|

市场调查报告书

商品编码

1911471

菲律宾二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Philippines Used Car - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

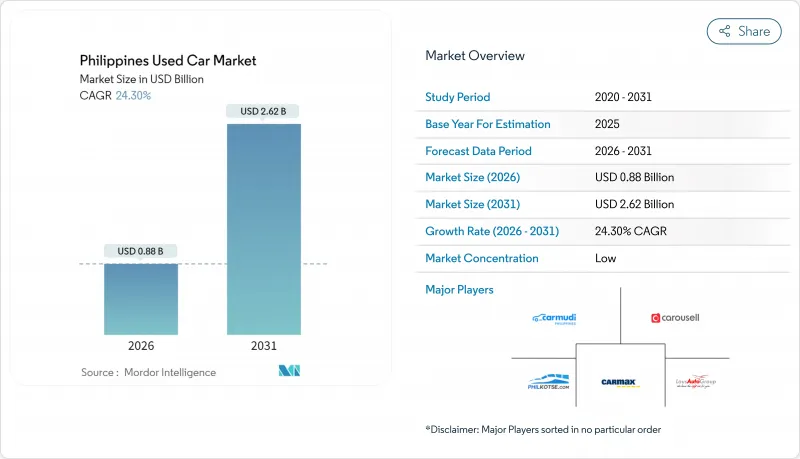

预计菲律宾二手车市场将从 2025 年的 7.1 亿美元成长到 2026 年的 8.8 亿美元,到 2031 年达到 26.2 亿美元,2026 年至 2031 年的复合年增长率为 24.30%。

这一令人瞩目的成长展现了市场在经济挑战下的韧性。新车价格上涨和中产阶级日益增长的出行需求正促使更多菲律宾人选择二手车。数位平台在促进市场扩张、提高透明度和简化交易流程方面发挥关键作用。预计这些线上通路在2025年至2030年间将迎来强劲成长。监管政策的调整,例如陆路交通管理局(LTO)暂停征收车辆过户罚款,正在推动二手车交易流程。此外,汽车金融渗透率的快速提升,以及银行与数位汽车交易平台之间的合作,预计将在未来几年推动交易量的成长。

菲律宾二手车市场趋势与分析

透过线上广告和电子商务实现二手车交易数位化

菲律宾二手车市场的数位转型正在从根本上改变交易结构,如今85%的销售线索都来自线上,尤其是Facebook等社群媒体平台。这种转变将传统的购车週期从数週缩短至数天,消费者利用数位工具比较不同选项、查询车辆历史记录并在前往经销商之前获得融资。数位平台的功能也日益超越简单的资讯发布,提供端到端的交易服务,包括线上支付、电子文件和虚拟验车。这种转变在网路普及率超过72%的大马尼拉地区最为明显,随着智慧型手机的普及,这种趋势正迅速扩展到其他地区城市。

马尼拉大都会不断壮大的中产阶级推动了对经济实惠交通工具的需求。

马尼拉大都会区不断壮大的中产阶级对经济实惠的出行解决方案的需求空前高涨,二手车市场正成为首次购车者的主要途径。这项人口结构的变化体现在25至35岁的年轻专业身上,他们更重视车辆的保值性和实用性,而非新车身分。推动这一趋势的经济务实性体现在他们对价格在50万至100万披索比索之间的车辆的偏好上,这类车辆在质量和价格之间取得了最佳平衡,能够满足月收入在5万至10万披索之间的中等收入家庭的需求。这种影响不仅限于车辆所有权本身,也延伸到车辆选择标准,燃油效率和维护成本逐渐取代品牌形象,成为首要考量。

车辆历史记录缺乏透明度会削弱买家信心。

菲律宾二手车市场仍面临车辆历史资讯不透明和文件管理不规范等挑战,尤其是在非正规市场,这持续侵蚀消费者的信任。资讯缺失导致购车过程出现许多摩擦,迫使买家依赖表面化的检查和第三方技工,而非已开发市场普遍采用的全面车辆历史报告。这种信任缺失在农村地区尤其严重,因为这些地区车辆检验服务有限,造成市场效率和价格上的区域差异。

细分市场分析

由于营运成本低且擅长建立人际关係,非正规经销商,尤其是在大都会区以外的地区,预计到2025年将占据71.65%的销售额。他们吸引那些寻求折扣的顾客,但由于文件资料不足,也面临一些挑战,这可能会让买家望而却步。非正规经销商凭藉对超当地语系化市场的深入了解和人际关係销售技巧,尤其是在遍远地区,得以维持市场地位,因为在这些地区,人脉关係往往比正式的资格认证更为重要。他们的经营模式通常以营运成本低、手续简便为特点,这使得他们能够提供具有竞争力的价格,但也带来了透明度方面的挑战,这对于日益成熟的消费者来说往往是一个问题。

以Carmudi和Automart.PH主导的成熟二手车市场正以25.05%的复合年增长率快速扩张,透过提供车辆检验证书、预先核准贷款和7天退货保证等服务,有效缓解了消费者的购车焦虑。线上平台覆盖全国,而位于马尼拉大都会区、宿雾和达沃的实体店则提供试驾和售后服务。随着消费者对车辆历史记录的要求日益提高,菲律宾二手车市场正逐步向这些透明化的平台转型。

到2025年,轿车将占汽车交易总量的36.10%,并将继续成为追求低运行成本的通勤者的首选。同时,SUV和MPV将以24.72%的复合年增长率成长,这主要得益于家庭用户对高离地间隙的需求,以应对洪水和坑洞路面。丰田威驰和本田锋范等紧凑型日系车型在该类别中占据主导地位,凭藉其可靠的性能和充足的零件供应,为用户提供了低廉的用车成本。掀背车是预算有限的消费者的入门车型,而厢型车则服务于商业用户和需要最大载客量的大家庭。皮卡在农村地区保持稳定的需求,因为越野实用性和耐用性是这些地区用户考虑的关键因素。

丰田Fortuna和三菱Montero Sport等中型SUV正在推动这一快速增长,它们配备了最新的驾驶辅助系统,并可容纳七名乘客。掀背车和厢型车保持着稳定的细分市场,而皮卡则迎合了需要兼顾货物运输和崎岖路况的农村买家的需求。预计到2030年,SUV在菲律宾二手车市场与轿车的销售差距将显着缩小。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 透过线上广告和电子商务实现二手车交易数位化

- 马尼拉大都会不断壮大的中产阶级将推动对经济实惠的交通工具的需求。

- 透过积极的OEM置换和融资计划缩短车辆拥有周期

- 受海外务工人员汇款支持的区域成长中心采购趋势

- 苏比克湾和自由港地区进口配额放宽,促进了供应。

- 燃油成本上涨正促使人们转向二手更节能的二手车。

- 市场限制

- 车辆历史记录缺乏透明度会降低买家信心。

- 颱风季过后,洪水灾害风险会降低残值。

- 都市区来自共乘和微出行的竞争

- 高利率限制了消费者获得金融产品的机会。

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方和消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元)及销售量(单位))

- 依供应商类型

- 有组织的

- 杂乱无章

- 按车辆类型

- 掀背车

- 轿车

- SUV 和 MPV

- 皮卡车

- 货车

- 按燃料类型

- 汽油

- 柴油引擎

- 混合动力汽车和电动车

- 其他(压缩天然气、液化石油气)

- 按销售管道

- 在线的

- 离线

- 按车辆型号年份

- 0-3岁

- 4-6年

- 7-10岁

- 超过10年

- 按价格范围(菲律宾比索)

- 不到50万披索

- 披索至100万披索

- 超过100万

- 按地区

- 吕宋岛

- 维萨扬群岛

- 棉兰老岛

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Carmudi

- Carousell

- Carmax

- LausGroup

- Toyota Motor Philippines

- Automart.PH

- Philkotse.com

- ZigWheels

- Tsikot.com

- Car Empire

- OLX Philippines

- AutoDeal.com.ph

- Hyundai HARI CPO

- Volkswagen PH

- Ford Philippines

- PGA Cars Premium Used

- Mitsubishi Diamond CPO

- Nissan Intelligent Choice PH

- Suzuki Certified Used Cars

- Isuzu PH Used Truck Centers

- Grab AutoExchange

- BPI Repossessed Cars Marketplace

第七章 市场机会与未来展望

The Philippines Used Car Market is expected to grow from USD 0.71 billion in 2025 to USD 0.88 billion in 2026 and is forecast to reach USD 2.62 billion by 2031 at 24.30% CAGR over 2026-2031.

This impressive growth underscores the market's resilience in economic challenges. As new car prices climb and the middle class seeks mobility, more Filipinos turn to pre-owned vehicles. Digital platforms are playing a pivotal role, boosting market expansion, enhancing transparency, and streamlining transactions. These online channels are anticipated to grow robustly from 2025 to 2030. Regulatory changes, like the LTO's temporary halt on ownership transfer penalties, are smoothing out the resale process. Furthermore, a surge in auto loan penetration, coupled with collaborations between banks and digital auto marketplaces, is set to amplify transaction volumes in the coming years.

Philippines Used Car Market Trends and Insights

Digitalization of Used-Car Transactions via Online Classifieds and E-commerce

The digital transformation of the Philippines used car market is fundamentally altering transaction dynamics, with 85% of leads now originating from online sources, particularly social media platforms like Facebook. This shift has compressed the traditional buying cycle from weeks to days as consumers leverage digital tools to compare options, check vehicle histories, and secure financing before visiting dealerships. Digital platforms are not merely listing services but increasingly offer end-to-end transaction capabilities, including online payment processing, digital documentation, and virtual inspections.The transition is most pronounced in Metro Manila, where internet penetration exceeds 72%, but is rapidly extending to provincial cities as smartphone adoption increases

Middle-Class Expansion in Metro Manila Boosting Affordable Mobility Demand

The expanding middle class in Metro Manila is creating unprecedented demand for affordable mobility solutions, with the used car market serving as the primary entry point for first-time vehicle owners. This demographic shift is characterized by young professionals aged 25-35 who prioritize value retention and practical features over new-car prestige. The economic pragmatism driving this trend is evident in the preference for vehicles in the PHP 500k-1 million range, which offers the optimal balance between quality and affordability for middle-income households earning PHP 50,000-100,000 monthly. The impact extends beyond simple ownership to influence vehicle selection criteria, with fuel efficiency and maintenance costs becoming primary considerations over brand prestige.

Limited Vehicle-History Transparency Undermining Buyer Trust

The persistent challenge of limited vehicle history transparency continues to undermine consumer confidence in the Philippines used car market, particularly in the dominant unorganized segment where documentation practices remain inconsistent. This information asymmetry creates significant friction in the purchasing process, with buyers forced to rely on superficial inspections or third-party mechanics rather than comprehensive vehicle history reports that are standard in more developed markets. The trust deficit is most acute in provincial areas where access to vehicle verification services is limited, creating geographic disparities in market efficiency and pricing.

Other drivers and restraints analyzed in the detailed report include:

- OEM Trade-in and Financing Programs Shortening Ownership Cycles

- OFW Remittance-Driven Purchases in Provincial Growth Centers

- Competition from Ride-hailing and Micro-mobility in Urban Hubs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Unorganized dealers controlled 71.65% of 2025 sales thanks to lower overheads and relationship-based negotiations, particularly outside major cities. They appeal to bargain hunters but struggle with limited documentation, which fuels buyer hesitation. Unorganized dealers maintain their foothold through hyperlocal market knowledge and relationship-based selling, particularly in provincial areas where personal connections often outweigh formal guarantees. Their business model typically involves lower overhead costs and minimal documentation, allowing for competitive pricing but creating transparency challenges that increasingly sophisticated consumers find problematic.

Organized players, led by Carmudi and Automart.PH is scaling at 25.05% CAGR by bundling inspection certificates, financing pre-approval, and seven-day return windows that reduce purchase anxiety. Their digital storefronts reach a national audience, while physical hubs in Metro Manila, Cebu, and Davao anchor test drives and after-sales service. As consumer expectations for verifiable histories grow, the Philippines' used car market gradually shifts toward these transparent marketplaces.

Sedans captured 36.10% of transactions in 2025 and remain the entry point for commuters seeking low running costs. Yet SUVs and MPVs are charting a 24.72% CAGR, buoyed by families looking for higher ground clearance against floods and potholes. The category is dominated by compact Japanese models like the Toyota Vios and Honda City, which benefit from established reliability reputations and abundant parts availability that reduce ownership costs. Hatchbacks serve as entry-level options for budget-conscious consumers, while vans cater to commercial users and large families requiring maximum passenger capacity. Pickup trucks maintain steady demand in provincial areas where utility and durability on unpaved roads are primary considerations.

Mid-sized contenders such as the Toyota Fortuner and Mitsubishi Montero Sport headline this surge, offering modern driver-assistance suites and seven-seat capacity. Hatchbacks and vans maintain steady niche roles, while pickups cater to provincial buyers balancing cargo needs and rugged roads. The Philippines used car market size for SUVs is forecast to close much of the volume gap with sedans by 2030.

Philippines Used Car Market Report is Segmented by Vendor Type (Organized and Unorganized), Vehicle Type (Hatchbacks, Sedans, and More), Fuel Type (Petrol, Diesel, and More), Sales Channel (Online and Offline), Vehicle Age (0 To 3 Years, 4 To 6 Years, and More), Price Band (Less Than PHP 500K, PHP 500K To 1 Million, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Carmudi

- Carousell

- Carmax

- LausGroup

- Toyota Motor Philippines

- Automart.PH

- Philkotse.com

- ZigWheels

- Tsikot.com

- Car Empire

- OLX Philippines

- AutoDeal.com.ph

- Hyundai HARI CPO

- Volkswagen PH

- Ford Philippines

- PGA Cars Premium Used

- Mitsubishi Diamond CPO

- Nissan Intelligent Choice PH

- Suzuki Certified Used Cars

- Isuzu PH Used Truck Centers

- Grab AutoExchange

- BPI Repossessed Cars Marketplace

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digitalization of Used-Car Transactions via Online Classifieds and E-commerce

- 4.2.2 Middle-Class Expansion in Metro Manila Boosting Affordable Mobility Demand

- 4.2.3 Aggressive OEM Trade-in and Financing Programs Shortening Ownership Cycles

- 4.2.4 OFW Remittance-Driven Purchases in Provincial Growth Centers

- 4.2.5 Relaxed Import Quotas in Subic and Freeport Zones Spurring Supply

- 4.2.6 Rising Fuel Costs Driving Shift to More Efficient Used Vehicles

- 4.3 Market Restraints

- 4.3.1 Limited Vehicle-History Transparency Undermining Buyer Trust

- 4.3.2 Flood-Damage Risk Post-Typhoon Season Depressing Residual Values

- 4.3.3 Competition from Ride-hailing and Micro-mobility in Urban Hubs

- 4.3.4 High Interest Rates Constraining Consumer Financing Access

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vendor Type

- 5.1.1 Organized

- 5.1.2 Unorganized

- 5.2 By Vehicle Type

- 5.2.1 Hatchbacks

- 5.2.2 Sedans

- 5.2.3 SUVs and MPVs

- 5.2.4 Pickup Trucks

- 5.2.5 Vans

- 5.3 By Fuel Type

- 5.3.1 Petrol

- 5.3.2 Diesel

- 5.3.3 Hybrid and Electric

- 5.3.4 Others (CNG, LPG)

- 5.4 By Sales Channel

- 5.4.1 Online

- 5.4.2 Offline

- 5.5 By Vehicle Age

- 5.5.1 0 to 3 Years

- 5.5.2 4 to 6 Years

- 5.5.3 7 to 10 Years

- 5.5.4 More than 10 Years

- 5.6 By Price Band (PHP)

- 5.6.1 Less than 500 k

- 5.6.2 500k to 1 million

- 5.6.3 More than 1 million

- 5.7 By Geography

- 5.7.1 Luzon

- 5.7.2 Visayas

- 5.7.3 Mindanao

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Carmudi

- 6.4.2 Carousell

- 6.4.3 Carmax

- 6.4.4 LausGroup

- 6.4.5 Toyota Motor Philippines

- 6.4.6 Automart.PH

- 6.4.7 Philkotse.com

- 6.4.8 ZigWheels

- 6.4.9 Tsikot.com

- 6.4.10 Car Empire

- 6.4.11 OLX Philippines

- 6.4.12 AutoDeal.com.ph

- 6.4.13 Hyundai HARI CPO

- 6.4.14 Volkswagen PH

- 6.4.15 Ford Philippines

- 6.4.16 PGA Cars Premium Used

- 6.4.17 Mitsubishi Diamond CPO

- 6.4.18 Nissan Intelligent Choice PH

- 6.4.19 Suzuki Certified Used Cars

- 6.4.20 Isuzu PH Used Truck Centers

- 6.4.21 Grab AutoExchange

- 6.4.22 BPI Repossessed Cars Marketplace

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

二手半拖车市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、流程及最终用户二手

二手半拖车市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、流程及最终用户二手 东南亚二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)非洲二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

东南亚二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)非洲二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年) 二手拖车市场-全球产业规模、份额、趋势、机会和预测:按车辆类型、动力类型、销售管道、地区和竞争格局划分,2021-2031年二手车市场 - 全球产业规模、份额、趋势、竞争格局、机会、预测(按车辆类型、动力类型、销售管道、最终用途、地区和竞争情况划分),2021-2031年印尼二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)印尼二手车融资:市场占有率分析、产业趋势与统计、成长预测(2026-2031)德国二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

二手拖车市场-全球产业规模、份额、趋势、机会和预测:按车辆类型、动力类型、销售管道、地区和竞争格局划分,2021-2031年二手车市场 - 全球产业规模、份额、趋势、竞争格局、机会、预测(按车辆类型、动力类型、销售管道、最终用途、地区和竞争情况划分),2021-2031年印尼二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)印尼二手车融资:市场占有率分析、产业趋势与统计、成长预测(2026-2031)德国二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲二手车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)