造假现象依然普遍存在。

- 分散式州登记资料库

- 岛际物流成本高昂阻碍了爪哇岛以外的贸易。

- 二手电动汽车电池健康检查的认证实施有限

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按车辆类型

- 掀背车

- 轿车

- SUV

- MPV

- 按燃料类型

- 汽油

- 柴油引擎

- 混合动力汽车和电动车

- 其他(液化石油气、压缩天然气等)

- 按价格范围

- 低于5500美元

- 5,500 美元至 10,999 美元

- 11,000 美元至 21,999 美元

- 超过22,000美元

- 按销售管道

- 线上数位分类门户

- 纯粹的电子零售商

- 经销商/OEM线上平台

- 实体加盟店

- 独立二手车经销商

- 竞标行(线上线下混合式)

- 私人销售

- 依供应商类型

- 组织

- 杂乱无章

- 车龄

- 0-2岁

- 3-5年

- 6-8岁

- 8年以上

- 贷款提供者

- 汽车製造商(OEM)

- 银行

- 非银行金融公司

- 按州

- 西爪哇

- 东爪哇

- 中爪哇

- 北苏门答腊

- 万登

- 雅加达

- 其他州

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Mobil88(PT Serasi Auto Raya(SERA))

- Toyota Astra Motor(Toyota Trust)

- PT Tunas Ridean Tbk.

- PT Inchcape Indomobil Distribution Indonesia(IIDI)(Mercedes Certified)

- BMW Premium Selection(BME Eurokars)

- OLX Indonesia

- Carro Indonesia(Trusty Cars Ltd)

- Carsome Indonesia

- Broom.id

- Carmudi Indonesia

- Moladin

- Mobil123

第七章 市场机会与未来展望

The Indonesia used car market is expected to grow from USD 71.80 billion in 2025 to USD 76.55 billion in 2026 and is forecast to reach USD 105.5 billion by 2031 at 6.62% CAGR over 2026-2031.

Demand resilience reflects a structural tilt toward pre-owned vehicles as tighter credit conditions and waning purchasing power push households to stretch budgets without postponing mobility goals. Used-car financing outpaced new-car loans for the first time in 2024, signalling a lasting recalibration of consumer behavior. Online classifieds now dominate discovery journeys, and emerging AI-grading tools narrow price dispersion by giving buyers objective condition scores. Financing pivots by major banks boost accessibility and margins, while ride-hailing fleet renewals inject a steady stream of high-quality cars into dealer inventories.

Indonesia Used Car Market Trends and Insights

Growing Online Classified and E-retail Activity

Digital portals empower consumers to compare prices, mileage, and photos, streamlining their transactions before reaching out to sellers. Platform operators integrate inspection, financing, and documentation, reducing search friction in secondary cities where dealer density is low. SEVA's 17,500-unit throughput and IDR 8.2 trillion gross transaction value in 2024 validated the model, encouraging capital inflows and unicorn creation . Traditional conglomerates have reacted: Astra's OLX acquisition aligned captive financing, inspection centers, and logistics into a single stack. Regulatory support from OJK for in-platform digital lending completes a frictionless experience, propelling the Indonesian used car market toward deeper online penetration.

Banks' Pivot to Used-car Specific Loan Products

Major banks such as BCA expanded vehicle loan books to IDR 65.3 trillion (USD 4.1 billion) in 2024, with used cars forming an increasing share as lenders chase higher yields . Proprietary scorecards have evolved to incorporate a range of crucial factors, including mileage bands, detailed inspection grades, and projected resale values, moving beyond the traditional focus on borrower income. This innovative approach allows for instant pre-approval within online marketplaces, significantly reducing approval times to just a few hours. As a result, this streamlined process not only enhances conversion rates but also invigorates liquidity in the Indonesian used car market, creating dynamic opportunities for both buyers and sellers.

Odometer and Accident-history Fraud Remains Pervasive

Provincial STNK and BPKB systems operate in silos, letting bad actors reset mileage or hide flood damage when vehicles cross borders. First-time buyers and online shoppers bear the brunt, paying inflated prices for compromised cars. Trust deficits raise financing risk premiums, dampening the Indonesia used car market velocity until AI inspection and centralized data become mainstream.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Organized Dealer Networks Outside Java

- Ride-hailing Fleet Renewal Cycles (Grab and Gojek)

- Fragmented Provincial Registration Databases

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SUVs owned 37.62% of the Indonesia used car market share in 2025, buoyed by high ground clearance and perceived safety in congested streets. MPVs, climbing at 7.05% CAGR, appeal to multi-generational households that prize sliding doors and flexible seating. Sedans cater to commuters seeking fuel efficiency, and hatchbacks target first-time owners navigating tight parking norms. The Indonesia used car market size for SUVs is projected to keep pace with robust supply from fleet replacements, yet MPVs fetch quicker days-to-sale in suburban Java as school-run demand rises. Chinese OEMs have entered both segments with competitive hybrid trims, pushing Japanese incumbents to refresh line-ups more frequently.

New-energy SUVs feed aspirational buyers in Jakarta and Surabaya, while compact MPVs dominate outer-island lanes where road quality varies. Digital platforms algorithmically recommend SUVs to ride-hailing prospects and MPVs to growing families, increasing match efficiency. Certified programs overweight SUVs and MPVs because warranty upsells monetize better than sedans.

Petrol models still command 63.10% of the Indonesia used car market size in 2025, yet hybrids and electric models exhibit a 12.34% CAGR, propelled by VAT cuts and zero luxury tax. The diesel share erodes amid rising subsidy talk and emissions scrutiny. The Indonesia used car market size for electric models remains small, but fast-charger rollouts and government roadmaps catalyze future secondary sales. Residual values of hybrids have outperformed petrol peers in Jakarta auctions by 6-8% since 2024, hinting at shifting buyer calculus.

Battery degradation uncertainty curbs wider uptake. Dealers hesitate to stock older BEVs without OEM testing. Banks apply shorter tenures and higher collateral haircuts for BEVs pending battery warranties. Petrol cars, however, keep liquidity advantages in rural exchanges where charging remains scarce.

Units priced USD 11,000-21,999 held 39.05% of the Indonesia used car market revenue in 2025 and expanded at 7.33% CAGR, aligning with median household affordability and bank lending brackets. Entry models under USD 5,500 attract cash buyers in tier-3 cities, while premium brackets above USD 22,000 serve affluent urbanites eyeing luxury badges. The Indonesia used car market share of mid-range vehicles benefits from abundant trade-ins and certified programs bundling one-year warranties.

Online calculators showcasing installment scenarios boost mid-range visibility: a USD 15,000 Avanza with a 20% down payment and a 48-month tenor remains the most-searched combination on leading portals. Growth in premium slices rides on expatriate turnovers and corporate fleet disposals, but remains niche relative to value-centric core segments.

The Indonesia Used Car Market Report is Segmented by Vehicle Type (Hatchbacks, Sedans, and More), Fuel Type (Petrol, Diesel, and More), Price Segment (Below USD 5, 500, USD 5, 500-10, 999, and More), Sales Channel (Online Digital Classified Portals, Pure-Play E-Retailers, and More), Vendor Type (Organized and Unorganized), Vehicle Age, Financing Providers, and Province. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mobil88 (PT Serasi Auto Raya (SERA))

- Toyota Astra Motor (Toyota Trust)

- PT Tunas Ridean Tbk.

- PT Inchcape Indomobil Distribution Indonesia (IIDI) (Mercedes Certified)

- BMW Premium Selection (BME Eurokars)

- OLX Indonesia

- Carro Indonesia (Trusty Cars Ltd )

- Carsome Indonesia

- Broom.id

- Carmudi Indonesia

- Moladin

- Mobil123

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Online Classified and E-retail Activity

- 4.2.2 Banks' Pivot to Used-car Specific Loan Products

- 4.2.3 Expanding Organized Dealer Networks Outside Java

- 4.2.4 Ride-hailing Fleet Renewal Cycles (Grab and Gojek)

- 4.2.5 OEM Buy-back Schemes Boosting Residual Values

- 4.2.6 AI-led Condition Grading Platforms Reducing Price Dispersion

- 4.3 Market Restraints

- 4.3.1 Odometer and Accident-history Fraud Remains Pervasive

- 4.3.2 Fragmented Provincial Registration Databases

- 4.3.3 High Inter-island Logistics Cost Discourages Non-Java Trade

- 4.3.4 Limited Certified-battery Health Checks for Used EVs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Vehicle Type

- 5.1.1 Hatchbacks

- 5.1.2 Sedans

- 5.1.3 SUVs

- 5.1.4 MPVs

- 5.2 By Fuel Type

- 5.2.1 Petrol

- 5.2.2 Diesel

- 5.2.3 Hybrid and Electric

- 5.2.4 Others (LPG, CNG, etc.)

- 5.3 By Price Segment

- 5.3.1 Below USD 5,500

- 5.3.2 USD 5,500 - 10,999

- 5.3.3 USD 11,000 - 21,999

- 5.3.4 >= USD 22,000

- 5.4 By Sales Channel

- 5.4.1 Online Digital Classified Portals

- 5.4.2 Pure-play e-Retailers

- 5.4.3 Dealer/OEM Online Platforms

- 5.4.4 Physical Franchise Dealerships

- 5.4.5 Independent Used-Car Lots

- 5.4.6 Auction Houses (Physical and Online Hybrid)

- 5.4.7 Peer-to-Peer (Private) Sales

- 5.5 By Vendor Type

- 5.5.1 Organized

- 5.5.2 Unorganized

- 5.6 By Vehicle Age

- 5.6.1 0 - 2 Years

- 5.6.2 3 - 5 Years

- 5.6.3 6 - 8 Years

- 5.6.4 Above 8 Years

- 5.7 By Financing Providers

- 5.7.1 Original Equipment Manufacturers (OEMs)

- 5.7.2 Banks

- 5.7.3 Non-Banking Financial Companies

- 5.8 By Province

- 5.8.1 West Java

- 5.8.2 East Java

- 5.8.3 Central Java

- 5.8.4 North Sumatra

- 5.8.5 Banten

- 5.8.6 Jakarta

- 5.8.7 Other Provinces

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Mobil88 (PT Serasi Auto Raya (SERA))

- 6.4.2 Toyota Astra Motor (Toyota Trust)

- 6.4.3 PT Tunas Ridean Tbk.

- 6.4.4 PT Inchcape Indomobil Distribution Indonesia (IIDI) (Mercedes Certified)

- 6.4.5 BMW Premium Selection (BME Eurokars)

- 6.4.6 OLX Indonesia

- 6.4.7 Carro Indonesia (Trusty Cars Ltd )

- 6.4.8 Carsome Indonesia

- 6.4.9 Broom.id

- 6.4.10 Carmudi Indonesia

- 6.4.11 Moladin

- 6.4.12 Mobil123

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2026-2030年全球二手车市场

2026-2030年全球二手车市场 二手车市场:2026-2032年全球市场预测(按车辆类型、燃料类型、年份、变速箱类型、所有权、用途和销售管道)

二手车市场:2026-2032年全球市场预测(按车辆类型、燃料类型、年份、变速箱类型、所有权、用途和销售管道) 二手半拖车市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、流程及最终用户二手

二手半拖车市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、流程及最终用户二手 东南亚二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)非洲二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

东南亚二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)非洲二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年) 二手车市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,以及2026-2034年的预测

二手车市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,以及2026-2034年的预测 二手拖车市场-全球产业规模、份额、趋势、机会和预测:按车辆类型、动力类型、销售管道、地区和竞争格局划分,2021-2031年二手车市场 - 全球产业规模、份额、趋势、竞争格局、机会、预测(按车辆类型、动力类型、销售管道、最终用途、地区和竞争情况划分),2021-2031年印尼二手车融资:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

二手拖车市场-全球产业规模、份额、趋势、机会和预测:按车辆类型、动力类型、销售管道、地区和竞争格局划分,2021-2031年二手车市场 - 全球产业规模、份额、趋势、竞争格局、机会、预测(按车辆类型、动力类型、销售管道、最终用途、地区和竞争情况划分),2021-2031年印尼二手车融资:市场占有率分析、产业趋势与统计、成长预测(2026-2031)